Fortune News | Jul 25,2026

Sep 10 , 2023

By , Bogolo Kenewendo and Reuben Wambui

Climate finance is inefficient, insufficient, and unfair. With debt levels and borrowing costs soaring, climate action must be funded through more equity investments and concessional financing. That means focusing on the needs of African countries, which are disproportionately vulnerable to climate change, despite contributing the least to creating the problem, in creating and implementing green-finance tools.

The sooner leaders of advanced economies and international organizations understand what Africa needs to achieve a just energy transition and provide the required financing and technology transfers, the greater the chance that the world will reach net-zero emissions by 2050. This week, Kenya is hosting the inaugural Africa Climate Summit and Africa Climate Week to increase commitments and pledges to support climate adaptation efforts and scale up renewable energy on the continent. That makes this an opportune time for governments, the private sector, and multilateral lenders to begin removing the systemic barriers to investment and development in African countries.

To meet the Paris Climate Agreement’s emissions targets, Africa will need 2.8 trillion dollars by 2030 – roughly equal to 93pc of the continent’s GDP. But, with the continent’s combined public debt reaching 1.8 trillion dollars in 2022, many African countries lack the fiscal space to mobilise domestic resources. International investors should fill this gap by providing financing and technology transfers that will help build capacity and develop local industry, rather than merely continuing to exploit the continent’s natural resources.

To that end, starting in Kenya this week and leading up to the United Nations Climate Change Conference (COP28) in Dubai in November and December, governments and financiers must begin implementing five critical reforms to ensure that Africa’s funding needs are met.

Lenders must offer more concessional finance to emerging markets and developing economies (EMDEs). The World Bank and regional multilateral development banks (MDBs), supported by the climate-finance contributions of advanced economies, should provide loans to low- and low-middle-income countries at an interest rate of one per cent and with a 10-year grace period and a 20-year repayment term for initiatives that boost climate resilience. Lending mechanisms such as the World Bank’s International Development Association, traditionally available only to low-income countries, should be extended to low-middle-income countries, and adopted by various multilateral institutions.

Governments and development agencies should also establish large and flexible pools of concessional capital earmarked for climate projects. And they should explore new avenues for international taxation to provide grants, rather than loans, when traditional private or public funding falls short.

Multilateral financial institutions can implement credit enhancement and guarantee schemes to incentivize private-sector participation. Such assurances would mitigate project risks and bolster investor confidence, attracting much-needed private capital to Africa.

Creditors, including in the G20, must provide debt relief to low- and middle-income countries. Given that around 60pc of low-income countries are in or at high risk of debt distress, suspending debt payments or, even better, cancelling debts would significantly improve their ability to respond to the damaging effects of global warming. These institutions need to implement Climate Resilient Clauses in loan contracts for poorer countries, which the World Bank announced this year. Moreover, debt-for-nature and debt-for-climate swaps could enable recipient countries to repay their debts by investing in biodiversity protection and climate action.

Building on its recent efforts to provide 100 billion dollars in special drawing rights (SDRs) to climate-vulnerable countries, the International Monetary Fund (IMF) should allocate an additional 100 billion dollars in paid-in capital and redirect SDRs to MDBs, starting with the African Development Bank this month. This would be in line with the Marrakech Declaration, an initiative to reform the global financial architecture which is being developed at the request of African finance ministers.

A multi-partner fund must be established to help mitigate foreign exchange risks for private investors by providing cost-effective currency and country hedges for climate investments in Africa. Such a fund would significantly reduce the perceived risks of investing in EMDEs, even in the face of currency fluctuations.

Lastly, lenders should support the creation of a facility that accelerates existing projects and programs on the continent, especially those that preserve nature and help communities adapt to extreme weather events such as droughts, floods, and heatwaves. Multiple funders and investment instruments already operating in Africa could set up such a facility, avoiding the cumbersome process of establishing a new fund.

