Radar | Oct 06,2024

Aug 29 , 2020.

For some time now, those at the helm of multilateral financial institutions have felt like they have an ideological ally in Ethiopia where economic management is concerned. Ethiopia has been on the right economic track, at least according to the International Monetary Fund (IMF). The improving consensus is mainly because of liberal economic reform efforts of Prime Minister Abiy Ahmed’s (PhD) administration.

Industries are opening for the private sector, and major state-owned enterprises are in the process of being transferred to private hands in a third-generation phase of privatisation. The third component of the Bretton Woods’ Holy Trinity of policy recommendations - a flexible exchange rate regime, which would deal a blow to capital account control – also seems to be on the horizon.

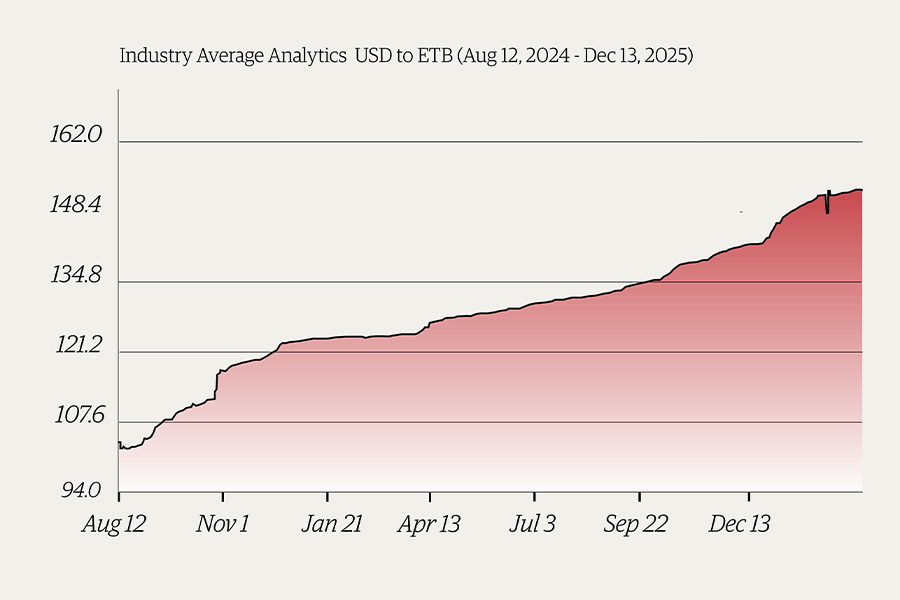

The creeping depreciation of the Birr against a basket of major currencies is one of the most perceptible changes that has pointed in this direction. There has not been a time when the value of the Birr has not been edging down; but it has been doing so at a steeper rate over the past two years.

In the five years since 2012, the value of the Birr against the dollar fell by over a third. In late 2017, the currency was devalued by 15pc against a basket of major currencies. After a short period of relative stability, beginning in November 2019, there has been a precipitous decline. Within less than a year, the Birr decreased by 22pc from its nominal exchange rate value of 28 Br against the dollar.

Together with a recent bill by the central bank that allows local banks to borrow directly in foreign currency, all of these are bold steps against longstanding capital account controls and a rigid exchange rate regime.

Indeed, Yinager Dessie (PhD), governor of the central bank, has indicated that Ethiopia is not many years away from removing the leash - where the Bank intervenes whenever needed - from its exchange rate regime, leaving the value of the Birr to the mercy of the market.

It is only standard that the IMF would commend these developments as a step in the right direction. Consistent in its call for a “market-clearing exchange rate,” it has argued that the current regime reduces access for the private sector, lessens confidence in the currency and diverts resources away from the formal economy because it inevitably creates a parallel exchange market. These are all valid points that should not be brushed aside.

Together with the World Bank, the IMF is consistent and determined in railing against the status quo in the exchange rate regime for its inability to reflect the value of the Birr in real terms. Its wise men and women believe the existing exchange rate policy leads to limited capital inflows and inefficient allocations of foreign currency to economic sectors and players. They create an economic environment of shortage, constraints and a quota system.

Fair enough. Too many Birr are being exchanged for too few dollars. The parallel market is a testament to this. It works according to the laws of supply and demand, to a more considerable degree, as a result of the absence of a central controlling entity.

The market left to itself does allocate foreign currency to those that are the most productive and value it the most - theoretically. When resources accrue to those that are productive, the economy becomes more competitive, and capital flows into the country, because investors are more confident they could take profits out. The value of the Birr remains more stable.

This happens in ideal circumstances. But Ethiopia’s economy is not ideal. An exchange rate that reflects the needs of the market to a higher degree - thereby clearing it - may not necessarily entail capital inflows or currency stabilisation. Neither could it guarantee the competitive stances of Ethiopia's exports.

