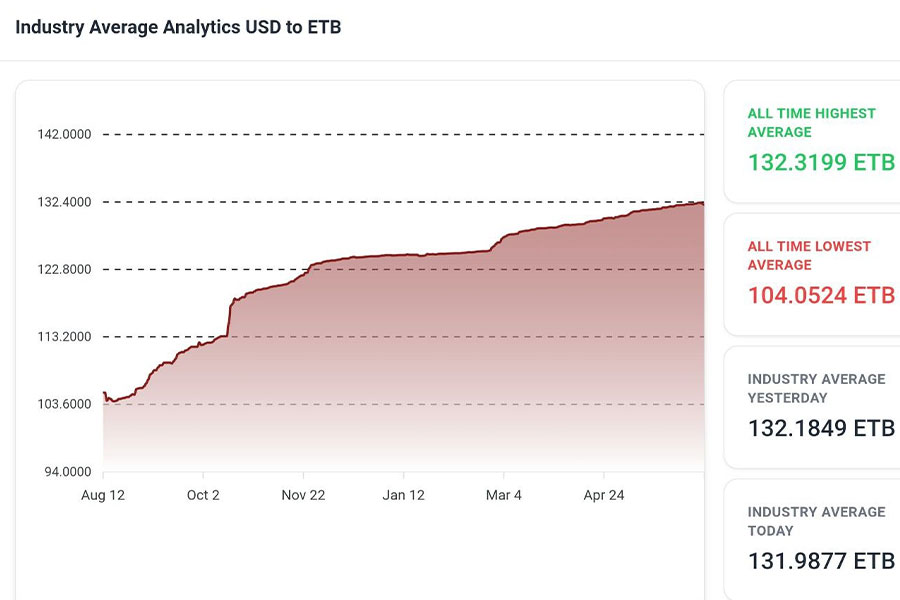

Radar | Nov 29,2025

Nov 8 , 2025

By Jayati Ghosh

As stock markets hit record highs, rising financial fragility is setting off alarm bells across the United States and Europe. The International Monetary Fund (IMF) has recently echoed these concerns, stoking fears of a looming crisis.

The warning signs are everywhere, and they are disturbingly familiar. Asset prices are climbing well beyond what can be justified by underlying fundamentals, while non-bank financial intermediaries now play a similar role to that of "shadow banks" in the years leading up to the 2008 financial crisis. At the same time, the rise of stablecoins has pulled regulated banks into the opaque world of cryptocurrencies, and vast sums of speculative capital are flooding into AI stocks, driven more by hype than by proven returns.

These trends bear the unmistakable marks of a financial bubble entering its most precarious stage, when even minor shifts in investor sentiment can trigger a sharp correction. The recent collapse of US auto parts supplier First Brands and subprime auto lender, Tricolor, both heavily leveraged and closely linked to non-bank financial institutions, may be early indications of structural vulnerabilities that are only coming into view.

Behind this growing fragility lies the rapid expansion of private financial institutions over the past decade.

According to the Financial Stability Board, these entities, which raise funds from retail investors and leverage their positions through aggressive borrowing, now account for nearly half of the world's total financial assets. Their appetite for risk has helped drive up asset prices, even amid trade uncertainties and policy volatility. The dismantling of already weak financial regulations under US President Donald Trump has only compounded the threat.

Taken together, these forces could set in motion the manic cycle famously described by the economic historian Charles Kindleberger.

The first stage, "euphoria," is dominated by optimism and excess. It is inevitably followed by a period of "stringency" as defaults rise and credit tightens, before giving way to "revulsion," when fear grips financial markets and even solvent borrowers struggle to find financing. Whether this sequence culminates in full-blown panic and collapse depends largely on how governments respond. But even without a crash, the consequences can be severe.

If history is any guide, the question is when, not if, another major financial meltdown will occur. For most of the world's population, however, the more pressing concern is how a crisis that originates in the US and Europe will affect their own countries.

The precedents are hardly reassuring. Both the 2008 crisis and the COVID-19 pandemic showed that turmoil in the US and other wealthy economies can devastate poorer countries with limited fiscal space and little protection against external shocks. When crises spread beyond financial markets, the damage is swift and far-reaching. Investment dries up, growth falters, and unemployment rises, triggering a chain reaction that reduces export demand and curtails foreign-exchange inflows from tourism and remittances, spreading the pain worldwide.

Entrenched currency hierarchies exacerbate the problem. The dominance of the Dollar, for example, ensures that in times of heightened uncertainty, private capital flows back to the US, causing sharp depreciations and banking crises in lower-income countries. Fears of capital flight further impede governments' ability to pursue countercyclical macroeconomic policies, making an already-difficult adjustment even harder.

The fallout could be especially severe for debt-distressed countries, many of which built their growth strategies around exports to advanced economies. That model has since been undermined by Trump's protectionist policies, leaving indebted countries dangerously exposed to a confluence of economic, geopolitical, and climate shocks that threaten to turn the next global financial crisis into a truly catastrophic event.

Developing countries should recognise these risks and take urgent steps to strengthen their economic resilience. The top priority should be to diversify trade relationships. Confronted with the Trump Administration's erratic and often unreasonable demands, some have already begun reducing dependence on the US. This process, though necessary, will not be painless.

To bolster their financial resilience, developing countries need to limit their exposure to volatile capital flows by adopting effective capital management tools and strengthening financial oversight, not merely through prudential regulations, but also by curbing speculative and opaque activities. Such safeguards should be in place before the next crisis erupts. In the medium term, reducing dependence on external debt is essential, as is preventing destabilising outflows by redefining the terms under which foreign investors operate.

Admittedly, the Trump Administration's efforts to steer its trading partners in the opposite direction, toward loosening regulation, particularly of cryptocurrencies, make this task exceedingly difficult. But only by resisting such pressures can developing countries avoid being swept into another crisis not of their making.

PUBLISHED ON

Nov 08,2025 [ VOL

26 , NO

1332]

Radar | Nov 29,2025

Money Market Watch | Jun 15,2025

Fortune News | Nov 24,2024

Verbatim | Feb 21,2026

Delicate Number | Sep 10,2023

Radar | Nov 08,2025

Radar | Jun 18,2022

Commentaries | Oct 03,2024

Editorial | Nov 29,2025

My Opinion | Aug 12,2023

Photo Gallery | 192208 Views | May 06,2019

Photo Gallery | 181980 Views | Apr 26,2019

Photo Gallery | 178722 Views | Oct 06,2021

My Opinion | 144237 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jul 25 , 2026 . By BEZAWIT HULUAGER

Global Bank's Board of Directors have overhauled top management, after suspending sev...

Jul 25 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have overturned the National Lottery Administration...

A newly enacted regulation by the Council of Ministers lets eligible producers pledge...

Jul 25 , 2026 . By FITSUM TADESSE

A fuel tanker carrying tens of thousands of litres was confiscated after its driver a...

Loading your updates...

Loading your updates...