Progress on these five reforms has already been made. At the Summit for a New Global Financing Pact in Paris in June, Senegal secured 2.7 billion dollars from developed countries to invest in renewable energy, and Zambia struck a deal to restructure 6.3 billion dollars in debt. Meanwhile, the African Risk Capacity Group, which offers parametric insurance against natural disasters, has provided 720 million dollars in coverage for 72 million people since 2014.

We can substantially increase such assistance by quickly putting money into the Loss and Damage Fund established at last year’s COP27 climate summit in Egypt. Innovative financing measures will help African countries recover from climate disasters, build resilience to future shocks, and complete the transition to cleaner energy – all of which can bring sustainable development gains.

But the continent needs a dramatic increase in funding to reap the full benefits of climate action.

This article first appears in the Project Syndicate (PS).

PUBLISHED ON

Sep 10,2023 [ VOL

24 , NO

1219]

Fortune News | Jul 25,2026

Viewpoints | Jul 09,2022

Featured | Jan 07,2024

Radar | Dec 01,2024

Radar | Aug 07,2025

Fortune News | Apr 05,2026

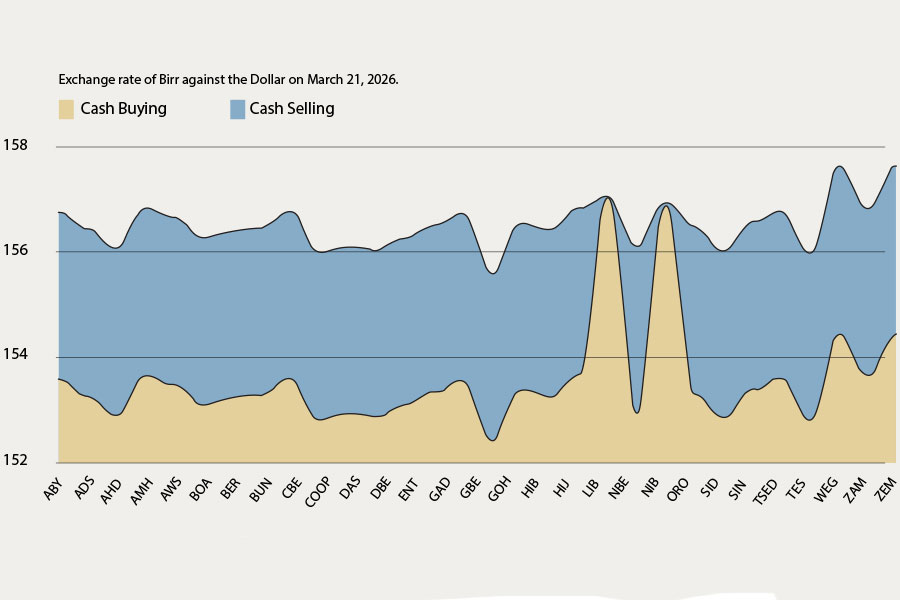

Money Market Watch | Mar 21,2026

Agenda | Apr 25,2026

Radar | Jan 10,2026

Delicate Number | Sep 10,2023

Photo Gallery | 192666 Views | May 06,2019

Photo Gallery | 182539 Views | Apr 26,2019

Photo Gallery | 179278 Views | Oct 06,2021

My Opinion | 144776 Views | Aug 14,2021

Commentaries | Jul 31,2026

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 31 , 2026

Weldu Yiheysh has not read the Pacific temperature charts. He does not need to. In Shibta District of Enderta Wereda, in...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Aug 1 , 2026 . By NAHOM AYELE

Addis Abeba University set out to win its institutional autonomy. Two years in, that...

Aug 1 , 2026 . By NAHOM AYELE

The state-owned Ethiopian Shipping & Logistics (ESL) unveiled its most ambitious...

The Ethiopian Airlines Group (EAG) will take delivery of eight Boeing 777 and Airbus...

Aug 1 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have ordered that 27 apartments at Noah Victory Apar...

Loading your updates...

Loading your updates...