My Opinion | Dec 24,2022

Jan 28 , 2023

By Joseph E. Stiglitz

There is overwhelming evidence that the primary source of inflation was pandemic-related supply shocks and shifts in the demand pattern, not excess aggregate demand, and indeed not any additional demand created by pandemic spending, argues Joseph E. Stiglitz, a Nobel laureate in economics and a professor at Columbia University, in this commentary provided by Project Syndicate (PS).

Despite favourable indices, it is too soon to tell whether inflation has been tamed. Nonetheless, two clear lessons have emerged from the recent price surge.

First, economists’ standard models – especially the dominant one that assumes the economy always to be in equilibrium – were effectively useless. And, second, those who confidently asserted that it would take five years of pain to wring inflation out of the system have already been refuted. Inflation in the US has fallen dramatically, with the December 2022 seasonally adjusted consumer price index coming in just one percent above that for June.

There is overwhelming evidence that the main source of inflation was pandemic-related supply shocks and shifts in the demand pattern, not excess aggregate demand, and certainly not any additional demand created by pandemic spending. Anyone with any faith in the market economy knew that the supply issues would be resolved eventually; but no one could possibly know when.

After all, we have never endured a pandemic-driven economic shutdown followed by a rapid reopening. That is why models based on past experience proved irrelevant. Still, we could anticipate that clearing supply bottlenecks would be disinflationary, even if this would not necessarily counteract the earlier inflationary process immediately or in full, owing to markets’ tendency to adjust upward more rapidly than they adjust downward.

Policymakers continue to balance the risk of doing too little versus doing too much. The risks of increasing interest rates are clear: a fragile global economy could be pushed into recession, precipitating more debt crises as many heavily indebted emerging and developing economies face the triple whammy of a strong dollar, lower export revenues, and higher interest rates. This would be a travesty. After already letting people die unnecessarily by refusing to share the intellectual property for COVID-19 vaccines, the United States has knowingly adopted a policy that will likely sink the world’s most vulnerable economies. This is hardly a winning strategy for a country that has launched a new cold war with China.

Worse, it is not even clear that there is any upside to this approach. In fact, raising interest rates could do more harm than good, by making it more expensive for firms to invest in solutions to the current supply constraints. The US Federal Reserve’s monetary-policy tightening has already curtailed housing construction, even though more supply is precisely what is needed to bring down one of the biggest sources of inflation: housing costs.

Moreover, many price-setters in the housing market may now pass the higher costs of doing business on to renters. And in retail and other markets more broadly, higher interest rates can actually induce price increases as the higher interest rates induce businesses to write down the future value of lost customers relative to the benefits today of higher prices.

To be sure, a deep recession would tame inflation.

But why would we invite that?

Fed Chair Jerome Powell and his colleagues seem to relish cheering against the economy. Meanwhile, their friends in commercial banking are making out like bandits now that the Fed is paying 4.4pc interest on more than three trillion dollars of bank reserve balances – yielding a tidy return of more than 130 billion dollars annually.

To justify all this, the Fed points to the usual bogeymen: runaway inflation, a wage-price spiral, and unanchored inflation expectations.

But where are these bogeymen?

Not only is inflation falling, but wages are increasing more slowly than prices (meaning no spiral), and expectations remain in check. The five-year, five-year forward expectations rate is hovering just above two percent – hardly unanchored.

Some also fear that we will not return quickly enough to the two percent target inflation rate. But remember, that number was pulled out of thin air. It has no economic significance, nor is there any evidence to suggest that it would be costly to the economy if inflation were to vary between, say, two percent and four percent. On the contrary, given the need for structural changes in the economy and downward rigidities in prices, a slightly higher inflation target has much to recommend it.

Some also will say that inflation has remained tame precisely because central banks have signaled such resolve in fighting it. My dog Woofie might have drawn the same conclusion whenever he barked at planes flying over our house. He might have believed that he had scared them off, and that not barking would have increased the risk of the plane falling on him. One would hope that modern economic analysis would dig deeper than Woofie ever did.

A careful look at what is going on, and at where prices have come down, support the structuralist view that inflation was driven mainly by supply-side disruptions and shifts in the pattern of demand. As these issues are resolved, inflation is likely to continue to come down.

Yes, it is too soon to tell precisely when inflation will be fully tamed. And no one knows what new shocks await us. But I am still putting my money on “Team Temporary.” Those arguing that inflation will be largely cured on its own (and that the process could be hastened by policies to alleviate supply constraints) still have a much stronger case than those advocating measures with obviously high and persistent costs but only dubious benefits.

PUBLISHED ON

Jan 28,2023 [ VOL

23 , NO

1187]

My Opinion | Dec 24,2022

Featured | Jan 01,2023

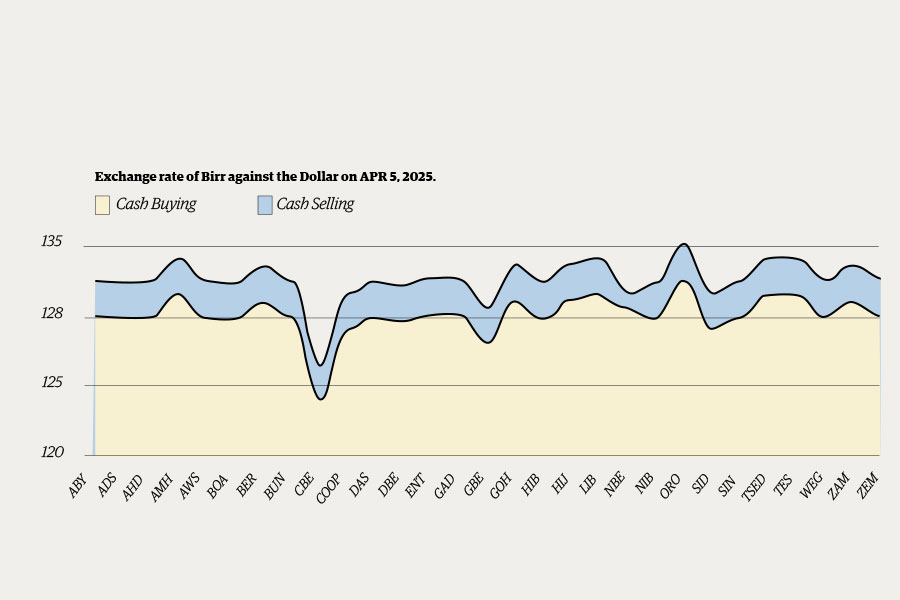

Money Market Watch | Apr 27,2025

Radar | Sep 02,2023

Viewpoints | Jul 18,2020

View From Arada | Jul 15,2023

Agenda | Jun 25,2022

Exclusive Interviews | Jan 24,2023

Agenda | Dec 28,2019

Obituary | Mar 21,2020

Photo Gallery | 191953 Views | May 06,2019

Photo Gallery | 181706 Views | Apr 26,2019

Photo Gallery | 178430 Views | Oct 06,2021

My Opinion | 143969 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jul 25 , 2026 . By BEZAWIT HULUAGER

Global Bank's Board of Directors have overhauled top management, after suspending sev...

Jul 25 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have overturned the National Lottery Administration...

Jul 25 , 2026 . By NAHOM AYELE

A newly enacted regulation by the Council of Ministers lets eligible producers pledge...

Jul 25 , 2026 . By FITSUM TADESSE

A fuel tanker carrying tens of thousands of litres was confiscated after its driver a...

Loading your updates...

Loading your updates...