Radar | Feb 15,2026

Apr 20 , 2024

By José Antonio Ocamp

Since the onset of the COVID-19 pandemic, the developing world has faced growing public-sector debt vulnerabilities. Interest-rate hikes and limited access to international capital markets have only exacerbated the problem – so much so that even solvent countries are now wrestling with liquidity challenges. The International Monetary Fund (IMF) predicts that, in the coming years, developing countries' debt levels will remain higher than in 2019.

It seems clear that many low- and middle-income countries will continue to experience debt stress, even if they are not at risk of default.

Yet the severity of the crisis is not reflected in the agenda for global cooperation. Last year's G20 Summit in New Delhi, for example, advanced important proposals for development finance but made little progress in addressing the over-indebtedness of low- and middle-income countries. Most crucially, the world still lacks a comprehensive debt-restructuring mechanism to deal with this widespread and recurrent problem.

The oldest existing debt-restructuring mechanism, the Paris Club, covers only sovereign debt owed to its 22 members – mainly OECD countries. Occasionally, multilateral lenders and foreign governments have adopted ad hoc responses to sovereign debt crises. For example, the United States-backed Bradly Plan, implemented after the Latin American crisis of the 1980s, helped reduce some countries' debts and catalysed the development of a sovereign bond market for developing countries. In 1996, the IMF and the World Bank launched the Heavily Indebted Poor Countries Initiative (HIPIC) to provide a much-needed reprieve for low-income countries; this was supplemented in 2005 with the Multilateral Debt Relief Initiative, which cancelled eligible countries' debts to multilateral creditors.

Other reactive measures have aimed to improve the restructuring process.

Following the Mexican crisis of 1994, the OECD's G10 proposed introducing collective action clauses (CACs) in bond contracts, enabling a qualified majority of bondholders to modify the terms and conditions if necessary. In 2013, after the Greek debt crisis, the European Union (EU) mandated the inclusion of aggregation clauses for CACs in its members' bond contracts, facilitating joint renegotiation of several issues. But despite these reforms, creditors can still build blocking majorities, owing partly to the lack of expanded CACs in roughly half of sovereign bonds issued by emerging and developing countries, and partly to the incompatibility between bond agreements and other debt contracts.

The IMF attempted but failed to create an institutional framework for sivering-debt-restructuring in 2001-03. The proposed mechanism would have allowed unsustainable external debts to be restructured through a rapid, orderly, and predictable process while protecting creditors' rights. The overseeing body would have been independent of the IMF's Executive Board and Board of Governors. Ultimately, the US rejected the initiative, as did some developing countries (notably Brazil and Mexico), fearing that the mechanism would restrict their access to capital markets.

