Radar | Sep 10,2021

Feb 5 , 2022.

The price of 12ltr of cylinder gas (LPG), an essential energy source for urban kitchens, shot up last week to 2,600 Br, increasing by more than four folds compared to prices three years ago. The rise in such a rate could only be explained by the loss of the Birr against the Dollar and other currencies as LPG is an imported commodity.

It may be too anecdotal to make a grand conclusion from this on the macroeconomic state of the country. But it is a symptom that should serve as a crucial sign of how policymaking (or not making) has a painful bearing on the market and consumers. The ailing has its roots buried deep in the economic structure and history of the country.

Over the past century, Ethiopia has had 44 years of left-leaning economic policymaking. The first 17 years were unfettered with private profit-making except in the case of micro-sized businesses. As it was known then, the command economy was extensively experimented with, including collectivised agriculture, quota in production, and fixed prices by the state's agents. The following 27 years led to liberalisation programs, most notably in the financial sector. Even then, the economic development that followed was state-centric, with the height of the economy commanded by the state. Enterprises in the telecom, airline and logistics sectors remained monopolies and subsidies in fuel and electricity were kept.

This was not, however, sufficient to address the structural limitations in the economy: productivity and competitiveness. More so, it was a significant slant in intellectual discourse away from free-market principles. Those on the left (and there were too many of them in and outside of the ruling political force) chose to confuse the legitimate demand for free-market with a market that is free of the state. Hence, the market was looked upon with suspicion. Any arguments in its favour are considered tantamount to being a neo-liberal. Bring up the issue in academic circles. The left would launch an offensive from their selective readings of Joseph Stiglitz, Nobel winning economist, and the harm done by structural adjustment programs of the 1980s.

The first real break to nearly half a century of intimacy with left-leaning economic policymaking was in 2018. The ascent to the highest executive office of Prime Minister Abiy Ahmed's (PhD) administration came to the scene, all guns blazing. Opening up the economy has been considered necessary, from rail systems and sugar estates to telecom and logistics. The Prime Minister may have a bent for conservatism on social issues and could have a knack for political illiberalism. His intention for economic liberalism was adequately demonstrated after he took office. To his predecessors’ credit, the Growth & Transformation Plans (GTPs) did target eventually putting the private sector at the driver’s seat, even if they were short on the details or suspect in their sincerity.

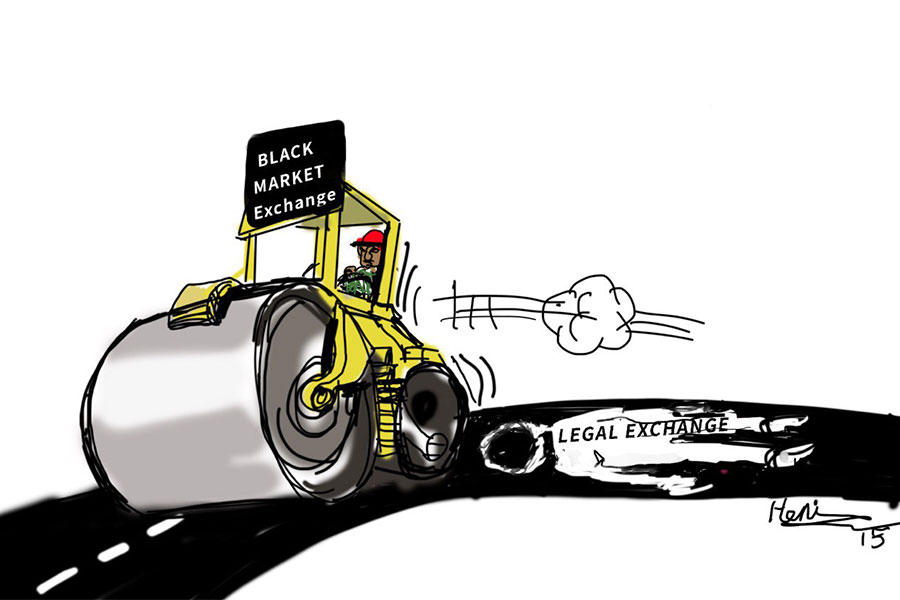

Nonetheless, even the new administration, with its liberal temptations, has not dared to go the extra mile. Considering the low base Ethiopia is starting from, pushing third-generation privatisation cannot be as groundbreaking as many would like to think. A bolder move to integrate the country into the global markets would be to liberalise the capital account and float the exchange rate regime, unleashing its economic potential despite fears of short term risks.

Unfortunately, the administration is teetering even on its modest liberalisation plans of opening up specific industries.

It has been three years, but no major state enterprise has been privatised. Only the telecom industry has welcomed a competitor after over a century of state monopoly. There is neither a capital market nor has the country moved far along in its accession into the World Trade Organisation (WTO). This is not a reassuring record. It could mean that meaningful liberalisation in the capital and currency markets would be lost as an agenda.

