Photo Gallery | 189162 Views | May 06,2019

May 30 , 2026. By Eyob Tesfaye (PhD) ( Eyob Tesfaye (PhD) - etesfaye48@yahoo.com - is a macroeconomist and policy analyst. )

For more than a decade, Ethiopia maintained an average headline GDP growth rate above eight percent, masking profound vulnerabilities expanding beneath the surface of the real economy. The rapid economic expansion was heavily undermined by systemic corruption surrounding state-led megaprojects, weak domestic savings, and a severe loss of international competitiveness, writes Eyob Tesfaye (PhD) - tesfayeeyob742@gmail.com - a macroeconomist. His views expressed in this commentary do not represent or reflect the positions of any organisation or institution with which he has been affiliated.

Ethiopia’s developmental state experiment was less a model of economic discipline than a response to political necessity. It offered public goods, from roads, dams, and railways to factories, as substitutes for legitimacy.

Public infrastructure became the language of power. Feasibility studies, institutional checks and financial prudence often gave way to speed, symbolism and political command. The promise was as straightforward as growth buys time, and visible projects would soften popular demands for accountability and consent, at least for a while.

Interestingly, the model itself was not born as a rigid theory. It began as an empirical account of East Asian practice and was later shaped by scholars such as Chalmers Johnson. Ethiopian policymakers borrowed the label but not the institutional foundations that made the East Asian record credible. South Korea and Japan, for instance, used directed lending alongside feedback, discipline and eventual correction.

However, and unwittingly, Ethiopia turned banks into instruments of political ambition, pushed megaprojects with weak commercial cases and drew heavily on domestic savings to finance them. The problem was not the absence of theory, inasmuch as it was the distortion of one. Finance became the centre of the experiment’s pressure point. By subordinating banking to politics, the state built a fragile system in which deposits were channelled into long-term projects with limited prospects of repayment. Banks carried short-term liabilities against long-term, but non-performing assets. Liquidity thinned, private banks were squeezed, state banks were drained, and, by the late 2010s, the tremor inside the system had become hard to ignore.

All commercial banks, but the Commercial Bank of Ethiopia (CBE), were compelled to divert more than a quarter of their deposits into bonds issued by the Development Bank of Ethiopia (DBE).

The policy stripped liquidity from the sector without providing market returns or tradable instruments. It was not merely a reserve requirement, as it was a structural distortion that deprived the private sector of credit and narrowed the banking industry’s capacity to finance productive enterprises.

State-owned enterprises absorbed even larger sums through directed loans and rolled-over bonds. The Ethiopian Electric Power Company (EEPCo) borrowed hundreds of billions without repaying a single Birr. The Ethiopian Sugar Corporation (ESC) pressed ahead with projects that failed or stalled, yet financing continued. The Corporation and Metal & Engineering Company (METEC) became drains on public resources, taking loans without matching accountability.

Under the mandate of advanced industrialisation and agricultural expansion, the Development Bank of Ethiopia (DBE) engaged in undisciplined lending practices. A distinct lack of professionalism in feasibility assessments, combined with questionable loan appraisal processes and deliberately inflated collateral valuations, led to a bypass of standard risk management practices. This systemic malfeasance directly triggered a service financial crisis, culminating in a non-performing loan ratio that exceeded 50pc.

Warnings about liquidity risks and the dangers of subordinating banks to political objectives were raised but dismissed. Board chairpersons of state-owned banks treated caution as an attack rather than a safeguard. The tremor was, therefore, not a surprise. It was the result of advice ignored, amid weakened monetary discipline. Banks were forced to extend credit without sufficient consideration for repayment capacity.

Monetary expansion accelerated, inflationary pressures mounted, and the National Bank of Ethiopia’s (NBE) ability to control money supply was undermined. What looked like development finance increasingly resembled a transfer of risk from state projects to the financial system.

The Commercial Bank of Ethiopia (CBE) became the main casualty. Long regarded as the backbone of the financial sector, for mobilising over 80pc of the country's finance, it was turned into a sacrificial institution. Its liquidity was drained, and its balance sheet was weighed down by loans to state-owned enterprises that were unlikely to be recovered on standard terms. Its solvency came to depend on the government’s willingness to roll over obligations indefinitely.

