Fortune News | Nov 03,2024

May 27 , 2023.

Tauted as a somnolent giant, Ethiopia’s financial scene now stirs, roused by favourable demographics, geostrategic position and untapped markets, offering a tantalising prospect for growth. An incessant swell in GDP and a population bulge that is youthful and vibrant frames this narrative, yet the devil is in the detail.

A mere 35pc of Ethiopia’s adult populace in 2017, according to the World Bank’s Global Findex Database, possessed saving accounts with banks. Recent years have seen a transformative shift, especially in the realm of digital banking, despite the uneven terrain of development and access.

Today, one branch of a financial service company caters to just over 8,000 people. With 31 banks licensed by the National Bank of Ethiopia (NBE) and operating 10,968 branches, the financial firms have corralled over two trillion Birr deposits by March of this year, marking a 60pc surge from the previous year. In 2022/23, total deposit mobilisation soared to 2.059 trillion Br, which rose from 1.2 trillion Br two years ago. In the nine-month period of the current fiscal year, they have registered an increase of 354.3 billion Br, indicating a 20.8pc growth.

The state-owned banks, like the Development Bank of Ethiopia (DBE), have the lion’s share in the financial expanse, boasting a growth rate of 355.8pc—albeit from a modest base—piling 3.1 billion Br in deposits. Yet, the undisputed king remains the Commercial Bank of Ethiopia (CBE), which surpassed one trillion Birr in deposits by March 2023, a 13.8pc uptick from the year before.

Private banking, however, is no underdog.

The banking industry appears robust and dynamic, with the growth of private banks and the emergence of new players stimulating competition. The industry is marked by new entrants, with several of them beginning operations over the past two years, such as Tsedey, Shebelle, Siinqee, and Amhara banks. Tsedey Bank, for instance, mobilised an impressive 31.3 billion Br within its first year in business. This suggests that different banks may be following different strategies, facing various levels of competition, or operating in different market segments.

The private banks show a variety of growth paces, with banks like Enat and ZamZam showing higher growth rates. Others have grown moderately, and a few have even contracted slightly. The Cooperative Bank of Oromia (Oromia Coop) witnessed a steep 51.3pc decline in loan collections from cooperatives. The state-owned banks also saw a 5.1pc decrease, indicating an inherent vulnerability and constraints alarming the banking industry.

The private banking sector has contributed robustly to deposit mobilisation and loan disbursements. Awash Bank, a private contender, exemplifies this trend with a 37.7pc growth to 168.4 billion Br deposits, manifesting the increasing diversity within Ethiopia’s banking ecosystem.

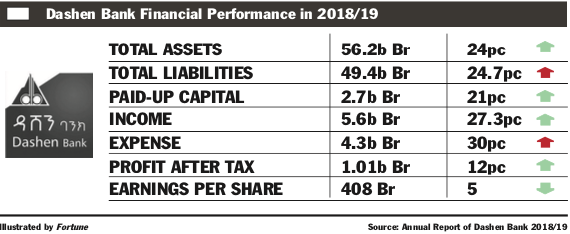

Private banks made up the bulk of loan collections during the nine months ending in March 2023, amassing 220.3 billion Br—an 82.7pc increase from the preceding year. Dashen Bank, a private stalwart, epitomises this trend with a 116.4pc growth in loan collections, reaching 27.9 billion Br.

Yet the shadow of potential structural risks lurks beneath the rosy growth picture. Focusing on a narrow band of sectors, mainly agriculture, which saw a quadrupling of credit to 41.6 billion Br, signifies a concentration of risks. A slump in these sectors could trigger a cascade of loan defaults, hurtling banks into a crisis.

The dominance of the two state-owned banks, despite a decline in the share of outstanding loans over time from 61.1pc in March 2021 to 47.8pc this year, could potentially imperil the industry. Their financial health and corporate governance are critically intertwined with the financial sector’s stability. Should either falter, it could spark a banking crisis of considerable magnitude.

