Jun 24 , 2023

By Tsedeke Y. Woldu

In 1997, a startling episode of financial legerdemain occurred in Ethiopia: the government wiped from the ledger a commercial debt used to acquire Ethiopian Airlines equipment, draining the country's foreign exchange (forex) reserve by a fifth. The International Monetary Fund (IMF), oblivious to Ethiopia’s precarious reserve position, sanctioned a substantial loan for a proposed structural adjustment programme.

The later revelation of Ethiopia’s dwindled reserves sparked outrage among the IMF's leadership.

Such historical episodes, while revealing fascinating crossroads in economic policy, continue to resonate today. A fresh call for financial market liberalisation has arrived, accompanied by the familiar issues of opaque commercial borrowings, forex reserve depletion, exchange rate reunification, and national conflicts. Any serious dialogue on financial liberalisation is welcome for the private sector, as businesses suffer from chronic forex shortages.

Forex discussions are usually about shortages induced by dismal exports and low remittance, with the conversation often veering towards the dependency on international commodity prices and proposing remedies like fiscal consolidation, monetary contraction, and structural trade adjustments.

The notion of exchange rate stability as a governmental or market competence is rarely addressed, let alone the complexity of maintaining a large gap between nominal and real exchange rates, or the concept of exchange market pressure (EMP) — the normalised percentage sum of reserve depletion and domestic currency depreciation.

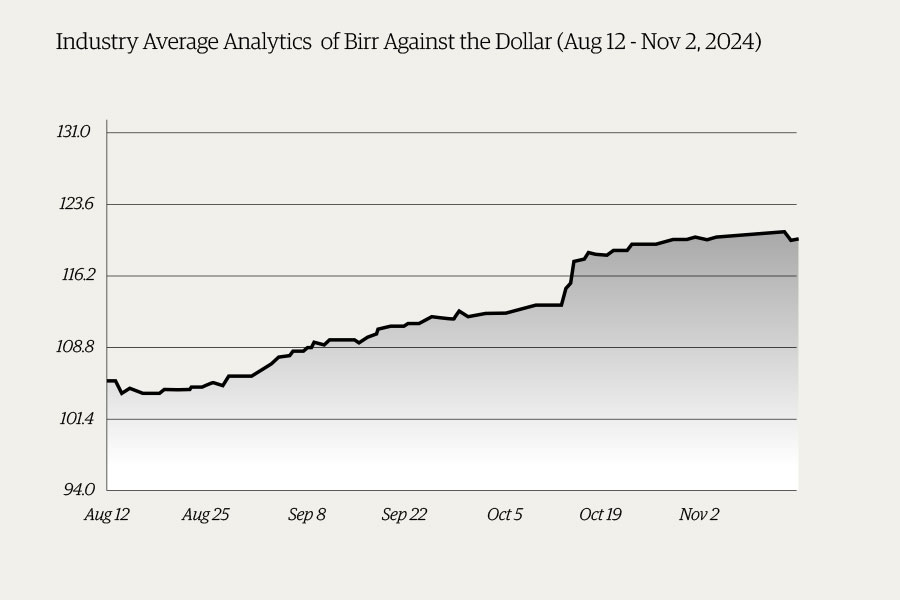

Today’s financial ecosystem appears fixated on the might of the US Dollar, even over gold, hinting that a reliable and convertible currency is akin to possessing an epic gold mine. This might suggest that Ethiopia could consider bolstering the Birr to become a reliable and convertible currency.

Despite consistent bourgeois criticism of the US political economy, its financial sector continues to allure global capital, and its industry entices world-class labour. This is possibly attributable to the country’s low level of political and financial repression.

The World Bank’s paper, "Exiting Financial Repression - The Case of Ethiopia" by Jean-Pierre Chauffour and Muluneh Ayalew Gobezie, explores the least disruptive paths for lifting financial repression in Ethiopia, emphasising monetary and financial liberalisation. It defines repression as the government’s capture of financial resources at below-market prices for discretionary allocation.

They proffer cautious advice on abolishing financial repression, insisting on continued capital account and exchange control until fiscal balance, effective monetary instruments, and adequate forex reserve are achieved alongside moderate inflation. However, the current EMP on the Birr has significantly worsened since the paper’s release.

EMP was also a focal point of the IMF’s recent publication, "Managing Exchange Rate Pressures in Sub-Saharan Africa—Adapting to New Realities, April 2023". The report suggested mitigating the adverse impact and containing exchange rate pressures via tighter monetary policy, fiscal consolidation, and strengthening the social safety net.

