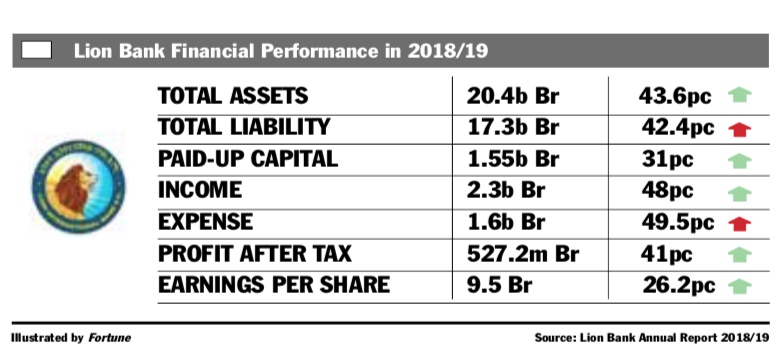

Radar | Dec 02,2023

Enat Bank, one of the youngest banks in the industry, saw shareholders' return on investment dip for the second year in a row, despite an improved performance last year.

But shareholders should have a bigger worry than a declined return from a net profit of almost 230 million Br from its operation in 2020/21. The figure is 10pc higher than what the Bank recorded the previous year. Shareholders' equity may have increased by 11pc to two billion Birr, in tandem with the Bank’s paid-up capital that reached 1.5 billion Br. Enat Bank, however, needs to raise 600 million Br annually in equity to meet the central bank's five billion Birr threshold capital.

Abdulmenan Mohammed, a financial statement analyst based in London, foresees difficulties for Enat directors and executives in raising the remaining 3.5 billion Br considering the economic slowdown and its lukewarm performances over the past couple of years.

"If we go by its track record, such a growth rate will be impossible to achieve," said Abdulmenan. "This may compel Enat to merge with other small banks."

Since its incorporation eight years ago with a paid-up capital of 75 million Br, Enat Bank raised equity by a yearly average of 142.5 million. Enat's directors and executives are aware of the trials that lie ahead.

Frehiwot Worku, Enat's board chairperson, urged shareholders to settle commitments and buy more shares to shore up its capital base. The air of desperation was evident during a shareholders' meeting held last month at the Inter Luxury Hotel. It is a time of economic woes due to global pandemics, wars, and growing competition within the industry for equity. For a third-generation bank like Enat, the headwind comes from almost all the private banks - large and small - running against time to meet the capital threshold set by the central bank for June 2026.

The appeal for the share-buying public comes from banks' track record in their performance, value to shareholders, and asset quality.

Close to 61pc of Enat Bank's assets, 14.6 billion, come from loans and advances. Although it is much lower than the industrial average of 74.4pc, it is a portfolio that has seen an impressive expansion of 30pc last year. For Ermias Andarge, president of the Bank, better results could have been achieved had it not been for the instability in the country's north, which forced the Bank to halt operations at eight of its 88 branches across the country.

The banking industry underwent a considerable expansion in branch networks over the past year. The 18 commercial banks opened 844 new branches, bringing the total to 7,262. The state-owned Commercial Bank of Ethiopia (CBE) leads the pack, opening 95 new branches to push its network to 1,920.

Although Enat opened 31 branches last year alone, it is one of the banks with the lowest network in the industry.

“The strategy is to position our branches in a few places and support them with electronic banking,” said Ermias.

Enat's branch expansion drive played a role in boosting deposits mobilised by 32pc to 11.2 billion Br. However, its loan-to-deposit ratio increased over three percentage points to 79.4pc; however, it is way below the industry average of 85pc, indicating the Bank has more cash in its vaults than it is lending.

Enat Bank’s liquidity level increased in value but not in relative terms, however. Cash and bank balance reached nearly three billion Birr, growing by 26pc, while its ratio of liquid assets-to-total assets fell slightly to 19.8pc from 20.5pc. Spendings on rent and branch openings put pressure on the Bank to improve its liquidity, Ermias concedes.

Salaries and benefits paid by Enat Bank to 800 employees, 147 of whom were hired during the reporting period, soared to 267.5 million Br. Interest expense, which accounts for almost half of total expenditures, ballooned by nearly a third to reach 652 million Br.

Increased lending activities helped the Bank grow its total income to 1.7 billion Br last year, up from 1.3 billion Br. Interest income, which accounts for 76pc of the total, climbed 30pc to 1.3 billion Br.

Enat's income from non-financial intermediation was mixed.

Revenues from fees and commissions stagnated at 222.7 million Br while other income shot up by a staggering 155pc to 148.2 million Br.

The Bank also managed the highest gains from foreign exchange dealings in its history. They nearly tripled to 124 million Br from the figure recorded in 2019/20.

Ermias contends the gains are partly due to the effects of the COVID-19 pandemic, which brought with it increased export revenues. Goods shipped from Ethiopia brought in 3.6 billion dollars last year, a 20pc jump.

"The Bank gained a thicker slice of the foreign currency earned by the country,” said Ermias.

Nonetheless, Enat Bank struggles to maintain the performance that saw profits jump by 40pc to 159 million Br two years ago. Shareholders seem buoyant about their prospects.

Azalech Zegaye owns 100,000 Br worth of shares at Enat Bank. She is not alarmed by the 1.8pc decline in earnings per share (EPS) to 158 Br.

"The returns fell by a small margin, which is expected under the current circumstances,” said Azalech.

Close to two-thirds of Enat's 18,000 shareholders are women.

PUBLISHED ON

Jan 22,2022 [ VOL

22 , NO

1134]

Radar | Dec 02,2023

Fortune News | Feb 29,2020

Radar | Jun 15,2025

Radar | Dec 16,2023

Editorial | May 28,2022

Radar | May 20,2023

View From Arada | Sep 10,2022

Radar | Dec 10,2022

Fortune News | Sep 04,2021

Fortune News | Mar 12,2022

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jun 7 , 2025

Few promises shine brighter in Addis Abeba than the pledge of a roof for every family...

Loading your updates...

Loading your updates...