Though a catalyst for economic growth, private-sector lending has its perils, too. As history has shown, a surge in credit could dilute lending standards, inflating a dangerous bubble whose burst could wreak havoc.

The sudden surge in loans for agriculture to 100 billion Br may have aligned with the aspirations of the Prosperitians to boost productivity, but it also brings its risks. The sector is susceptible to weather vagaries, fluctuating global prices and conflict-induced productivity drops.

The mounting competition in the banking industry, while catalysing change and cost reduction, could destabilise the industry if banks fail to carve out a strong market position. The need for adequate safeguards against liquidity crunches for more minor, less-established banks is paramount as the upward trend of non-performing loans (NPLs) to 5.4pc of the 1.8 trillion Br in stock of outstanding loans should serve as a red flag. With the potential to erode asset quality and destabilise the financial system, this should be a concern that further exacerbates the burgeoning interconnectedness of the financial sector and the consequent cybersecurity threats.

As digitisation sweeps across banking services, an invulnerable cybersecurity infrastructure is crucial to fending off potential cyber threats that could inflict substantial financial losses and erode public trust.

The Ethiopian financial sector’s isolation from global money markets is a double-edged sword. While it shields the industry from global financial shocks, it simultaneously stifles access to international capital. Ethiopia`s banks need to navigate the delicate equilibrium between protecting domestic financial stability and reaping the benefits of global financial integration as the world grows increasingly interconnected.

The industry is grappling with the risk of foreign exchange exposure. A sizeable proportion of its loans is tied to international trade; any significant depreciation of the Birr against foreign currencies could incur heavy losses. The share of global trade from total outstanding loans may have slightly dropped to 16.4pc this year from nearly 19pc last year and 15.5pc the previous year. Its aggregate allocation was consistently upward from 189.8 billion Br in March 2021 to 274.9 billion Br in the same period the following year and a little over 300 billion Br this year.

Striking a balance in maintaining a foreign currency portfolio will thus be a daunting yet critical task for bank executives.

While the growth story of Ethiopia’s banking sector paints an optimistic picture, the narrative is nuanced with complex interplays of risk and reward, pointing to a sector undergoing a period of dynamic changes. This underlines the imperative need for regulatory vigilance and proactive risk management strategies at the corporate level.

The overarching macroeconomic climate adds another layer of complexity. The current political instability and uncertainty loom as considerable risks over the financial sector. While banks might not be able to influence this development directly, they need to formulate strategies to weather the impacts of these risks, which include economic downturns and political crises.

The tableau of Ethiopia’s banking sector is one of thrilling potential, interspersed with the intricate challenges of a dynamic and rapidly evolving market. From systemic risks to the need for effective regulatory vigilance and sectoral diversification, the terrain requires deft navigation and prudent strategy. As the financial giant stirs, the hope is that it rises, not merely to awaken but to shine.

PUBLISHED ON

May 27,2023 [ VOL

24 , NO

1204]

Fortune News | Nov 03,2024

Radar | Jan 09,2021

Viewpoints | May 18,2019

Radar | Oct 28,2023

Fortune News | Feb 15,2020

Fortune News | Jun 04,2022

Radar | Oct 23,2023

Fortune News | Mar 26,2022

Commentaries | Apr 24,2021

Radar | Oct 16,2021

My Opinion | 131819 Views | Aug 14,2021

My Opinion | 128203 Views | Aug 21,2021

My Opinion | 126147 Views | Sep 10,2021

My Opinion | 123767 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 6 , 2025 . By BEZAWIT HULUAGER

The federal legislature gave Prime Minister Abiy Ahmed (PhD) what he wanted: a 1.9 tr...

Jul 6 , 2025 . By YITBAREK GETACHEW

In a city rising skyward at breakneck speed, a reckoning has arrived. Authorities in...

Jul 6 , 2025 . By NAHOM AYELE

A landmark directive from the Ministry of Finance signals a paradigm shift in the cou...

Jul 6 , 2025 . By NAHOM AYELE

Awash Bank has announced plans to establish a dedicated investment banking subsidiary...

Loading your updates...

Loading your updates...