The foreign-exchange crisis deepened the damage. Reserves were depleted, the parallel market expanded, and the official exchange rate lost credibility. By 2018, CBE had been hollowed out by liquidity shortages and paralysed by foreign-currency scarcity. Had the Bank failed, the shock would have spread across the system, trembling the wider economy, which also showed the same imbalance.

Although its expansion was real, the economy rested on fragile foundations. Indeed, it maintained average GDP growth above eight percent for more than a decade, but the headline figures concealed structural weakness. Corruption flourished around state-led projects, inflation eroded household purchasing power, savings were weakened, and competitiveness suffered.

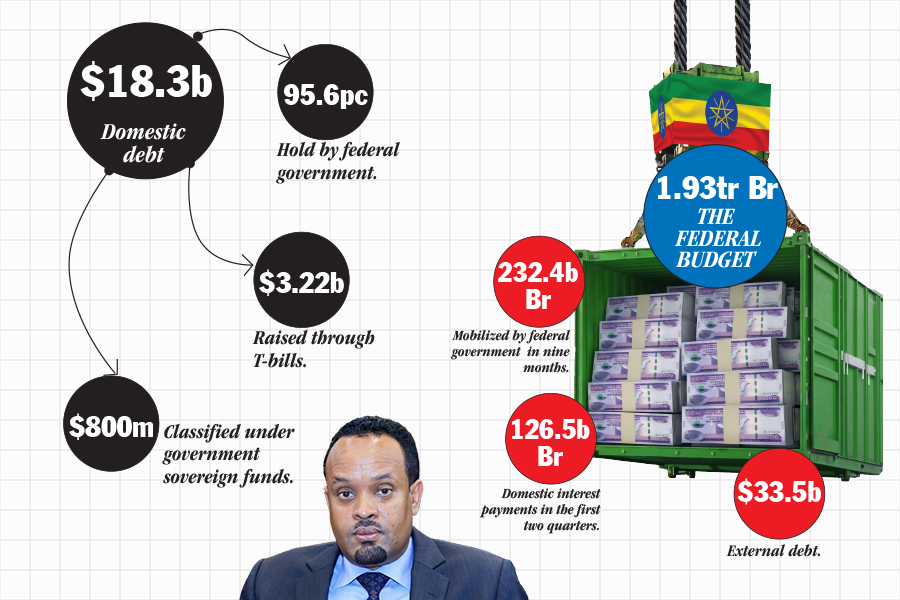

Debt mismanagement added to the pressure. Obligations were rolled over instead of resolved, creating a debt overhang that constrained growth. By 2025, external debt reached 33.3 billion dollars. That level may appear moderate by global standards after restructuring, but the composition and service burden left the economy vulnerable to recurring stress.

By 2018, the banking industry was on the verge of an abyss, forcing the new Administration to take corrective measures to prevent a collapse. Liquidity injections kept CBE afloat, and the decisive step came when more than 900 billion Br of liabilities were assumed through fiscal measures. This was a rescue operation designed to absorb a systemic shock, demonstrating that institutional safeguards, though delayed, could still function when the cost of inaction became too large.

Policy reforms, such as restructured and prudential limits, helped CBE regain some footing. At the height of the crisis, the Bank’s foreign-exchange liability was 400pc above its capital base, far beyond limits under the Central Bank’s open position directive. More than liquidity, correcting that imbalance required structural reform and tighter supervision.

However, the whole episode left behind a crucial lesson that subordinating finance to politics is not development but an utter distortion. Banks cannot be treated as captive vaults, and debt cannot be rolled over indefinitely without consequence. Directed lending to state firms helped build visible monuments, but it weakened institutions, undermined monetary control and left the financial sector exposed.

PUBLISHED ON

May 30,2026 [ VOL

27 , NO

1361]

Photo Gallery | 189162 Views | May 06,2019

Photo Gallery | 178933 Views | Apr 26,2019

Photo Gallery | 175518 Views | Oct 06,2021

My Opinion | 141277 Views | Aug 14,2021

Jun 6 , 2026

For a political veteran as controversial as Getachew Reda, last week's national elect...

May 30 , 2026

Tomorrow, millions of Ethiopians are expected to vote in the seventh national electio...

May 23 , 2026

An International Monetary Fund (IMF) team has spent weeks in Addis Abeba conducting t...

May 16 , 2026

The federal budget tells a troubling story about inflation, debt and reform. The prob...

Loading your updates...

Loading your updates...