Photo Gallery | 187583 Views | May 06,2019

May 23 , 2026.

An International Monetary Fund (IMF) team has spent weeks in Addis Abeba conducting the fifth review of the macroeconomic reform programme it backs in Ethiopia. Its checklist would be familiar and hard.

Its experts demand to see a fuller floating of the Birr in the foreign-exchange market, a phased withdrawal of direct state subsidies and much stronger efforts to raise domestic taxes. In Ethiopia, as elsewhere, such prescriptions mean weaker currencies, faster inflation and a higher cost of living. Kenya’s experience, where anger over tax measures helped ignite an urban insurrection, warns governments trying to extract more revenue from weary households.

Particularly in a country where society is polarised, the political order fragmented, and the incumbents’ legitimacy always contested, Ethiopia is a difficult place for such prescriptions. Pushing painful measures on an aggravated public could carry consequences beyond the budget. Yet policymakers face fiscal ambition and economic reality.

The closest dollar-denominated benchmark for real GDP in 2024 was about 120 billion dollars, in constant 2015 prices. Nonetheless, the tax take remains among the weakest in Africa. This is a background to a proposed amendment to the tax administration proclamation, almost a decade after the current law came into force. However, the bill is not an overhaul as it only adds provisions, clarifies ambiguities, and codifies practices already applied through directives, internal instructions, and administrative practices.

Its timing is deliberate as Prime Minister Abiy Ahmed’s administration wants higher domestic revenue. Expanding the tax base, introducing new taxes, and raising the tax-to-GDP ratio have become the main drivers as financing pressures tighten.

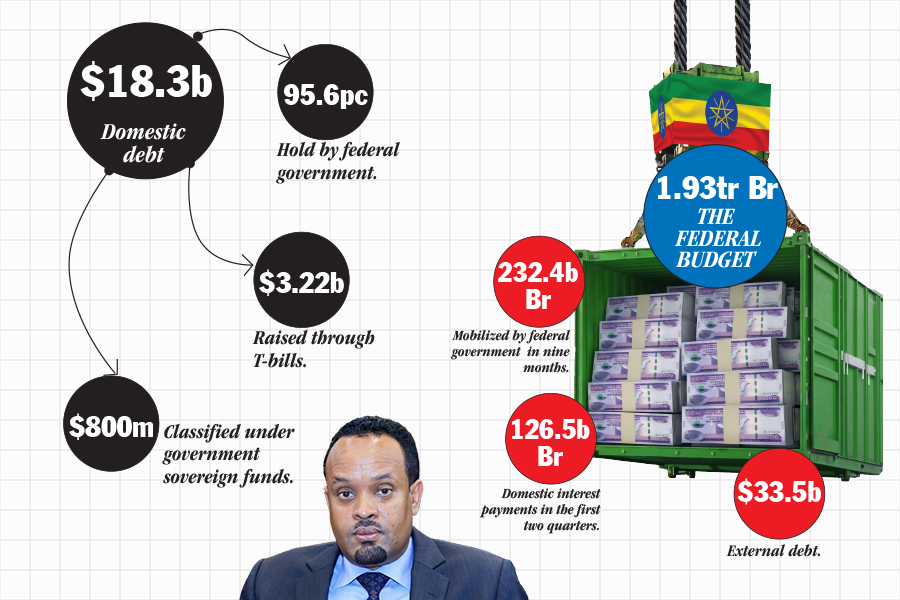

According to data from the National Bank of Ethiopia (NBE), the tax-revenue-to-GDP ratio fell to 7.1pc in 2023/24, from 7.9pc a year earlier and 8.8pc in 2021/22. An IMF-linked estimate put income-tax revenue at only 2.9pc of GDP in 2024. With external borrowing constrained, subsidies costly and debt obligations heavy, tax revenue is the state’s main fiscal prop.

The federal government collected about 720 billion Br in taxes in 2024/25, a “record” increase in nominal terms. But the figure says less than it seems. Inflation, exchange-rate movements and customs-linked receipts can inflate Birr collections. The burden remains in the high single digits of GDP, while federal receipts have expanded faster than the economy’s capacity.

On paper, the strategy appears to have logic. Ethiopia needs more domestic revenue to finance services and borrow less. It has produced gains. Federal tax mobilisation increased sharply in 2024/25, with federal and regional collections exceeding one trillion Birr. The full-year target was 1.5 trillion Br, split between 900 billion Br for the federal government and 600 billion Br for regional administrations.

The first half of 2024/25 gives the clearest picture. The Ministry of Revenues reported collecting more than 451 billion Br, including 247.7 billion Br from domestic taxes and 203.8 billion Br from export trade duties and taxes. Federal tax officials claimed this was 110pc higher than a year earlier.

