Editorial | May 27,2023

Aug 7 , 2021

By HAWI DADHI

Promoters of two interest-free banks under formation, Ramis and Zad, have agreed to a merger deal, under pressure to meet central bank requirements, persons close to the matter disclosed to Fortune.

It is a move signalling that promoters of financial institutions rushing to join the banking industry have to raise half a billion Birr in capital before the deadline in mid-September this year. Others are pleading with regulators at the central bank for an extension.

Ramis, which began selling shares in September 2019, has raised more than 400 million Br in paid-up capital, while Zad has managed to raise somewhere around 80 million Br. If the merger goes through, the interest-free bank will be the third to join the industry after ZamZam and Hijra banks, which entered the financial sector earlier this year with a paid-up capital of 870 million Br and 700 million Br, respectively.

A recent directive approved by the National Bank of Ethiopia (NBE) requires commercial banks in operation to raise paid-up capital in five years to five billion Birr. New entrants were given the option to get incorporated with 500 million Br capital and increase tenfold in sevenyears. Several initiatives currently offering shares to the public have thus far failed to attain their goals due to political instability, lack of interest from prospective shareholders, and insufficient time to complete paperwork.

Promoters of another new entrant, Akufada Bank, one among over two dozen banks currently selling shares to the public, are downbeat about meeting the requirement before the deadline, having raised just 25pc of the required amount. The current state of affairs with instability in the country and the economic slowdown are not helping, says Robel Nigusse, project manager of Akufada.

The group is considering the option of a merger and has held a few discussions with prospective partners, disclosed Robel. The promoters might attempt to raise five billion Birr in seven years, the other option laid out in the directive, instead of dissolving.

It is not the only group on the lookout for prospective partners in the merger bid. Ge'ez Bank, mobilising 300 million Br from 5,000 shareholders since last year, is devising new sales strategies, according to Layne Kinfe, marketing manager. Ge'ez hopes to meet the threshold set by the central bank upon deadline but remains open to merge with others. The group has been approached for a merger, an offer promoters are considering, according to Layne.

"We won't achieve much on our own," said Layne.

Promoters of Jano and Kush banks remain hopeful they will conclude selling shares soon. Jano hopes to close initial public offerings this week, having raised the required capital while the latter is still mobilising equity from the public.

Promoters of Ge'ez and Jano, along with six others, filed a petition before the Governor of the central bank two weeks ago, pleading that the six-month period provided in the directive is not sufficient to complete selling shares, hold shareholders assemblies and file the necessary paperwork before the public notary office. The promoters of these groups hope to be granted an extension of six months up to a year.

According to Abdulmenan Mohammed, a finance expert known for keeping a close watch on the banking industry for the last two decades, pleading for an extension is a reasonable demand.

"It's not easy to raise such an amount of money in a short period of time," he said.

Among the petitioners, Afro Bank has raised a little over a quarter of a billion Birr. Kassahun Ayalew, one of the promoters of the Bank, says one-third of the six month period is spent on completing paperwork. He believes the COVID-19 outbreak, the national elections, and recurrent conflicts have made it difficult for people to invest in new initiatives.

He disclosed that the group is considering a potential merger while awaiting a response from officials at the central bank.

"We've received a request," he told Fortune.

Pushing banks to consolidate in the market is one of the justifications put forth by the central bank for the requirements to increase capital 10-fold, though industry insiders see it as a move aimed at limiting the number of banks in business. Having less than 20 banks operating in a country with as large a population and economy as Ethiopia is simply insufficient, Abdulmenan says. Less than 7,500 bank branches are serving a population of over 100 million.

"Compared to other Sub-Saharan countries, the number of banks in Ethiopia is small," he said.

Abdulmenan does caution the dominance of state-owned banks, which constitute 60pc of the assets in the industry. This is much higher than in neighbouring Kenya, where state banks have less than a five percent share.

"What makes the formation of a larger number of banks in Ethiopia worrying is that they scramble for a market share which is just a third of the industry size," says Abdulmenan.

Kassahun begs to differ. The market share of the state-owned Commercial Bank of Ethiopia (CBE) is slowly eroding, mainly due to the growth of private banks. In his opinion, the banks aspiring to join the industry, especially those that will provide specialised services, will contribute to loosening the CBE's grip.

Its unlikely new banks able to raise five billion Birr in capital will emerge soon; the industry will remain out of reach to newcomers for years to come, Abdulmenan projects.

PUBLISHED ON

Aug 07,2021 [ VOL

22 , NO

1110]