Although such advice is academically sound, it often overlooks the harsh realities faced by policymakers who must bear financial and political risks alone. Policymakers themselves are often trapped in myths: they assume a pseudo-control on forex, exaggerate the blessings of devaluation, downplay the role of “management” in a managed float, and persist in the belief that domestic currency will perpetually depreciate until exports outpace imports.

The fear that a free float will drain reserves, unmoor inflation, and result in financial collapse also paralyses decision-making. These myths need to be challenged.

The reality is that no central bank can control another’s currency. The coercive confiscation of earnings in its realm is not control — it is expropriation. Devaluation provides only temporary relief, with the benefits quickly vanishing in the face of ensuing inflationary pressure. The belief that the Birr will continue to depreciate indefinitely contradicts certain factors; the relative abundance of domestic currency and the flow of goods, services and capital occurs in cycles, requiring a dynamic ebb and flow of currency.

The fear that a free float will result in a reserve depletion and rampant inflation is indeed concerning. Yet, this rests on assumptions that domestic reserves will be unlimited and that central bank intervention will be absent—both far from reality.

A commercial bank’s reserves drying up whenever the National Bank of Ethiopia (NBE) or Commercial Bank of Ethiopia (CBE) infuses some dollars into the forex market highlights the impracticality of such a catastrophic depletion of foreign assets from a free float. It is absurd to imagine the government remaining idle during a reserve run.

Although intervention will be necessary to avert financial collapse, it should not replicate old methods of expropriation. A more astute financial approach is possible.

For instance, instead of expropriating remittance earnings and forcing the surrender of forex earnings, a proactive market intervention could be employed to prevent a sharp depreciation or appreciation. The central bank could provide a generous supply of forex to the market from its reserve and absorb excess Birr to maintain exchange rate stability.

A cautious liberalisation of the forex market, with the government acting as a stabilising force, might prove a sensible approach.

Yet, the journey towards a financially liberalised Ethiopia confronts an uncomfortable reality. As Ethiopia navigates its journey towards a free market economy, it must wrestle with an unusual state of affairs in which the "managed float" or "crawling peg" asserted by the National Bank of Ethiopia (NBE) has become, in effect, a synonym for forex rationing. Here, the belief in an everlasting depreciation of the Birr finds itself at odds with a reality shaped by an abundance of domestic currency and cycles of goods, services, and capital flows. Addressing these obstacles requires dislodging deeply-rooted misconceptions.

Interestingly, the government and market competence dichotomy in exchange rate stability needs revisiting. While the government has a role in maintaining stability, particularly in times of shock or crisis, market forces should primarily determine the rate. An adequately managed float implies the central bank’s intervention to avoid excessive volatility while generally allowing the exchange rate to be set by the market.

Ultimately, the discourse on Ethiopia’s financial liberalisation and forex reform should move beyond rigid positions and outdated myths.

This transition is necessary for technical expertise, political bravery, adept strategic communication, and a nuanced understanding of the interplay between global and local forces. It requires a pledge towards a future in which Ethiopia’s financial system is resilient, and inclusive, and serves the country’s broader developmental aspirations.

PUBLISHED ON

Jun 24,2023 [ VOL

24 , NO

1208]

Featured | Sep 10,2021

Featured | May 25,2019

My Opinion | Sep 10,2022

News Analysis | Dec 08,2024

Agenda | Mar 02,2024

Fortune News | Nov 03,2024

Editorial | Jun 15,2024

Money Market Watch | Nov 16,2024

Radar | Oct 08,2022

Fortune News | Nov 04,2023

My Opinion | 131451 Views | Aug 14,2021

My Opinion | 127803 Views | Aug 21,2021

My Opinion | 125783 Views | Sep 10,2021

My Opinion | 123419 Views | Aug 07,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jun 7 , 2025

Few promises shine brighter in Addis Abeba than the pledge of a roof for every family...

Jun 29 , 2025

Addis Abeba's first rains have coincided with a sweeping rise in private school tuition, prompting the city's education...

Jun 29 , 2025 . By BEZAWIT HULUAGER

Central Bank Governor Mamo Mihretu claimed a bold reconfiguration of monetary policy...

Jun 29 , 2025 . By BEZAWIT HULUAGER

The federal government is betting on a sweeping overhaul of the driver licensing regi...

Jun 29 , 2025 . By NAHOM AYELE

Gadaa Bank has listed 1.2 million shares on the Ethiopian Securities Exchange (ESX),...

Loading your updates...

Loading your updates...