In the first quarter of 2024/25, revenue and grants reached 177.2 billion Br. Domestic revenue was 165.4 billion Br, and tax revenue was 153.7 billion Br, accounting for 93pc of domestic revenue. Indirect taxes contributed 118.4 billion Br, foreign-trade taxes 83 billion Br, domestic taxes 35.4 billion Br and direct taxes 35.3 billion Br. Within direct taxes, personal income tax brought in 11.8 billion Br and business income tax 19.3 billion Br. Revenue and grants execution reached 31pc of the annual plan, while budget execution was 22.7pc, uncovering that spending lagged mobilisation. Collections then increased from 153.7 billion Br in the first quarter to more than 451 billion Br by midyear.

The system still relies heavily on indirect and trade-related taxes rather than direct taxation. At midyear, domestic taxes of 247.7 billion Br were only modestly above the 203.8 billion Br collected from export trade duties and taxes. That leaves the Treasury exposed to import cycles, customs performance and macroeconomic shocks.

Are rising nominal collections evidence of reform, or mostly the outcomes of inflation and exchange-rate change?

The federal government acknowledged this in October 2024, publishing its first strategy for National Medium-Term Revenue through to 2027/28. The plan seeks to reverse the tax-to-GDP decline and lift revenue by a cumulative 6.9 percentage points of GDP. Of that, three percentage points would come from tax policy measures, 2.9 percentage points from administrative improvements and one percentage point from macroeconomic reforms.

The direction could be defensible, but the method remains contested. Citizens and financial experts criticise aggressive taxation on households squeezed by inflation and living costs. Recent fiscal laws lean on new collection mechanisms and tougher penalties. The danger is that enforcement looks less like compliance and more like revenue hunting.

One controversial provision in the bill tabled now bars taxpayers from submitting new evidence during complaints, appeals or tax revisions if documents were not presented during the initial assessment. If late evidence materially changes the liability, taxpayers could face a penalty equal to one-fifth of the revised obligation. Officials at the Ministry of Finance argue that late documents prolong disputes and delay proceedings. The purpose seems to be to bring administrative certainty, while the problem remains with procedural fairness.

Valid documents should be reviewed because they are valid, not rejected for being late. Taxpayers may miss deadlines without negligence. Records can be delayed, institutions slow, and assessments complicated. If legitimate evidence changes an assessment, the tax authority should reassess the liability rather than dismiss the material or punish the taxpayer. The penalty tilts the system toward the state, limiting safeguards and widening official leverage. At a minimum, it should be reduced to reflect taxpayers’ practical difficulties.

The bill also creates a mediation system before disputes reach the Tax Appeal Commission. In principle, mediation could settle cases faster. In practice, crucial questions remain unanswered, including a lack of clarity about who qualifies as a mediator. The Ministry of Finance states institutions may serve, but the bill leaves appointments to the tax authority. A mediator chosen by one disputing party would no doubt struggle to appear neutral.

Costs are also shifted to taxpayers, without being shared. If mediation is independent, its financing should show it.

Why is mediation needed if the tax authority is applying the law correctly?

Another provision targets businesses that fail to issue receipts, nearly doubling existing fines. Granted, compliance is necessary so long as enforcement is legitimate. But excessive fines can produce perverse incentives. When punishment is too severe, businesses and tax officers may engage in informal bargaining, with bribes used to avoid penalties. A system built on fear can weaken compliance and encourage corruption.

Collections are rising, but legal and administrative burdens are increasingly falling on ordinary firms and consumers. Improving compliance, aligning disputes with international standards, and modernising tax administration remain sound. But laws that look efficient in statute books can become arbitrary at the counter, on the shop floor, or at the tax office.

Undoubtedly, Ethiopia needs a larger, fairer and more reliable tax base. It also needs public trust, in which citizens pay more willingly when revenue is used for services and procedures that treat them as taxpayers, not targets. A reform built mainly on restrictions, penalties and state discretion may lift collections for a time. It is less likely to build the voluntary compliance that the Treasury will need long after the IMF team leaves Addis Abeba.

PUBLISHED ON

May 23,2026 [ VOL

27 , NO

1360]

Photo Gallery | 187583 Views | May 06,2019

Photo Gallery | 177608 Views | Apr 26,2019

Photo Gallery | 174032 Views | Oct 06,2021

My Opinion | 140306 Views | Aug 14,2021

May 23 , 2026

An International Monetary Fund (IMF) team has spent weeks in Addis Abeba conducting t...

May 16 , 2026

The federal budget tells a troubling story about inflation, debt and reform. The prob...

May 9 , 2026

The Ethiopian state appears to have discovered a fiscal instrument that is politicall...

May 2 , 2026

By the time Ethiopia's National Dialogue Commission (ENDC) reached the end of its fir...

Loading your updates...

Loading your updates...