Editorial | May 27,2023

Radar | Apr 15,2023

Radar | Oct 17,2020

Radar | Dec 24,2022

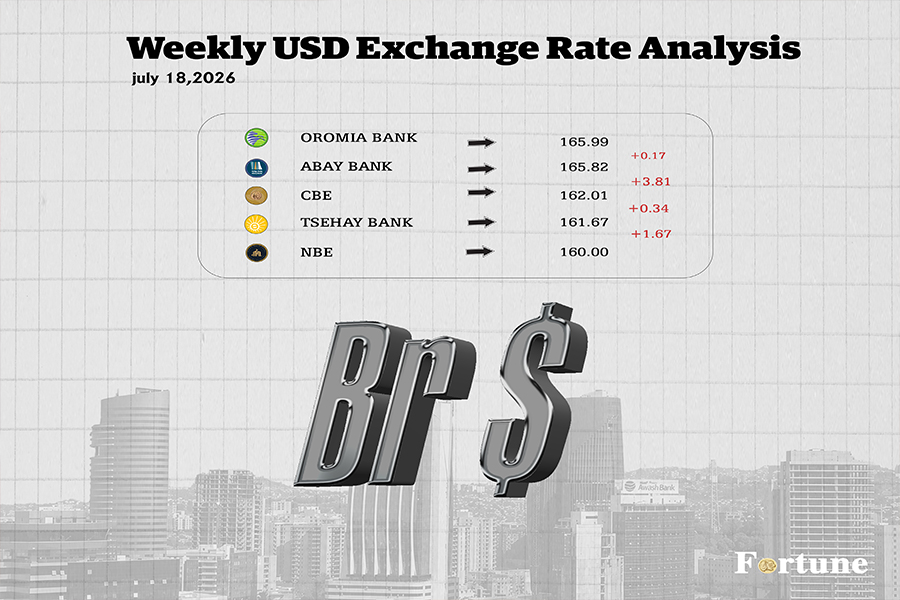

Money Market Watch | Jul 19,2026

Covid-19 | Jun 12,2021

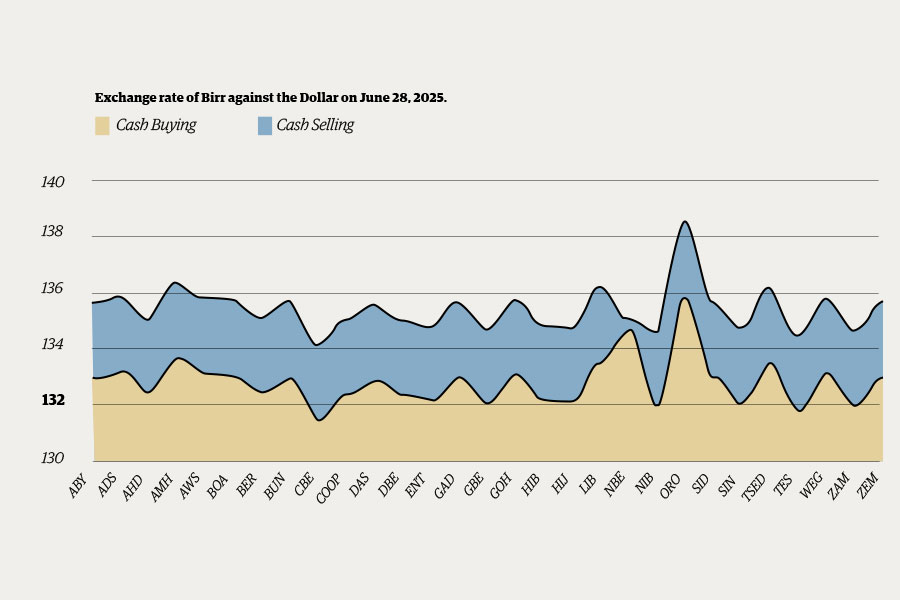

Money Market Watch | Jun 29,2025

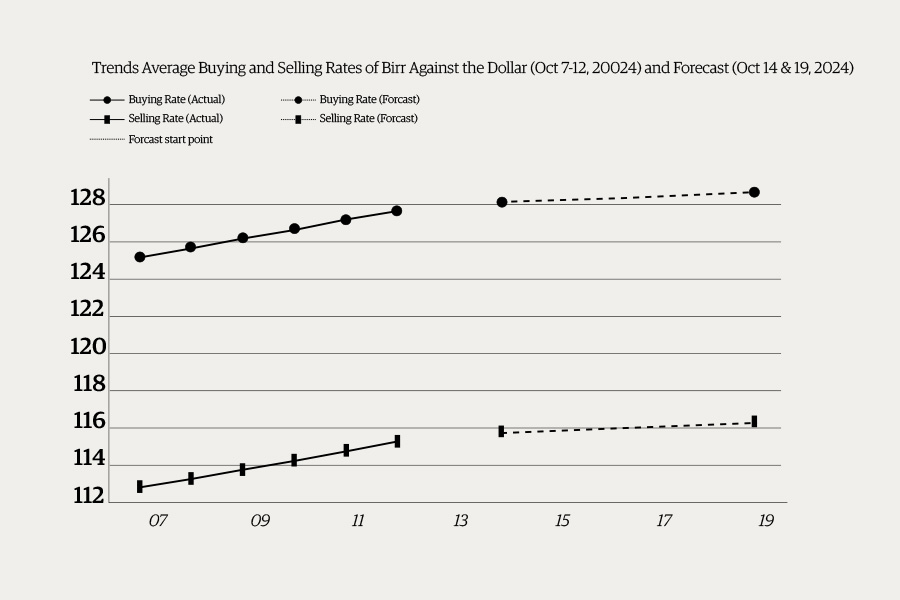

Money Market Watch | Oct 13,2024

News Analysis | Mar 23,2024

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jun 27 , 2026

The federal legislative house rushed through one of the country's most contentious ho...

Loading your updates...

Loading your updates...