Jul 23 , 2022

By Christian Tesfaye

There is a phrase we hear a lot these days: interest rates. It is a key indicator rocking financial markets worldwide and creating economic havoc through a massive capital flight from emerging markets. It is not surprising. Inflation and interest rates are the opposite sides of the same coin. The Phillips Curve tells us that unemployment and inflation are inversely related. When unemployment is too low, inflation edges higher. The balance can be restored by loosening the labour market.

In highly financialised economies, tight labour markets could be loosened by increasing benchmark interest rates. The less cheap money in circulation, the less credit out there in the economy. With less credit, household and private sector spending falls, slowing business activity and reducing employment. It is an ugly process where everybody is left bleeding. But central banks find it a necessary pain to bear for the bigger evil of inflation. This is how most countries operate.

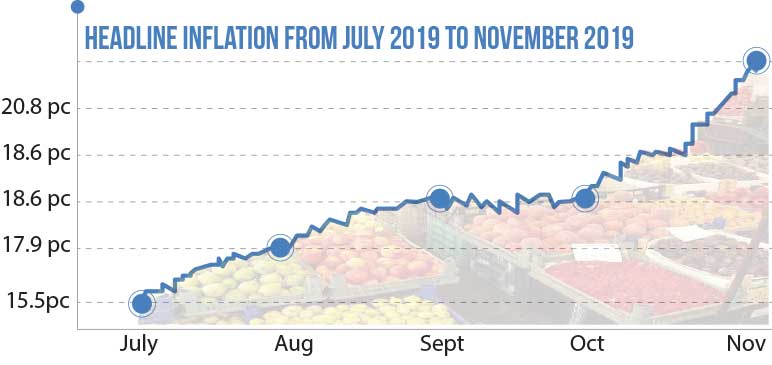

But wait a minute. Ethiopia has been dealing with high inflation for longer than the rest of the world. How come we have not heard talk of interest rates? Why has the key interest rate, savings deposit rate, not been bumped up from its current seven percent?

Inflation hovers in the 30-40pc range. Should savings interest rates not be raised to at least 30pc? It would surely incentivise household saving and discourage spending. Why has the central bank not budged?

Two words: domestic debt. Over the past few years, the federal government has dug deep into a resource that did not use to be as crucial to the budget. Since T-bills have been floated, hundreds of billions of Birr have flown into government coffers to fill budget deficits. This was smart to a point.

For one, double-digit inflation means that a borrower benefits because the real interest rates they pay are negative. The high discount rate makes any amount of Birr now far more valuable than in the future. It is creditors - in this case, banks – that stand to make a loss (do not shed tears for commercial banks; they make the loss back by paying negative interest rates to their depositors).

It is also possible to lean on domestic debt, unlike external financing. Reliance on expansionary fiscal policy by borrowing in the local currency is advocated by proponents of modern monetary theory (MMT). They argue that a government can spend with impunity if it finances deficits with local currency-denominated debt. High debt burden? No problem. Print more money. Sure, the average business or household should worry about its debt, but why should the Ethiopian government, the monopoly issuer of the Birr, be so perturbed?

But what about inflation?

No matter. When it gets out of hand, the government can increase taxes to take money out of the economy. It is a novel way of thinking, and mainstream economists hate it. Nonetheless, it has gained traction in policymaking circles even though no maths back the theory.

Hopefully, this is not something policymakers in Ethiopia use to inform their decisions. Nonetheless, they have allowed domestic borrowing to get out of hand. At this point, the cost of hiking interest rates to fight inflation would hurt a great deal more than it is worth because of domestic debt.

This has to do with expanding treasury bill financing by the government. It is so much that, in the current fiscal year, 278.6 billion Br worth of T-bills will fall due, according to Cepheus Research & Analytics. This is an average of 23 billion Br every month. New borrowing and refinancing are estimated to bump up bond yields by at least two percentage points.

A couple of percentage points rise in saving rates, say to 10pc, will not be catastrophic. But this is unlikely to bring down inflation. With inflationary pressure as sustained and high as that of Ethiopia, and a central bank that has lost credibility, interest rates need to be dialled up all the way to 30pc. Inflation will not know what hit it.

And neither would the federal government. Bond yields will go up and make any more government borrowing to finance deficits impossible. In fact, if it fails to roll over debt - and it will fail at 30pc-plus bond yields - the government will default and take the commercial banks down with it.

More practical solutions are to suspend direct government advances and work to improve rural agricultural productivity. These will have more direct and predictable implications than interest rate hikes.

PUBLISHED ON

Jul 23,2022 [ VOL

23 , NO

1160]

Fortune News | Feb 01,2020

Radar | Feb 12,2022

Radar | Jan 01,2022

Radar | May 16,2020

Radar | May 23,2020

Fortune News | Dec 13,2021

Agenda | Apr 17,2021

Fortune News | Dec 07,2019

Radar | May 09,2020

Commentaries | Dec 09,2023

My Opinion | 131658 Views | Aug 14,2021

My Opinion | 128022 Views | Aug 21,2021

My Opinion | 125985 Views | Sep 10,2021

My Opinion | 123609 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jun 7 , 2025

Few promises shine brighter in Addis Abeba than the pledge of a roof for every family...

Jun 29 , 2025

Addis Abeba's first rains have coincided with a sweeping rise in private school tuition, prompting the city's education...

Jun 29 , 2025 . By BEZAWIT HULUAGER

Central Bank Governor Mamo Mihretu claimed a bold reconfiguration of monetary policy...

Jun 29 , 2025 . By BEZAWIT HULUAGER

The federal government is betting on a sweeping overhaul of the driver licensing regi...

Jun 29 , 2025 . By NAHOM AYELE

Gadaa Bank has listed 1.2 million shares on the Ethiopian Securities Exchange (ESX),...

Loading your updates...

Loading your updates...