Commentaries | Dec 09,2023

Oct 11 , 2025

By Yehualashet Tamiru , Naomi Atlabachew

Debt and equity will always anchor corporate finance, but the hinge between them, conversion, should swing smoothly, not haul investors around. Updating the exchange-rate rule would unlock capital, fortify companies, and bolster the country's financial standing. Aligning policy with practice is no longer a convenience, but an imperative for growth, argue Yehualashet Tegegn (yehuala5779@gmail.com), attorney and consultant-at-law and adjunct lecturer at the Addis Abeba University (AAU).

Companies hungry for cash face a familiar choice of either borrowing and repaying with interest or selling shares and sharing in the upside. Debt has fixed repayment dates, while equity involves surrendering a portion of ownership, and neither path is without its issues.

However, a third route, converting debt into equity, is gaining favour worldwide and appears in Ethiopia’s revised Commercial Code. The idea is simple. Lenders, for our case, are shareholders and are also foreign investors, exchange the money they are owed for stock, thereby strengthening a firm’s balance sheet without draining its day-to-day liquidity.

Any foreign loan first requires approval from the National Bank of Ethiopia (NBE), which vets whether a company truly needs the funds and grants lenders the right to repatriate principal and interest in hard currency. That double check reassures both investors and domestic firms. Still, one vexing issue, which exchange rate applies when the foreign-currency loan is converted into equity, persists. The rulebook is silent.

Bankers and officials tend to default to the “historic” rate —the Birr-to-Dollar level in effect when the shareholder loan was first registered. Instead of the rate on the day the conversion actually happens, they lock in the older figure. The approach is widespread within the Ethiopian Investment Commission and the Central Bank, although it is not codified in statute. The gap breeds uncertainty in foreign investment that Ethiopia can least afford.

Consider what happens when the Birr slides after a loan is logged. A lender agreeing to convert the debt later ends up with fewer Birr for the same dollars. The more the Birr weakens between registration and conversion, the bigger the haircut on the investor’s stake. The damage is real, not theoretical, and it pushes capital to the sidelines. Companies vying for fresh funds find doors slamming shut.

Imagine a foreign shareholder who lent one million dollars when the Birr traded at 50 to the dollar. Suppose the Birr later weakens to 150. Under Ethiopia’s standard practice, the conversion still values the loan at 50 million Birr. At the prevailing rate, the same dollars would fetch 150 million Br. The investor relinquishes the loan, strengthens the company, and ends up owning half the equity that today’s rate would justify. Small wonder lenders hesitate to swap.

Debt-for-equity swaps, when done properly, allow firms to trade liabilities for permanent capital and enable policymakers to shore up the external accounts. Loans eventually demand foreign currency for repayment, a headache for a country already tight on reserves. Equity, by contrast, stays put. It creates no future hard-currency outflow. Hence, macroeconomic policymakers should be cheering conversions, not hobbling them.

Nonetheless, the practice of using old rates makes conversions look punitive. Investors who could take their money back and walk away are punished for choosing to stay. They are compelled to absorb the entire exchange-rate loss. That tips incentives toward short-term lending rather than long-term partnership, throttling the very growth policymakers say they want.

Beyond the balance sheets, reputation is on the line. Global players track how emerging markets treat foreign capital. Rules that appear arbitrary or skewed send a loud message. For a country striving to woo direct investment, perceptions of unpredictability are toxic. There is also the wider economic effect. A thicker equity cushion inside domestic companies eases borrowing constraints, fuels expansion, and creates jobs.

Heavy leverage, on the other hand, drags on credit ratings and crowds out new borrowing. By tying swaps to a stale exchange rate, policy undercuts these broader benefits.

The legal argument for the historic rate is weak. Registration of a loan at the Central Bank is a compliance box to tick, not the moment an investor takes an economic stake. The real transaction occurs when debt is cancelled and shares are issued. Treating the administrative date as the decisive point misaligns regulation with substance and violates basic fairness. Matching valuation with current market conditions shields investors from avoidable currency risk and brings transparency.

Elsewhere, regulators usually peg the swap to the spot rate on the day of execution. Ethiopia could follow that lead and level the playing field overnight. They follow similar logic, and its own ambitions to grow industry, create jobs, and diversify exports depend on a steady inflow of patient capital.

The macro picture reinforces the case for change. Ethiopia’s balance of payments suffers when firms marshal scarce foreign exchange to honour debts. Equity conversions remove that looming strain. They also deepen domestic capital markets and build confidence that profits can be reinvested rather than remitted.