The administration’s indecision and lack of conviction could be part of the problem. There is no better example of this than how caveats to telecom liberalisation, especially on mobile payments, might have cost the state millions of dollars in its license agreement with Safaricom Ethiopia. But this seems only partially the reason.

The fear of short term risks and the reluctance to go full course in setting the economy free of its structural and historical chains would be understandable. The two most significant challenges may have been the public health crisis due to COVID-19 and the civil war. The former has put greater importance on low-income targeted policies such as subsidies. The pandemic's economic turmoil worldwide has bolstered many governments heavy-handed involvement with economies. Developed countries have pumped over 11 trillion dollars to bail out their economies. Ethiopia’s case has at least kept liberalisation efforts from progressing, slashing revenues from tourism and remittance and putting pressure on foreign currency reserves.

The civil war has had an even more devastating impact on the economy. A fall in productivity and investor confidence and cuts to development aid have made capital and foreign currency more scarce. It has ballooned headline inflation to over 35pc. A Birr loss in value has led to a fall in savings and an increasing dollarisation of the economy. The fear that opening the capital account and floating the Birr at such a time could bankrupt the country is therefore legitimate. It was such concerns following the Dollar gaining so much on the Birr in the parallel market at some point, indicating higher than usual capital flight, that the central bank suspended collateralised lending for a quarter of the year.

These events should not be surprising to have knocked the administration off its course. But it needs to get back on track, building on its liberalisation initiatives and move onto the monetary policy front. It first needs to address threats to capital flight.

The COVID-19 pandemic does not increase capital flight, but it has put substantial pressure on the treasury and foreign currency reserves by reducing revenues from tourism and remittances. The pandemic may never go away, but there is a more significant global consensus that it is impossible to continue on and off with lockdowns. International travel and large gatherings may become annoying (tests at different checkpoints and mask-wearing guidelines), but there is hope that they will recover.

The administration still needs to worry about the militarized conflict in the north and the insurgency in the southwest, nonetheless. This requires a political prescription. Securing peace through a negotiated settlement can better prepare the ground for the much needed economic liberalisation to occur. An open capital account and market-based exchange rate regime require a political environment with a modicum of stability. Peace will further improve the diplomatic fallout with the Transatlantic Alliance to recover development aid. It could also make Ethio telecom partial privatisation and the offering for a second national telecom operating license more attractive to prospective investors, all of which are important to building up the foreign currency reserve.

Neither would it be possible to bring inflation down to the single-digit with a war that chokes down supply chains and forces the administration into deficit financing, most likely through printing money. The budget deficit will hit four percent of GDP this year, a percentage point higher than is considered prudent. The administration will find it hard to lower the gap while at the same time prosecuting a costly war.

An administration with the courage in its convictions to secure lasting peace through a negotiated settlement can launch an economic opening aggressively with more confidence. It has already taken some overdue actions, including lifting subsidies in energy, sugar, edible oil, wheat and eventually fuel. But these are only beginnings. As long as the economy remains at the mercy of bureaucrats who make the very few rich with a stroke of pens and the many impoverished, the economy will continue to be robbed of the competitiveness it needs to take itself to the next level.

This should not be confused with market fundamentalism, as the folks from the left often argue. Regulations, or the state's role in the economy, can be instrumental but in a different way. The state would not be selling goods and services but creating an environment that makes it possible for everyone else to increase overall economic output. Regrettably, this is unlikely to happen with the gaze of bureaucrats distributing rents in an economy historically marked by deprivation.

PUBLISHED ON

Feb 05,2022 [ VOL

22 , NO

1136]

Radar | Sep 10,2021

Addis Fortune | May 04,2024

Radar | Dec 21,2019

Sponsored Contents | Apr 04,2022

Fortune News | Oct 18,2025

Editorial | Oct 01,2022

Viewpoints | Jul 18,2021

Fortune News | Dec 05,2018

Fortune News | Apr 13,2024

Radar | Apr 24,2021

Photo Gallery | 190073 Views | May 06,2019

Photo Gallery | 179817 Views | Apr 26,2019

Photo Gallery | 176467 Views | Oct 06,2021

My Opinion | 142162 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 21 , 2026 . By NAHOM AYELE

Federal and regional authorities have spent months urging taxpayers to pay more into...

Jun 21 , 2026 . By BEZAWIT HULUAGER

The fledgling capital market is producing the headline numbers its architects hoped f...

Jun 21 , 2026 . By BEZAWIT HULUAGER

Nightly "Z-report" summaries from physical cash registers are to be replaced by real...

Jun 21 , 2026 . By HELINA HADGU

In the fast-growing towns of South Ethiopia, the cost of progress is arriving one cor...

Loading your updates...

Loading your updates...