Exclusive Interviews | Apr 13,2019

Jul 20 , 2019

By Sophia Bekele

Unless the central bank rectifies the wrongful appropriation of diaspora shares in Ethiopian banks and insurance, it will be a fool’s errand to come and invest their money, writes Sophia Bekele, an international entrepreneur and corporate executive with governance and policy expertise in both public and private sectors.

The National Bank of Ethiopia (NBE) passed a guideline about relinquishing shares in banks owned by foreign nationals of Ethiopian origin in 2016. The majority of the public, particularly the intellectuals and legal experts who understood what happened with the sale of the shares by the central bank and the financial institutions, know that it was a huge mistake.

Various voices have echoed their concerns on the matter. I took all the concerned institutions to court, because I wanted to test if our judicial system works. However, political expediency superseded reason or justice. I argued that the NBE should have differentiated between “investment” versus “inheritance” issues, which was elementary in making its revisionist policy. I also argued the policy violates one of the fundamental principles of law, the non-retroactivity principle. This principle states that the law’s effect does not extend to include past affairs and cannot pass judgment on events that occurred before its implementation. I inherited the shares from my father who passed away before the guideline was passed. Therefore, the guideline should not have applied to me.

The legal analysis of why Ethiopian banks are not duly empowered by the owners, or acquire ownership rights, to be able to grant themselves the right either to sell or appropriate the premium to themselves or to that of the third party has been presented and argued by multiple competent legal experts. A good reference to such legal analysis was written and discussed by the prominent attorney Tameru Wongemagehu who presented his views early on. But he was ignored by the presiding authorities.

Tamiru argued that if the sellers or those who auction the shares are without power or legitimate right to affect the transaction, then the transaction becomes defective to the point of being invalid. He further cited my case as an example in his legal commentary and said, “Sophia took up the gauntlet and headed to the court to vindicate her rights.”

He further challenged the legality of the guidelines stating, “At the time of the auction, an Ethiopian born foreign national remains the owner of the shares unless it is proven that ownership is acquired fraudulently or with criminal intent.”

The parties who were auctioning the shares have no legal standing to sell a property that they did not own. His conclusion was “the path taken by the NBE guideline constitutes an act of sequestration, expropriation or forced purchase.”

He was unequivocal about his conclusion: “NBE’s actions are undeniably illegal.”

Issues such as who owned the shares during the auction, and whether a bank that is neither owner nor agent can sell shares that it does not own, should have been considered. And apparently, the shareholders should have been the beneficiaries of the premiums - that is the gains beyond the par value of the shares upon transfer by auction.

What the central bank and the banks have done is similar to the illegal confiscation of property by the Dergue, which was then against the property right of the law instituted in 1960. Through these improper acts, the central bank of the country has represented the government as a beneficiary of wrongdoing. Therefore, it is a participant in an illegal act.

No evidence has been produced by the NBE of any illegal or criminal act by any diaspora share owners. In fact, there was no damage done. The dividends the diaspora earned could not even be taken out of the country but could only be reinvested. However, financial institutions were forced by the National Bank to identify non-Ethiopian shareholders and to then sell the shares of Ethiopians who have changed their citizenship to another nationality. Shares secured legally by purchases or inheritances by Ethiopian-born individuals who have changed their citizenship is, therefore, deemed a criminal act.

Assuming that foreign nationals of Ethiopian origin are subject to additional restrictions beyond those indicated in the guideline, it may serve as a wake-up call to the financial institutions and to such shareholders to correct and adjust their relationship in accordance with the law, immediately or as soon as practical. The guideline is imprecise on the detail of divesting the shareholders of their ownership right. Nor does it indicate that the bank should redeem or repurchase the shares from the owners. It leaves the ownership right in ‘void’ between the time of surrendering of the certificate by the owners and selling of the shares to the highest bidder. That sounds like an anomaly, because the shareholders are, on the one hand, divested of their ownership right, and on the other, the bank that sells the shares is not the owner of the shares, thereby acting without the will and consent of the owners. We, therefore, face a situation where the bank is selling shares which it neither owns nor is legally empowered as an agent to affect the transaction. What was the motive for the central bank to participate in this illegal collusion with the private banks?

While I could not determine initially why the NBE would issue this new directive to nationalise the investments, I have now come to learn how they justified their actions or reactions. This is obvious for the trained eye after reading the commentary paper submitted to the central bank on behalf of the shareholders of the local financial institutions. That is the pretext of “atmosphere of both fear and suspicion by the new, left-leaning leadership” to initiate and participate in such a sham. Seemingly, the shareholders of the financial institutions were highly concerned and threatened by a large amount of shareholding and investment from the diaspora. As a result, they had pressured their own leadership to aggressively lobby the NBE and presented a prescriptive paper that recommended the distinct strategies on the sale of the diaspora shares and various policy options. I have come to learn the NBE blindly and unequivocally adopted these recommendations.

In fact, I may argue further that even the structures of the new proposed investment directive depend heavily on these recommendations, evidencing the collaboration.

