Money Market Watch | Aug 11,2024

The increase in the informal flow of foreign currency could be unyielding. However, banks and fintech firms rush to avail digital remittance platforms, positioning themselves to boost inflow by significantly cutting transfer fees. It is a new development converging with the expansion of an active parallel market abroad, becoming the preferred source of foreign currency for businesses unable to secure forex from the local market.

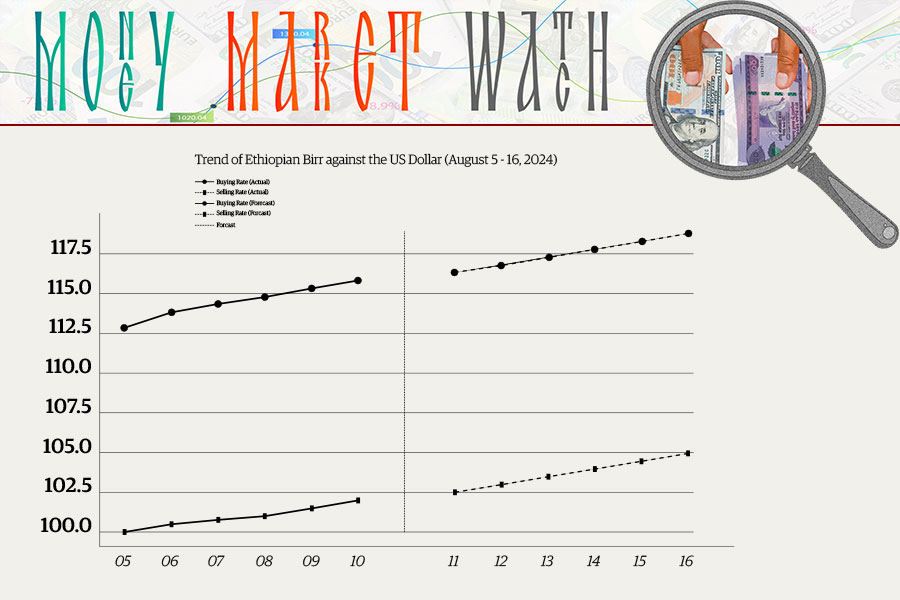

Those operating in the parallel markets abroad trade a dollar for over 65 Br, an amount 10 Br less in the streets of Addis Abeba. It is a trend fintech firms and banks want to buck by introducing innovative digital products.

The latest to join the race is Mama Pays, an app developed by Belcash Technology Solutions Plc, owner of the popular mobile money service, Hellocash. The app was launched after it was integrated with the Bank of Abyssinia's e-commerce gateway. Mama Pays is one of several digital platforms dedicated to remittance and other financial services launched over the past few weeks.

While traditional remittance services such as Western Union take as much as 15pc in transaction fees depending on the transfer mode, some commercial banks have begun offering services for free. Mama Pays allows receivers to request payments from senders, with the option to connect to their bank account, currently limited to the Bank of Abyssinia and Somali Microfinance (SMFI). When a user requests payment, the app automatically generates a link the sender can use to settle the payment through international cards such as Visa and Mastercard. These transactions are subject to a one dollar fee.

Vincent Diop, CEO of Bel Cash, has had his developers working on the app for about eight months. They hope to take the app into the next phase, integrating more commercial banks.

“We're also working on expanding to more payments such as PayPal,” Vincent told Fortune.

The Commercial Bank of Ethiopia (CBE) is gearing up to launch a remittance platform that would cut the transaction costs incurred when using traditional remittance services such as Western Union.

Lion Bank is working to integrate its system with Mama Pays, but the process is not yet completed. The system uses the Bank of Abyssinia e-commerce gateway, launched over a year ago, to authorise credit card or direct payments processing for e-businesses, online retailers, and traditional brick and mortar banking.

The state-owned Commercial Bank of Ethiopia (CBE) hopes to use a gateway to launch a digital remittance platform. Its executives follow the footsteps of Abyssinia, striking a deal with a payment services provider, Flocash. When the application is launched, senders will be allowed to remit, but no service fee is imposed, slashing transfer cost down to zero. The Bank will retain the fees associated with sending money through a global card service, which average 6.5pc globally.

The CBE plans to launch its own gateway, which has been in the works for three years. The Bank had to go through acrimonious public procurement protocols, which contributed to the delay, according to Fikresilassie Zewdu, vice president for branch and digital banking at the CBE.

"Digital journeys are long and painful," said Fikreselassie, referring to the sluggish growth.

Another private bank with an impressive inroad on the fintech front is Dashen Bank. It deployed an e-commerce gateway this year through its Amole Mobile Wallet, partnering with Flutterwave and Thunes.

Flutterwave, a globe remittance facilitator and aggregator, works with more than 100 payment services. Similarly, Thunes also works with hundreds of platforms such as TapTap Send, another app, eyeing the Ethiopian market.

For developing countries such as Ethiopia, remittance from the diaspora far exceeds export revenues. In the past year, remittance inflow was registered at above six billion dollars, a 16pc increase from the previous year. The country’s total export revenues were half this amount. Over the years, the flow of remittance through informal channels has grown tremendously to cover close to 50pc last year, according to the National Bank of Ethiopia (NBE). It was 39pc a decade ago.

Not all banks are taking a slice of the growth in remittance.

According to data from the international business department of Oromia International Bank, the flow of remittances in July and August has shown a 30pc dip compared to the same period of the previous year.

Despite this, service providers seem to be hopeful that the convenience and reliability they offer will lead the informal market to lose ground to digital remittance.

"We believe Ethiopians will see the value of using us as opposed to the informal market," says Mawutor Abraham, growth director for Taptap Send.

However, for the CBE, remittance inflow has been on the rise, according to Fikresillase, although he refrained from citing any figures.

Having launched a crowdfunding platform that raises funds for the Grand Ethiopian Renaissance Dam (GERD), the Bank generated more than 120,000 dollars in about two months.

A similar platform dubbed "It's my Dam", developed by Chapa, a fintech firm, generated more than 200,000 dollars within a few months, collaborating with Zemen Bank.

The country stands to benefit from encouraging remittance rather than focusing on exports, economists believe.

Alemayehu Geda is an economics professor who studied the informal remittance business. He advocates for the establishment of a dual exchange rate regime to incentivise remittance flow through formal exchange markets.

However, the remittance market is driven by demands created through import underwriting and supply credit through export overwriting causes concern among some quarters to embrace this proposition.

As long as the formal market fails to respond to imports and supply foreign currency adequately, the remittance will not see a significant change, according to an executive working in the international banking division at one of the commercial banks.

A country with close to 30 billion dollars in external debt, the economy suffers a balance of payments deficit of an average of five billion dollars. Less than filling this gap, the banks and their fintech allies will find it an uphill task to overcome the competition entrenched in the parallel market.

PUBLISHED ON

Sep 26,2021 [ VOL

22 , NO

1117]

Money Market Watch | Aug 11,2024

Money Market Watch | Mar 07,2026

Commentaries | Apr 26,2019

Fortune News | Jun 15,2019

Commentaries | Aug 14,2021

Viewpoints | Apr 08,2023

Featured | Aug 10,2025

Radar | Mar 14,2020

Commentaries | Jul 13,2020

Featured | Feb 16,2019

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 27 , 2026

The federal legislative house rushed through one of the country's most contentious ho...

When Parliament takes up the appropriation bill, federal legislators will receive a d...

Jun 13 , 2026

The recent policy decision to fully open freight forwarding to foreign capital may be...

Jun 6 , 2026

For a political veteran as controversial as Getachew Reda, last week's national elect...

Loading your updates...

Loading your updates...