Fortune News | May 15,2024

Oct 26 , 2024

By Bogolo Kenewendo , Patrick Njoroge

A large-scale debt relief plan is necessary to relieve the crushing debt burden and enable investment in climate-resilient infrastructure. This plan should involve bilateral creditors and MDBs taking a 'haircut' to restore fiscal stability, incentives and penalties to ensure creditors' participation in debt restructuring, and support for non-distressed countries to reduce capital costs, write Bogolo Kenewendo and Patrick Njoroge, co-chairs of the Debt Relief for a Green & Inclusive Recovery Project. This commentary is provided by Project Syndicate (PS).

Many countries have experienced extreme weather in one form or another this year. The summer, marked by intense wildfires, was the hottest on record, while the return of El Nino has led to catastrophic flooding and other disasters. Such shocks demonstrate the urgent need for multilateral efforts to address climate change and achieve sustainable development.

In the last few months of this year, world leaders will gather for a series of summits – including the International Monetary Fund (IMF)-World Bank Group annual meetings in Washington, DC [ongoing], the G20 summit in Rio de Janeiro, and the United Nations Climate Change Conference (COP29) in Baku – where they could make progress on these fronts. These meetings are particularly important for African countries, which remain vulnerable to the effects of global warming amid a deepening sovereign debt crisis.

Of the 20 countries most vulnerable to climate change, 17 are in Africa. In addition to adverse weather and rising temperatures, African economies have suffered a series of external shocks in recent years, including inflation spikes, interest-rate hikes in advanced economies, rising geopolitical tensions, and violent conflicts. Partly due to these shocks, the continent’s public debt levels increased by a whopping 240pc between 2008 and 2022.

The consequences are dire. Over half of African countries now spend more on interest payments than on healthcare and lack the fiscal space to invest in sustainable development. This cycle of debt and development distress makes these countries even more vulnerable to the effects of global warming, trapping them in a loop of economic instability and environmental degradation.

While increased liquidity may offer temporary relief to African economies by easing short-term fiscal pressures, it fails to address the deeper debt problem impeding green growth. To mobilise the financing needed for climate action and to achieve the UN Sustainable Development Goals (SDGs) by 2030, we estimate that at least 34 African countries will require significant debt relief. Unfortunately, the G20’s Common Framework for Debt Treatments, designed to provide relief to countries in debt distress, has proven woefully inadequate.

Its case-by-case approach is slow and insufficient, leaving many countries in a perpetual state of fiscal instability. Private creditors’ reluctance to participate in debt restructuring, coupled with the exclusion of multilateral development banks (MDBs), has resulted in uneven and often inadequate responses.

To embark on the path of sustainable development, African countries need large-scale debt relief. This would provide governments with the fiscal space to invest in resilient infrastructure, renewable energy, and other climate-related projects. Without such measures, Africa’s green-growth aspirations will be unfulfilled, and the continent will continue to suffer from unsustainable debt dynamics that escalate climate damage and worsen social outcomes.

Large-scale debt relief should rest on three pillars.

Bilateral creditors and MDBs should take a haircut to restore fiscal stability in debtor countries. Incentives and penalties are also required to ensure private and commercial creditors’ full participation in debt restructuring. Finally, credit enhancements and support for non-distressed countries should be provided to reduce capital costs and maintain liquidity. This holistic approach would enable African countries to scale up and sustain investment in climate resilience and sustainable development.

An essential part of these reforms is the inclusion of climate considerations in the IMF’s debt sustainability analyses (DSA). Currently, DSAs focus on a country’s ability to service its debt, while failing to consider its need to invest in the energy transition and the industries of the future. By incorporating climate risks and opportunities into DSAs, the international community can ensure that debt relief is aligned with broader sustainability goals.

It is also critical for all creditor classes, including private bondholders and MDBs, to participate in debt restructuring. Using fair comparable-treatment rules to determine losses would ensure equitable burden-sharing.

