Fortune News | Nov 04,2023

Aug 10 , 2024

By Tesfaye B. Lelissa (PhD)

The timeline for stabilising the Birr depends on a comprehensive and well-coordinated policy response that is urgently delivered. Learning from global experiences and insights will be crucial for the authorities as they steer clear of troubled waters, ensuring long-term economic stability and growth. Tesfaye B. Lelissa (PhD) (teskgbi@gmail.com), president of Global Bank, projects that the road ahead could be rough, but with the right strategies, Ethiopia can shine brightly on the economic stage.

Federal policymakers have transitioned the Birr towards a more flexible and market-based exchange rate system, hoping to see the currency stabilise and improve the country's economic competitiveness. For far too long, the Birr was subject to a fixed peg, resulting in an overvaluation that contributed to persistent trade deficits and foreign exchange shortages. The new system seeks to let its value be determined by supply and demand dynamics in the foreign exchange market rather than an artificial peg.

However, this transition has not been without turbulence.

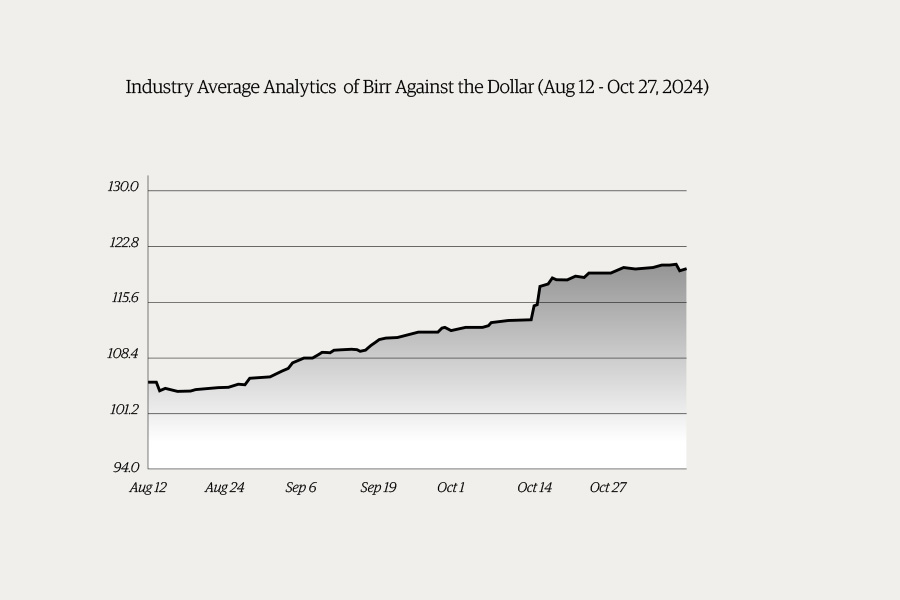

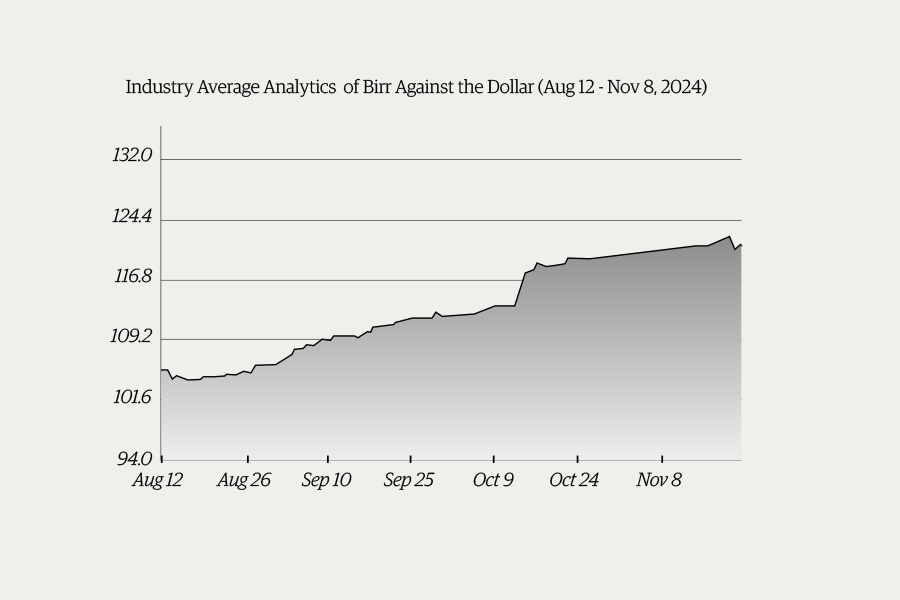

Recently, the Birr experienced a sharp depreciation, plummeting from around 58.6Br for a dollar to over 100 Br within a few weeks. While some expected this acute drop, it represents a setback in the efforts to stabilise it under the new floating regime. The initial depreciation period is formidable for the economy, posing substantial limitations until signs of stability emerge. Despite these difficulties, stabilising the Birr is crucial for addressing the long-standing trade and foreign exchange problems.

A more stable and market-responsive exchange rate can enhance export competitiveness, attract foreign direct investment (FDI), and support overall economic development.

Making definitive judgments on the appropriateness or timing of the Birr's devaluation or speculating on its long-term impact would be premature. The more relevant question should ponder when the Birr will stabilise and at what exchange rate. A combination of economic and policy factors will convolute the process.

