Fortune News | Jan 01,2022

Sep 24 , 2022

By Asseged G. Medhin

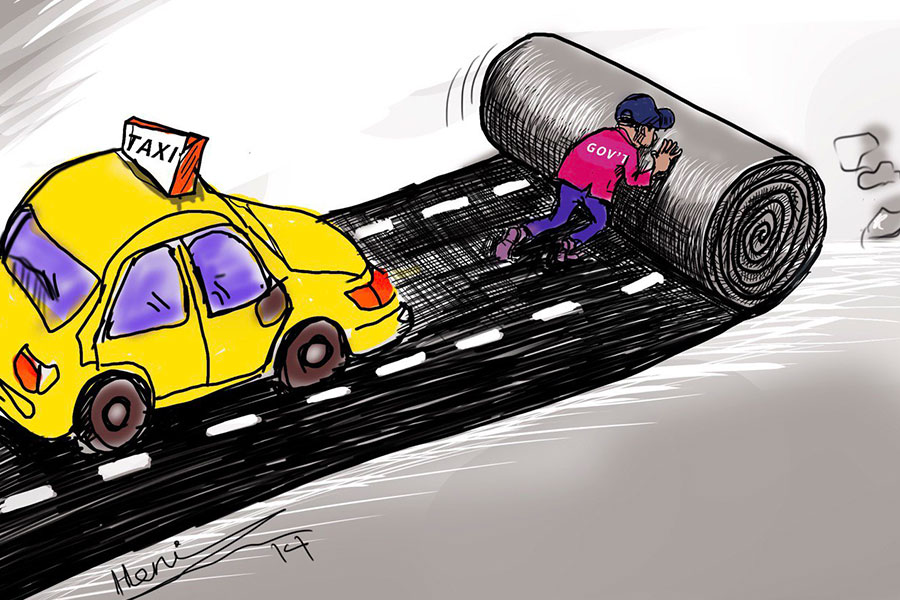

The insurance industry, through reinsurers and the regulatory body, is reducing its appetite to provide surety for contractors. This is bad news for the construction business and the economy, writes Asseged Gebremedhin, an insurance professional with over a decade of experience in finance.

As the Ethiopian insurance industry is challenged by contractors who fail to perform their contractual obligation, the National Bank of Ethiopia (NBE), has issued restrictions on issuing financial guarantee bonds. This and similar regulatory decisions create wrong assertions about the bond market, risk management and the insurance industry as a whole.

Recently, most contractors have failed to perform their contractual obligation and caused larger claims of advance payment and performance bonds. The trend, if it continues, will urge insurers to reduce their appetite for the bond market. The paradox is that for the construction industry to continue to grow and the country’s infrastructure to be developed, guarantee bonds that redistribute risk need to expand.

A good indicator is this year’s federal budget, where 787 billion Br was approved. Road construction takes up 66.2 billion Br, water and energy 24.7 billion Birr, and urban development and construction 18.9 billion Birr. The Addis Abeba City Administration has also approved 100 billion Br to hit certain targets, giving priority to infrastructure, water, road, entrepreneurship and industrial sectors. In support of primary insurers, reinsurers were supposed to have an enhanced appetite to accept mega risks with more relaxed criteria.

The Ethiopian insurance industry is supported by Africa Re, Zep Re and local Ethiopian Re, and a few other internationally-based reinsurers. The first one recently introduced enhanced criteria for domestic insurers on performance bonds and advance payment guarantees.

With diminished appetite and barriers to bond issuance, how will we satisfy the need for development projects? What would be the role of insurers in the construction industry?

After all, the share of insurance to GDP is estimated at one percent and the penetration ratio is negligible. The total asset of insurers is three-quarters of a percentage of GDP. We are also bucking the global trend where bond insurance rose nine percent in 2021 as market demand continued to increase steeply, initially due to credit concerns caused by the pandemic. This is because the performance of contractors, regardless of the outcome, should not block the appetite for the bond market. During financial crises, world insurers and reinsurers do not close their doors and walk away.

They would instead use the incident to issue different securities that allow them to retain their existing customers and attract new ones. The idea of breaking the need to have collateral for mega-projects through different insurance sureties is becoming common in the world bond market.

The rationale behind availing the insurance bonds without having collateral or with a small share of collateral on the bond value is creating strong bondage with multinational contractors willing to place their bigger ventures at a higher premium than average bond rates in the market. By designing tailor-made insurance coverage and retaining crucial bond buyers, insurers alleviate the risk associated with bonds.

The situation in Ethiopia is different. Primary insurers and reinsurance companies are developing very stringent criteria, insisting insurers hold around half the bond value in collateral. Can even grade-one contractors satisfy this criteria? The declining appetite for the bond market in a country where infrastructural development is the primary driver of growth will have detrimental effects. It will also hinder the growth of the insurance industry, which is something shareholders, executives and boards of directors should dwell on for longer.

When reinsurers and regulatory bodies become so demanding, insurers will follow, and contractors will begin to avoid risks altogether. Instead of this crisis, the insurance sector should develop a workable enhanced rate and tailor-made products since the experience and opportunity of several contractors remain valuable. The regulatory body should support such alternatives and help insurers revise directives in bond insurance. Otherwise, economic transactions will be tied up without the adequate provision of surety and end in a lose-lose scenario.

PUBLISHED ON

Sep 24,2022 [ VOL

23 , NO

1169]

Fortune News | Jan 01,2022

Editorial | Aug 20,2022

Fortune News | Jul 29,2023

Fortune News | Jul 02,2022

Featured | Sep 10,2021

Films Review | Jun 01,2019

Fortune News | Apr 26,2019

Fortune News | May 04,2024

Radar | Jul 24,2021

Featured | Jan 07,2023

My Opinion | 131819 Views | Aug 14,2021

My Opinion | 128203 Views | Aug 21,2021

My Opinion | 126147 Views | Sep 10,2021

My Opinion | 123767 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 5 , 2025

Six years ago, Ethiopia was the darling of international liberal commentators. A year...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jul 6 , 2025 . By BEZAWIT HULUAGER

The federal legislature gave Prime Minister Abiy Ahmed (PhD) what he wanted: a 1.9 tr...

Jul 6 , 2025 . By YITBAREK GETACHEW

In a city rising skyward at breakneck speed, a reckoning has arrived. Authorities in...

Jul 6 , 2025 . By NAHOM AYELE

A landmark directive from the Ministry of Finance signals a paradigm shift in the cou...

Jul 6 , 2025 . By NAHOM AYELE

Awash Bank has announced plans to establish a dedicated investment banking subsidiary...

Loading your updates...

Loading your updates...