Those who are worried that the liberalisation of foreign exchange may fall short of its intended goals need to be heard. Ethiopia’s economy suffers from deep structural problems. It is also the case that there is not nearly enough information about transactions in goods and services and adequate monetary policy instruments to effectively manage the exchange market.

The more flexible it gets, several factors would determine the viability of the forex market, including the level of growth, demand, prices in exports, inflation and effective monetary policy, or lack thereof. All except the latter are prey to the country’s production capacity and aggregate demand.

What defines Ethiopia's economic reality is severe limits in its productive capacity and lack of competitiveness in the global market. It buys far more from others than what it can sell them. There are advantages to the stability of the Birr only in as far as the country can continue to be less dependent on imports, improve its exports and reduce its vulnerability to the fluctuations of the international market.

But where Ethiopia’s foreign currency reserve remains subject to the vagaries of the world market in agriculture exports, making the exchange rate too flexible could create more problems than help address structural economic ailments.

The only component that will be left in the authorities' toolbox as the flexibility of the exchange rate increases is indirect monetary policy instruments, including interest rates. Only around 35pc of the population is banked, in 2017, and the majority of savings and borrowing continues to be carried out outside of financial institutions, according to the World Bank. Neither does it help that a third of Ethiopia’s economy is estimated to be informal.

With a significant part of the economy standing outside of its influence, the central bank would not be that successful in effecting change on the exchange market through indirect policy instruments. It would thus truly be floating, without any meaningful controls left to the central bank. It should not be lost on advocates that a free market does not necessarily mean a market free of the state.

The state, however, is not doing a good job of managing the exchange market to ensure allocations of forex for an optimum return in the economy. For all that is evident, the forex regime is mismanaged currently, giving undue leverage to the bureaucrats at the central bank to determine who could make it from rags to riches. Access to forex in Ethiopia today becomes the indispensable key to succeeding spectacularly.

The status quo begs for change. The course of change would rather be pragmatic in its approach, but not losing sight of its strategic goals of creating an exchange market that functions based on demand and supply.

Although in a different context and stated long ago, the words of Dominique Strauss-Kahn (PhD), former managing director of the IMF, hit the message home.

“We must be pragmatic," he said in a speech in 2011, referring to labour markets in that instance. "We must get past the binary and unhelpful contrast between 'flexibility' and 'rigidity'."

It was a speech that even contented one of the institution’s famous detractors, Joseph Stieglitz, for softening long-held views of “market fundamentalism.”

One of the IMF’s objectives has been creating “global monetary cooperation.” It is not a means to arrive at an end. It is an end unto itself, like reducing word poverty. At best, this means that the institution would attempt to harmonise recommendations on exchange regimes with developmental objectives of a country. At worst, and this is the case with having policy absolutes, it is insisting on these recommendations even when it is counterproductive.

No doubt, under ideal circumstances, flexibility is the right policy. It should be the long-term aim of Ethiopia, because it offers market dynamism and has been shown to improve competitiveness. But it should not be taken as a solution to currency instability or the forex shortage in and of itself. It is instead a complement to more comprehensive economic liberalisation that succeeds in addressing the economy's dependence on imports, lack of diversified export structures and limited financial inclusion.

The flexibility of the exchange rate of the Birr would instead be attached to the rate at which the country addresses these structural failings under a politically different context. It could make a whole different impact where a political force takes such delicate and consequential policy moves with a clear and unambiguous electoral mandate.

PUBLISHED ON

Aug 29,2020 [ VOL

21 , NO

1061]

Radar | Oct 06,2024

Radar | Jun 20,2020

Agenda | Jan 18,2020

Fortune News | Dec 04,2021

Fortune News | Apr 09,2022

Agenda | Oct 13,2024

Radar | Oct 08,2022

Money Market Watch | Dec 13,2025

Fortune News | Nov 18,2023

Commentaries | Feb 25,2023

Photo Gallery | 191213 Views | May 06,2019

Photo Gallery | 181007 Views | Apr 26,2019

Photo Gallery | 177675 Views | Oct 06,2021

My Opinion | 143298 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 12 , 2026 . By BEZAWIT HULUAGER

When a WhatsApp notice told about 60 households at a gated community on the outskirts...

Jul 12 , 2026 . By BEZAWIT HULUAGER

The Addis Abeba City Administration has begun charging a municipal tax on every hotel...

Jul 12 , 2026 . By BEZAWIT HULUAGER

Bahir Dar International Stadium is nearing completion, and the people building it say...

Jul 12 , 2026 . By BEZAWIT HULUAGER

Federal regulators of the coffee sector are preparing a fund to shield growers and ex...

Loading your updates...

Loading your updates...