Radar | Jul 21,2024

Building on its success over the past four years, Tsehay Insurance registered another growth in profitability. Yet its earnings per share (EPS) showed a notable decline last fiscal year.

Despite the 12pc increase in profit after tax of 32.8 million Br, its EPS declined to 34 Br from 37 Br, due to a rise in claims paid and paid-up capital.

In the reported period the company increased its paid-up capital by 26.9pc to 110.8 million Br. It also spent 165.7 million Br in claims and other technical provisions, a 13pc growth.

The increase in claims paid in terms of the frequency of motor accidents coupled with the level of severity of the damage that raised the price of spare parts pushed the claims higher, according to Kassa Lisanework, CEO of Tsehay, which was established seven years ago and currently has 216 employees and 160 shareholders.

However, Abdulmenan Mohammed, a financial analyst based in London, United Kingdom, applauds the management of the company for achieving solide performance, saying that the claim growth is reasonable and the management should carefully watch claim growth despite the reasonable rise.

Mandefro Erkou, the chairperson of the board of directors of Tsehay, remarked that the positive performance was achieved despite a formidable challenge in the last fiscal year mainly related to the political unrest.

Tsehay Insurance Financial Performance In The Year 2018/19.

"It distressed the performance of the insurance industry as a whole," he told shareholders in the annual report of the company.

A modest increase in premiums, a surge in commission earned, reduction in premium ceded and increase in dividend income helped the company to increase its net profit.

Underwriting surplus increases by 35pc reached 34.6 million Br, while the gross written premium grew by five percent to 300 million Br. Out of this, Tsehay was able to retain over 245 million Br, helping the company to increase the retention rate by three percentage points to 82pc.

Tsehay earned 9.7 million Br in commission, a nine percent increase against the 12pc rise in paid commissions to agents that reached 23.3 million Br.

The higher rate of growth in commissions compared to the growth in written premiums must be a result of tough competition in the insurance industry, the expert remarked.

Interest and dividend income showed a percentage point and 44pc surge to 22.5 million Br and 6.8 million Br, respectively. The company invested in shares at United, Abyssinia and Berhan banks, and Ethio-Reinsurance, among others.

The insurer's expenses on staff and general administration rose by 33pc to 28.3 million Br, while direct expenses accounted for a 37pc increase to 27.3 million Br.

The rise in expenses is considerable, according to the expert suggesting that management set up cost control mechanisms to keep expenses at bay.

However, Kassa, the CEO, does not have much concern about the increase in expenses, stressing that it is well below the 35pc threshold set by the National Bank of Ethiopia, which was still described as good.

In the reported period, the company made a salary raise to retain staff and opened three new branches, pushing the total number of branches to 23. Kassa also attributed the rental price hike as one of the causes for swelling expenses.

The massive expansion of the company’s balance sheet showed a 20.6pc increase in its total assets, which reached 599.4 million Br.

The investment in shares, government securities and time deposits accounted for close to 44pc of its total assets, a reduction from 48.3pc in the previous fiscal year.

The expert noted that the reduction must have been a result of the huge money held with reinsurers as receivables, as well as the increase in cash and bank balances. The company has 153.7 million Br of receivables from reinsurers.

“Tsehay needs to collect this money and invest it in income-generating activities,” Abdulmenan suggested.

The increased level of liquidity of Tsehay was reflected in its cash and bank balances that shot up by 106.7pc to reach over 70 million Br. The ratio of cash and bank balances to total assets also went up to 11.7pc from just 6.8pc in the preceding year.

“The increase in the liquidity level must have contributed to the reduction in the ratio of invested funds to total assets,” the expert observed.

Its capital and non-distributable reserves accounted for 22.8pc of the total assets, indicating the sound capital base of the insurance company, according to the expert.

PUBLISHED ON

Jan 18,2020 [ VOL

20 , NO

1029]

Radar | Jul 21,2024

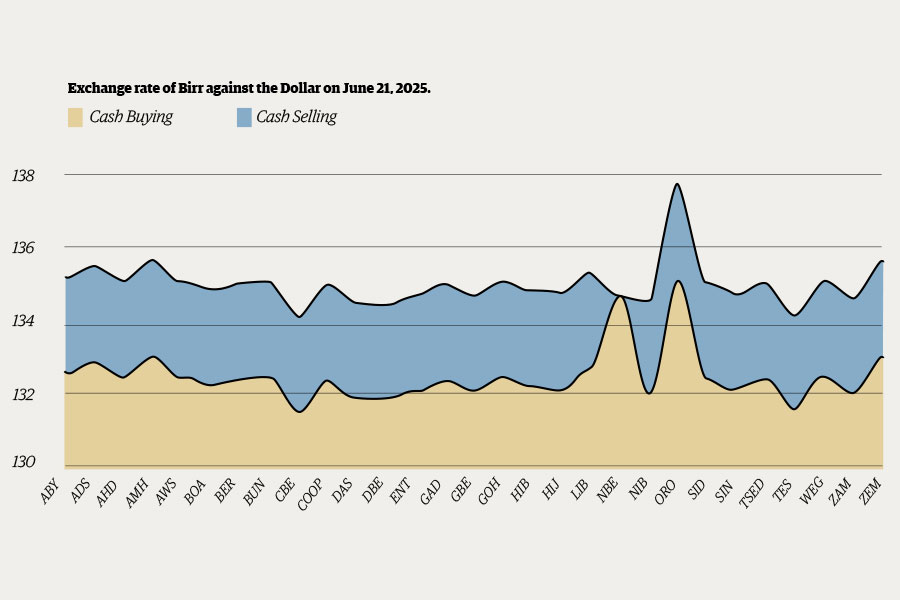

Money Market Watch | Jun 21,2025

News Analysis | Dec 09,2023

Fortune News | Mar 02,2019

Fortune News | Mar 18,2023

Fortune News | May 29,2021

Sunday with Eden | May 20,2023

Commentaries | Aug 25,2024

Covid-19 | Jul 06,2021

Fortune News | Oct 26,2019

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jun 27 , 2026

The federal legislative house rushed through one of the country's most contentious ho...

When Parliament takes up the appropriation bill, federal legislators will receive a d...

Loading your updates...

Loading your updates...