Editorial | Apr 15,2023

Jun 1 , 2024.

Ethiopia appears to be mired in a vicious economic cycle - rather a negative dynamic - characterised by low productivity, high unemployment, cantering inflation and declining exports, exacerbated by reactive policymaking under Prime Minister Abiy Ahmed (PhD). In a bid to manage debt servicing obligations and inflation, the federal government has adopted an austere economic policy. However, this has only deepened the crisis.

Export revenues have declined consecutively, worsening the foreign currency crunch, while the federal government increasingly race with the private sector for credit. Security issues in several regional states - most alarming in the two largest states - further deter productivity, leading to a private sector that hires less and an economy misaligned with aesthetics-focused public spending aspiring for urban revivals, an unfathomable shift in priorities towards tourism. As federal authorities continue redirecting precious resources to projects that do not permanently alter supply dynamics, macroeconomic instability remains a persistent issue.

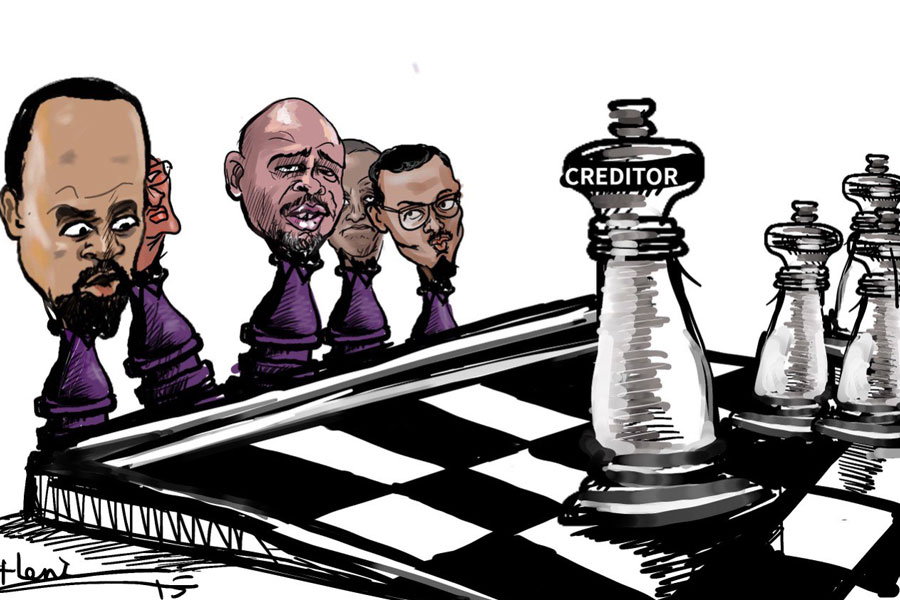

Finance Minister Ahmed Shide and State Minister Eyob Tekalegn appeared before federal legislators recently with their nine-month report with a sense of pride. They celebrated the absence of external non-concessional (commercial) loans over the past five years despite domestic debt soaring to 37 billion dollars. This would be commendable if alternative financing models had been used effectively. Yet, the lack of new infrastructure projects, essential for sustained economic growth, belies their achievement. Debt is not inherently detrimental when obtained under reasonable terms and directed towards productivity.

Ethiopia's debt servicing issues are part of a broader trend of rising public debt across Africa. It is one of 22 African economies facing debt servicing difficulties, driven by high external debt and limited fiscal space. In November 2023, its leaders agreed with official bilateral creditors for a debt service standstill from January 2023 to December 2024, providing a two-year grace period before repayments begin, followed by a three-year repayment period from 2027 to 2029.

This suspension offered short-term liquidity relief and facilitated broader debt treatment discussions, which are crucial as Ethiopia navigates its economic recovery. However, its debt servicing costs have risen, reflecting an increasing share of debt owed to private creditors. The shift heightens vulnerability to global financial conditions, particularly the rising interest rates and tightening of international financial markets since mid-2022. Higher costs associated with private debt than concessional loans exacerbate the fiscal burden.

Global interest rate hikes, elevated sovereign debt spreads, and exchange rate depreciations have further increased borrowing costs, limiting Ethiopia's access to international capital markets and complicating efforts to refinance existing debt and secure new funding. Effective implementation of broader debt restructuring under the G20 Common Framework is critical. Successful restructuring could expand Ethiopia's fiscal space, allowing for increased investment in growth-promoting sectors. However, as Finance Minister Ahmed pressed in Nairobi last week, expedited restructuring is necessary to avoid prolonged fiscal uncertainty and restore investor confidence.

Ethiopia's public debt-to-GDP ratio has surged over the past decade, driven by massive public investments and external borrowing. Despite these investments, the efficiency of public spending remains questionable. The growth benefits of debt-financed investments have not generated adequate revenue streams for debt repayment.

Ethiopia's economic growth trajectory will be crucial to its debt sustainability. Robust growth can enhance revenue generation, reducing the debt-to-GDP ratio and easing debt servicing costs. Conversely, any economic slowdown or external shocks could exacerbate fiscal vulnerabilities and heighten the risk of debt distress. Ethiopia's tax-to-GDP ratio is relatively low compared to other developing countries, hovering below 10pc, far from the 15pc threshold deemed necessary for financing Sustainable Development Goals (SDGs).