Sceptics argue that sticking with the historic rate protects against speculative timing or sudden conversion demands. Yet, those fears can be addressed through notice periods or caps without crippling valuations. What investors need most is clarity and parity with global norms and simple logic. Indeed, many markets require the use of the spot rate at conversion. Such rules do not ignite a rush to game the system. They simply align accounting with reality.

Failure to modernise carries opportunity costs. Companies weighed down by debt postpone projects, forego hiring, and struggle to compete. Banks hesitate to extend credit to firms that are already heavily leveraged. A straightforward fix, valuing swaps at the prevailing date rate, would flip those dynamics. Applying the prevailing rate can also cushion investors against swings they cannot control. Currency depreciation is a systemic risk, not a matter of individual misjudgment. Making one party absorb all of it is neither efficient nor equitable. Sharing risk through fair valuation keeps capital flowing and encourages reinvestment.

The gap between regulatory form and economic substance thus strikes at confidence. If investors cannot predict how their loans will be treated years down the road, they will price that uncertainty, or steer clear altogether. Ethiopia’s drive to industrialise and climb the value chain depends on reversing that perception. Thus, policymakers face a choice between continuing with an unwritten rule that discounts investor contributions or adopting a transparent, market-based measure. The latter course lowers financing costs and signals a commitment to fairness.

They can clearly indicate in the bylaws that debt-to-equity conversions use the exchange rate on the date of execution. They can also require companies to notify regulators in advance, allowing oversight without distorting value. They can tie any exceptions to clear and objective criteria.

Such reforms would resonate beyond balance sheets, amplifying the message that policymakers value long-term partnerships, respect economic reality, and price stability over procedural quirks. In an era of mobile capital and stiff competition for investment, that message could make the difference between stagnation and acceleration.

PUBLISHED ON

Oct 11,2025 [ VOL

26 , NO

1328]

Commentaries | Dec 09,2023

Advertorials | Sep 15,2023

Viewpoints | Aug 10,2024

Money Market Watch | Nov 16,2025

Radar | Mar 02,2024

Delicate Number | Apr 13, 2025

Fortune News | Sep 13,2025

Editorial | Nov 23,2024

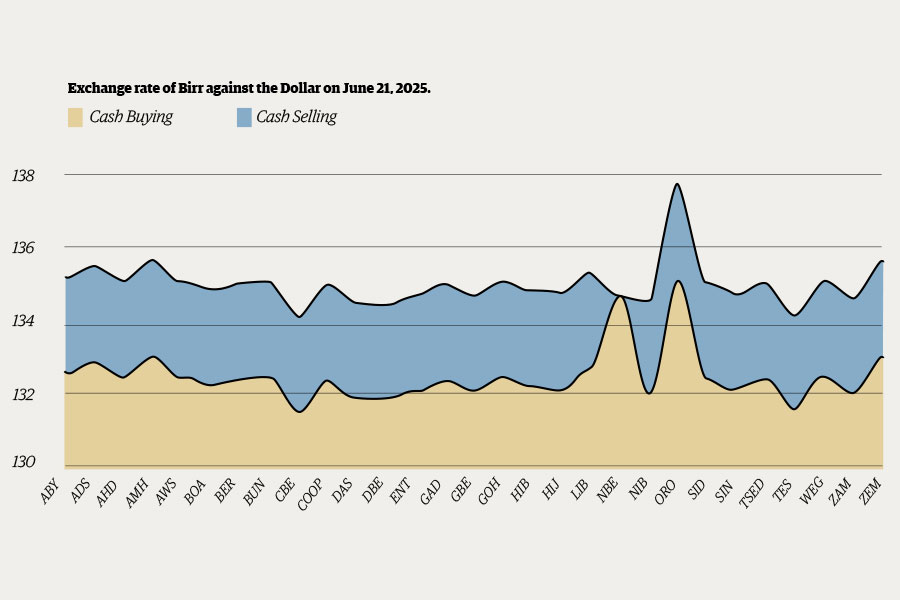

Money Market Watch | Jun 21,2025

Photo Gallery | 191951 Views | May 06,2019

Photo Gallery | 181704 Views | Apr 26,2019

Photo Gallery | 178428 Views | Oct 06,2021

My Opinion | 143967 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jul 25 , 2026 . By BEZAWIT HULUAGER

Global Bank's Board of Directors have overhauled top management, after suspending sev...

Jul 25 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have overturned the National Lottery Administration...

Jul 25 , 2026 . By NAHOM AYELE

A newly enacted regulation by the Council of Ministers lets eligible producers pledge...

Jul 25 , 2026 . By FITSUM TADESSE

A fuel tanker carrying tens of thousands of litres was confiscated after its driver a...

Loading your updates...

Loading your updates...