Active intervention in the foreign exchange market will be a critical factor in stabilising the Birr. Tools such as foreign exchange auctions, capital controls, and reserve requirements can help manage currency fluctuations. The size and adequacy of the foreign exchange reserves will also play a crucial role in responding to exchange rate volatility. Countries like China and India have successfully managed their exchange rates by building substantial foreign exchange reserves to support their intervention efforts.

Beyond mobilising external resources, Ethiopia should explore ways to accumulate foreign exchange reserves, potentially through managing current account balances and attracting foreign direct investment.

Addressing underlying macroeconomic imbalances, such as high inflation and budget and trade deficits, will stabilise the Birr. Coordinating monetary, fiscal, and exchange rate policies to create a more stable and supportive macroeconomic environment should be indispensable. Structural reforms to enhance the economy's competitiveness, productivity, and export potential, similar to the experiences of Vietnam and Malaysia, would contribute to a more sustainable exchange rate. These countries have achieved more effective exchange rate regimes by aligning their exchange rate management strategies with broader macroeconomic policies, supporting their economic development priorities.

Ethiopia has explored developing a similar comprehensive policy framework through its homegrown economic reform. Effective execution of these policies is vital in the search for long-term equilibrium.

Deepening and broadening the liquidity of the foreign exchange market will be crucial to reduce the impact of speculative activities. Encouraging the participation of diverse market participants, including businesses, investors, and financial institutions, can lead to price discovery and market stability.

Improving the transparency and efficiency of foreign exchange trading platforms, as seen in developing currency futures markets in countries like South Africa and India, can also support Birr's stabilisation. These markets have provided essential price discovery mechanisms and increased the transparency of currency pricing, contributing to more efficient and stable exchange rate dynamics.

Addressing the impact of adverse external shocks, such as volatility in global commodity prices and shifts in international capital flows, and diversifying Ethiopia's trading partners and export markets, as seen in the strategies of countries like Chile and Peru, can reduce the country's vulnerability to external economic disruptions.

Chile, for instance, has proactively sought to expand its trade relationships beyond traditional partners by exploring new Asian markets, particularly China and other emerging economies. This diversification has helped it reduce its vulnerability to fluctuations in demand or prices for its primary export commodities, such as copper.

Ethiopia could emulate these strategies by actively seeking to diversify its trading partners and export markets, reducing its reliance on a few dominant markets or a narrow range of exported goods. This could involve pursuing new trade agreements and partnerships with diverse countries and regions. It could also encourage the development of non-traditional export sectors, such as manufacturing or services, to complement its reliance on primary commodity exports.

Restoring confidence in the government's ability to manage the economy and Birr's exchange rate effectively will be a tasking effort. Transparent and credible communications of the policy framework for exchange rate management, as well as measures to improve the predictability and stability of the Birr's movements, can help reduce uncertainty and speculation. The experiences of countries like Malaysia and Thailand, which have successfully overcome currency crises through effective communications and policy coordination, can provide valuable insights.

The critical question that needs to be addressed is whether the current parallel-market rate of 120 Br for a dollar can be considered the true equilibrium price. Other countries' experience with similar currency crises provides important insights. In many cases, the parallel market exchange rate has not been a reliable indicator of the currency's long-term equilibrium value.

Take Venezuela, for instance. The parallel market exchange rate for its currency, Bolivar, soared to over four million against the dollar at the height of the country's economic crisis in 2019, far exceeding the official exchange rate set by the government. In Zimbabwe during the late 2000s, the parallel market exchange rate for the Zimbabwean Dollar reached astronomical levels, reflecting the country's hyperinflationary environment and the collapse of the formal foreign exchange market. In both cases, the parallel market rates were driven by short-term imbalances between supply and demand for foreign currency, fueled by economic instability, policy distortions, and speculative activities.

These rates did not accurately capture the long-term purchasing power parity or the equilibrium exchange rate based on the countries' underlying economic fundamentals.

Lessons from these experiences suggest that the parallel market rate for the Birr is also unlikely to represent the equilibrium price. Its rate is often distorted by various market imperfections, such as capital controls, foreign currency rationing, and speculative activities, and may not accurately reflect the country's economic conditions.

Proactive policy interventions and market development efforts can help converge the official exchange rate with the equilibrium level over time.

PUBLISHED ON

Aug 10,2024 [ VOL

25 , NO

1267]

Fortune News | Nov 04,2023

Radar | Sep 08,2019

Viewpoints | Sep 06,2020

Money Market Watch | Nov 09,2024

Money Market Watch | Nov 24,2024

Commentaries | Aug 18,2024

Viewpoints | Jun 22,2024

News Analysis | Jan 05,2020

Fortune News | Sep 29,2024

Agenda | Sep 10,2022

My Opinion | 131981 Views | Aug 14,2021

My Opinion | 128369 Views | Aug 21,2021

My Opinion | 126307 Views | Sep 10,2021

My Opinion | 123925 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 5 , 2025

Six years ago, Ethiopia was the darling of international liberal commentators. A year...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jul 6 , 2025 . By BEZAWIT HULUAGER

The federal legislature gave Prime Minister Abiy Ahmed (PhD) what he wanted: a 1.9 tr...

Jul 6 , 2025 . By YITBAREK GETACHEW

In a city rising skyward at breakneck speed, a reckoning has arrived. Authorities in...

Jul 6 , 2025 . By NAHOM AYELE

A landmark directive from the Ministry of Finance signals a paradigm shift in the cou...

Jul 6 , 2025 . By NAHOM AYELE

Awash Bank has announced plans to establish a dedicated investment banking subsidiary...

Loading your updates...

Loading your updates...