While I can simply assert that the NBE was manipulated by the private sector financial institutions, the profit motives for both the central bank and the financial institutions leaves me to conclude that one cannot be a victim of the other. The amount of money collected by the treasury from its actions is merely a low figure of 20 million to 25 million dollars. But the private financial institutions have benefited from the proceeds of the sale during the 30-day period they themselves prescribed as an option, which the NBE accepted. The buyers of the shares from the Ethiopian diaspora were the shareholders of the banks and insurance institutions themselves. This can be verified easily through a legal discovery process.

As a result, a huge injustice was done to the trusting Ethiopian diaspora. Our trust is now broken by our financial institutions. The gatekeeper, the NBE, has also been the poacher. It is now rewriting another directive or proclamation to sway the diaspora into bringing yet more investment money. This has obviously already been met with huge suspicion. The diaspora has no protection with the demonstrated musical chair policy of the NBE, where there is potentially a clear danger of it writing yet another proclamation to nationalise our new investment. What the NBE already did is an act of extortion and betrayal, it should be corrected to build trust with the Ethiopian diaspora.

The way forward to rectify the situation is for NBE at first instance to correct the wrongful act it did in order for the Ethiopian diaspora to feel whole, build trust and contribute to the future investment in Ethiopia.

Allow the executive organ of the country to be involved in the decision-making process when it issues important directives such as selling property illegally and or making key directives, such as the one they are doing now to liberalise the space. We should not suffer from our loss. The organs that have caused the damage must be responsible to make us whole, by reinstating our original share ownership, or if that seems unattainable, new shares must be issued at equivalent value to us with all the premiums covered by the tortfeasor.

The monies and profits confiscated from the sale of the diaspora shares should be returned in full. All unsold shares in the banks and insurance companies should remain at par value at the respective institutions. Directives should be made by the central bank communicating to all private banks and insurance firms that participated in the sale of diaspora shares. If the NBE fails to rectify its previous position with the above measures, I strongly caution that we do not come running to Ethiopia to invest. We will be running a fool’s errand.

PUBLISHED ON

Jul 20,2019 [ VOL

20 , NO

1003]

Exclusive Interviews | Apr 13,2019

Commentaries | Feb 13,2021

Radar | Feb 25,2023

Commentaries | Nov 09,2019

Radar | Mar 20,2021

Commentaries | Oct 05,2019

Radar | Nov 14,2020

Fortune News | Nov 09,2019

Radar | Oct 26,2025

Commentaries | Jun 29,2019

Photo Gallery | 186107 Views | May 06,2019

Photo Gallery | 176136 Views | Apr 26,2019

Photo Gallery | 171818 Views | Oct 06,2021

My Opinion | 139556 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

May 9 , 2026

The Ethiopian state appears to have discovered a fiscal instrument that is politicall...

May 2 , 2026

By the time Ethiopia's National Dialogue Commission (ENDC) reached the end of its fir...

Apr 25 , 2026

In a political community, official speeches show what governments want their citizens...

For much of the past three decades, Ethiopia occupied a familiar place in the Western...

May 9 , 2026 . By NAHOM AYELE

Finance Minister Ahmed Shide entered the last quarter of the fiscal year with a budge...

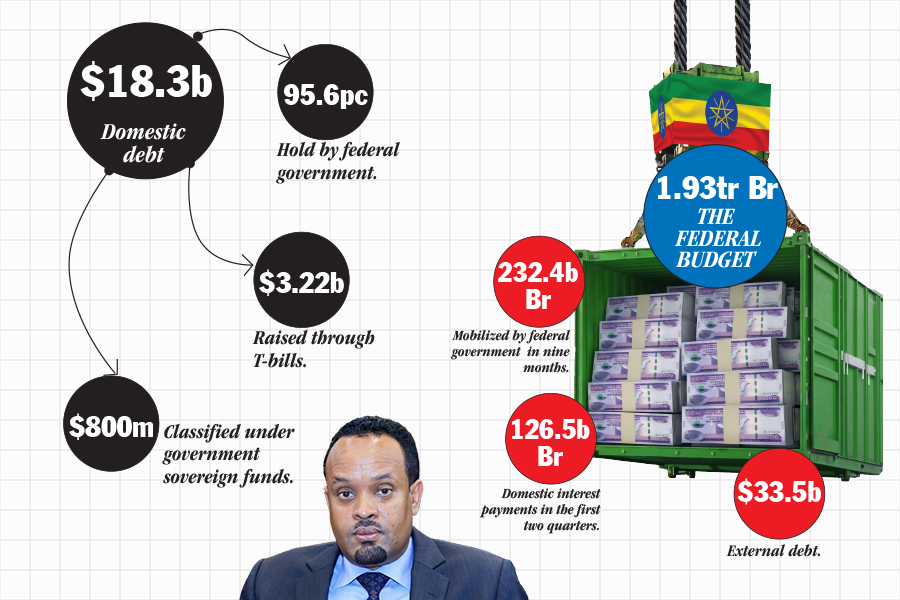

May 9 , 2026 . By NAHOM AYELE

At the Federal High Court's Lideta Division, on Dejazmach Bekele Weya Street, one of...

May 13 , 2026

Mayor Adanech Abiebie's cabinet has approved an additional 9.9 billion Br budget, a m...

May 9 , 2026 . By BEZAWIT HULUAGER

The fight over Cosmo Trading Plc has outgrown the courtroom where it began. What star...

Loading your updates...

Loading your updates...