Such a coordinated and comprehensive approach to debt relief would unlock Africa’s potential for green growth, an essential part of any long-term solution to the climate crisis. The continent has vast solar, wind, and hydro resources and the world’s youngest and fastest-growing workforce. With the right investments, Africa could become a hub for renewable energy and clean industries, thereby advancing the continent’s development goals and the global fight against climate change.

Looking ahead to 2025, African leaders will have a unique opportunity to drive the reforms needed to address the debt-climate nexus. With South Africa presiding over the G20 (which now counts the African Union as a permanent member), and Uganda leading the G77, the continent’s governments will be in a position to push for significant debt relief and critical reforms to the global financial architecture.

The climate and debt crises in Africa are inextricably linked, and addressing one but not the other is a recipe for failure. The international community should act now to support Africa in building a sustainable, green future for all.

PUBLISHED ON

Oct 26,2024 [ VOL

25 , NO

1278]

Fortune News | May 15,2024

Exclusive Interviews | Jan 04,2026

Fortune News | Oct 15,2022

Radar | Jul 13,2025

Radar | Aug 24,2019

Fortune News | Apr 28,2024

Fortune News | Mar 30,2024

Radar | Jan 24,2026

Fortune News | Dec 20,2025

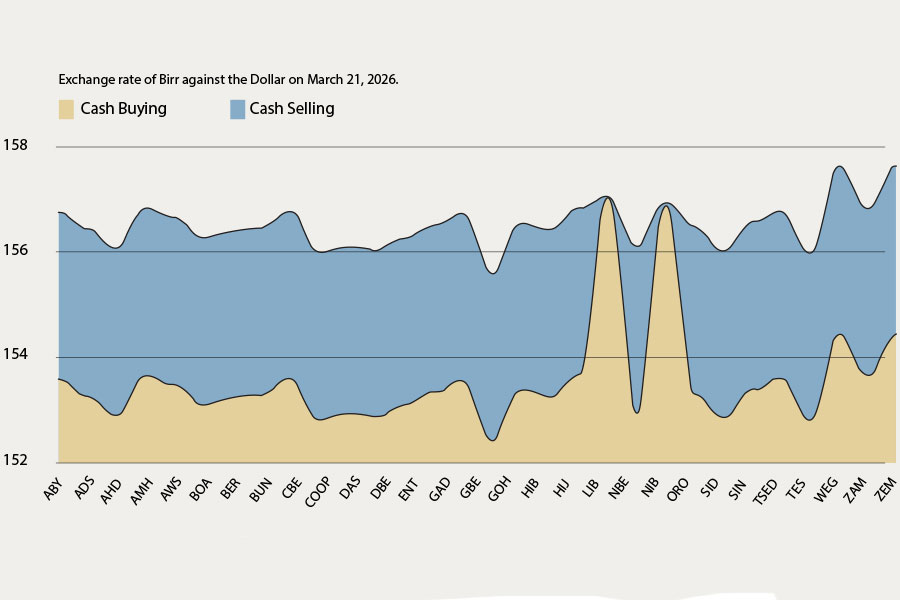

Money Market Watch | Mar 21,2026

Photo Gallery | 190987 Views | May 06,2019

Photo Gallery | 180770 Views | Apr 26,2019

Photo Gallery | 177439 Views | Oct 06,2021

My Opinion | 143083 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jun 27 , 2026

The federal legislative house rushed through one of the country's most contentious ho...

When Parliament takes up the appropriation bill, federal legislators will receive a d...

Jun 13 , 2026

The recent policy decision to fully open freight forwarding to foreign capital may be...

Jul 7 , 2026

The health sector remains underprovided despite rising public spending, Prime Ministe...

Jul 7 , 2026

Prime Minister Abiy Ahmed (PhD) delivered one of his bluntest rebukes yet to the coun...

Jul 7 , 2026

Prime Minister Abiy answered his critics with a mix of gratitude and edge, thanking l...

Jul 7 , 2026

A ruling-party lawmaker, Mohammed Ahmed, called the Chamber to its feet for Prime Min...

Loading your updates...

Loading your updates...