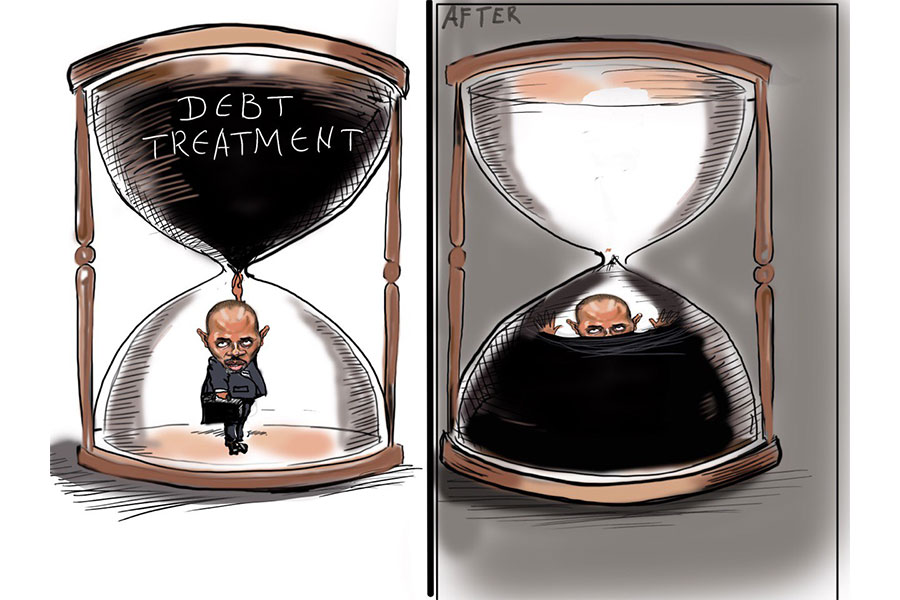

During the pandemic, when public debt levels soared, the G20 and the Paris Club created the Debt Service Suspension Initiative (DSSI) for low-income countries, which stopped debt payments for 48 of 73 eligible countries from May 2020 to December 2021. Then, at the end of 2020, they endorsed the Common Framework for Debt Treatment to coordinate and provide debt relief to DSSI-eligible countries. But, so far, only three countries – Ghana, Zambia and Chad – have reached an agreement under the framework, while only one other – Ethiopia – has applied.

Fears of credit-ratings downgrades have reportedly deterred several other potential beneficiaries from participating.

There is a need for a permanent solution: an institutional mechanism for sovereign debt restructuring, preferably under the aegis of the United Nations. The IMF could also house such a mechanism, but only if the dispute-settlement body remains independent of the Fund's Executive Board and Board of Governors, as proposed in 2003. The renegotiation framework should call for a three-stage process of voluntary renegotiation, mediation, and arbitration, each with a fixed deadline.

However, even if agreed upon, a statutory mechanism would require long and complex negotiations. Thus, an ad hoc instrument is an essential complement. The UN and other entities have proposed a revised Common Framework, which should set a clear and shorter time frame for restructuring, suspend debt payments during negotiations, establish clear procedures and rules, guarantee the participation of private creditors, and expand eligibility to middle-income countries. To ensure post-restructuring stability, any agreement should include revised maturities and interest rates and debt reduction if necessary.

An alternative could be a mechanism supported by the IMF, the World Bank, or regional multilateral development banks (MDBs). In addition to providing the renegotiation framework, the presiding institution could facilitate financing, address the macroeconomic imbalances of the countries involved, and support the restructuring process. If new bonds are issued, they should have a guarantee attached, similar to the Brady bonds.

There is also the question of whether debts owed to MDBs and the IMF should be included in the restructuring processes, as was done for low-income countries in 2005. Given that these institutions are responsible for a significant share of the debt owed by highly indebted low-income countries, especially in Sub-Saharan Africa, it may be necessary to include them. If so, it would be essential to ensure a steady flow of development aid to cover their losses.

The traditional separation between official and private creditors has been complicated by new official lenders, notably China, and the rise of various debt contracts, including guarantees to private investors, separate from bonds. Future "aggregations" must encompass all obligations. Therefore, establishing a global debt registry covering all liabilities with private and official creditors is required to ensure equitable creditor treatment and enhance transparency.

Lastly, to mitigate future debt crises, the World Bank and others have suggested the widespread adoption of state-contingent bonds that adjust returns based on economic conditions or commodity prices. This would alleviate pressure on sovereign balance sheets during downturns. Over-indebted developing countries will never get the relief they need if the international community does not centre the issue on its agenda. Debt restructuring should be a top policy priority at this year's G20 summit in Rio de Janeiro and the Fourth International Conference on Financing for Developing, which will be held in Spain in 2025.

PUBLISHED ON

Apr 20,2024 [ VOL

25 , NO

1251]

Radar | Feb 15,2026

Sunday with Eden | Jul 27,2024

Editorial | Jul 17,2022

Fortune News | Jun 11,2022

Radar | Jan 03,2026

Obituary | Dec 05,2020

Fortune News | Jan 19,2019

Radar | Jun 15,2024

Commentaries | Aug 16,2020

Photo Gallery | 191973 Views | May 06,2019

Photo Gallery | 181726 Views | Apr 26,2019

Photo Gallery | 178450 Views | Oct 06,2021

My Opinion | 143989 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jul 25 , 2026 . By BEZAWIT HULUAGER

Global Bank's Board of Directors have overhauled top management, after suspending sev...

Jul 25 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have overturned the National Lottery Administration...

Jul 25 , 2026 . By NAHOM AYELE

A newly enacted regulation by the Council of Ministers lets eligible producers pledge...

Jul 25 , 2026 . By FITSUM TADESSE

A fuel tanker carrying tens of thousands of litres was confiscated after its driver a...

Loading your updates...

Loading your updates...