Despite efforts to enhance tax collection efficiency, inefficiencies persist. Substantial portions of potential tax revenues are lost due to exemptions, non-compliance, and administrative challenges. The tax-to-GDP ratio is expected to improve gradually if reforms in tax administration and efforts to broaden the tax base succeed. Digitalisation and automation of tax collection processes, along with measures to improve compliance, are likely to boost tax revenues. The African Development Bank (AfDB) projects the tax-to-GDP ratio could increase to around 16pc to 17pc by 2029. Assuming GDP grows at an average of six percent, this could provide the government with a fiscal space of 30 billion dollars a year in domestic taxes, enough to cover debt servicing.

Despite the anticipated GDP growth and tax revenues increase, debt servicing will remain difficult. Starting in 2027, deferred payments under the debt standstill agreement will come due, coinciding with regular debt servicing obligations, creating significant fiscal pressure. Effective debt restructuring and prudent fiscal management are essential for long-term debt sustainability. To ensure this, the G20 Common Framework for debt treatments must be successfully implemented.

Domestically, the central bank's tighter hold on new money has resulted in a noteworthy reduction in direct government borrowing, dropping by 90 billion Br from the previous year. Many economists welcome this policy direction for its likely impact on inflation. However, policymakers' shift towards mandatory bond purchases by commercial banks to cover the budgetary deficit has led to fewer investments in productive sectors by public and private entities. This can only benefit those entrenched in the informal sector or outright corruption.

While Ethiopia's total public debt-to-GDP ratio of nearly 40pc appears relatively acceptable compared to the continental average of around 60pc, it does not indicate financial stability in a country that recently experienced double-digit growth. Public-financed investments in infrastructure, primarily roads and higher education, during the long reign of the Revolutionary Democrats, paid dividends in GDP per capita, employment, and capital accumulation. The new model, yet to be fully articulated by the Prosperitans, seems to prioritise satellite towns, recreational parks, and smart cities as anchors for growth.

What would be striking about the current policy choices is the rush to revise right-of-way compensation laws, which have become cumbersome for aesthetic aspirations. Pinning hopes on tourism to resolve the macroeconomic crisis seems overly optimistic in a country where citizens are increasingly apprehensive about travelling between regions. The incumbent's economic model, if there is any available, has not addressed the foreign currency crunch, as merchandise exports continue to decline annually.

Policymakers often cite the low tax-to-GDP ratio as a cause for persistent budget deficits, now eyeing agriculture.

Undoubtedly, Ethiopia's tax-to-GDP ratio has shown substantial variability over the past decade, influenced by macroeconomic and structural factors. Improvements in tax collection, mainly through digital tools and automated systems like electronic sales register machines, have particularly enhanced VAT compliance and collection. Recent data indicate an improvement in aggregate tax revenues. In 2022/23, tax revenues grew by 35.8pc, a notable increase compared to 12.3pc the previous year, part of broader fiscal consolidation efforts that saw the fiscal deficit narrow from 4.2pc of GDP in 2021/22 to close to four percent the subsequent year.

However, Ethiopia's tax-to-GDP ratio remains below the average for many African countries, about 14.6pc of GDP. Non-resource-intensive countries have increased their tax revenues to around 17.8pc of GDP in 2022. While Ethiopia's ratio is below the continental average, continued reforms and economic growth can bolster this key fiscal indicator over the next five years. This projected increase will be crucial for financing development goals and reducing the fiscal deficit.

Introducing new taxes without overhauling the collection strategy will likely worsen the situation, considering declining productivity and revenue. Both foreign and domestic investors criticise the Revenues Ministry for underdeveloped tax collection policies, lack of expertise, and a rush to assume tax evasion. Credit limitations and economic slowdown will erode the private sector's ability to meet new tax obligations. A vicious cycle of declining investments in capital goods, less taxable income, and stagnant productivity seems likely. Systemic issues in Ethiopia's economy are rooted in a poorly articulated economic plan that no amount of new cash can resolve.

An IMF package that might accompany foreign exchange regime reform could provide temporary liquidity relief but might also plunge a large portion of the populace into deeper poverty. Prosperity's gamble to consume a large share of the economic pie while leaving crumbs for the private sector that finances it will likely prove too costly soon. The economy's path forward requires more than temporary fixes; it demands a comprehensive and well-articulated strategy that addresses the underlying structural issues. Without such a plan, macroeconomic instability will remain an enduring feature, and the vicious cycle of low productivity and high unemployment will continue to haunt Ethiopia.

PUBLISHED ON

Jun 01,2024 [ VOL

25 , NO

1257]

Editorial | Apr 15,2023

Radar | Apr 09,2022

Radar | Dec 19,2020

My Opinion | Feb 17,2024

Radar | Dec 10,2022

Fortune News | Feb 09,2019

Fortune News | Jun 10,2023

Fortune News | Aug 14,2021

Fortune News | Jul 29,2023

Radar | Jun 22,2024

My Opinion | 131819 Views | Aug 14,2021

My Opinion | 128203 Views | Aug 21,2021

My Opinion | 126147 Views | Sep 10,2021

My Opinion | 123767 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 6 , 2025 . By BEZAWIT HULUAGER

The federal legislature gave Prime Minister Abiy Ahmed (PhD) what he wanted: a 1.9 tr...

Jul 6 , 2025 . By YITBAREK GETACHEW

In a city rising skyward at breakneck speed, a reckoning has arrived. Authorities in...

Jul 6 , 2025 . By NAHOM AYELE

A landmark directive from the Ministry of Finance signals a paradigm shift in the cou...

Jul 6 , 2025 . By NAHOM AYELE

Awash Bank has announced plans to establish a dedicated investment banking subsidiary...

Loading your updates...

Loading your updates...