Radar | Sep 10,2021

For domestic businesses with a robust presence in the global market, the inability to accept small online payments from international customers remains beyond incomprehensible. It is a frustrating ordeal.

Adam Overton, manager of Gesha Village, a high-end coffee exporter with a farm in the West Omo Zone, is among those who lived this episode of despair. Overseeing a farm located 479Km south of Addis Abeba, his company sends off coffee samples regularly, between 250g to two kilograms, but bears the cost amounting to 400,000 Br a year.

Ever since its establishment a decade ago, transactions were traditional. Samples are sent out, orders follow, shipments are made, and transfers through the banks are undertaken.

This has changed lately after Adam stumbled upon international payment gateway services offered by the Bank of Abyssinia. Orders for shipping samples are placed on the company`s website for prices ranging from 16 to 99 dollars and Adam and his team were keen to test the platform the bank offers. Initially, they may have been nervous that the platform could not provide policies for refunds, as standard e-commerce trading platforms do.

The challenges, Adam recalled, were not as worrisome as he had feared.

"Within a week, with no advertisement, we've managed to receive up to 10 orders," said the General Manager. "I was happy not to have to say no to people."

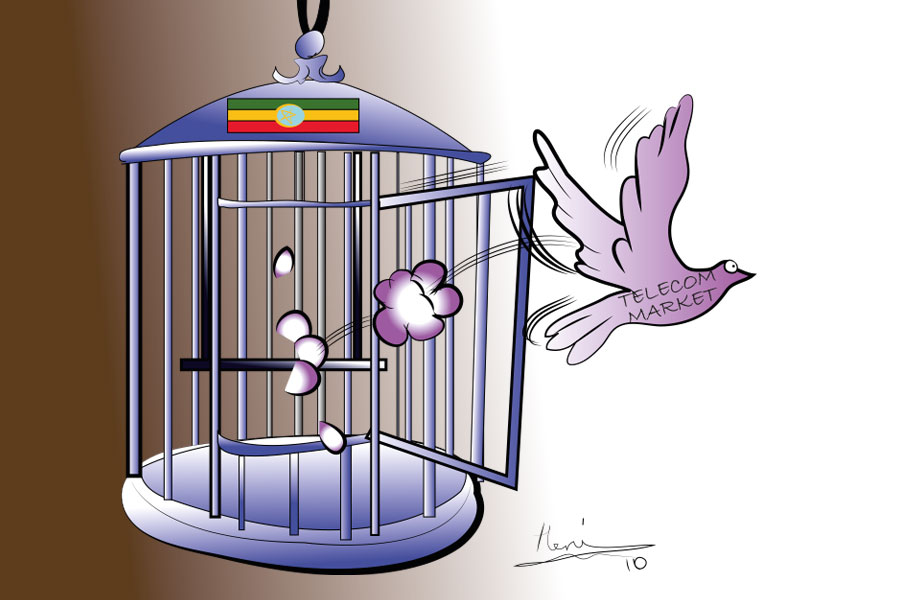

The icing on the cake is the reduced shipping rates DHL charges for transactions on e-commerce. Now that the payment side has been figured out, Gesha hopes to export larger quantities of coffee in addition to the samples if the legal framework changes to permit it to do so. The first international gateway platform for the country, unveiled by the Bank of Abyssinia last year, allows domestic companies to sell products in international markets.

Designed to read card information from the payer's side and process a payment to collectors, in this case, e-commerce sellers, international payment gateway services can be instituted in two ways. While the first is to partner with an already established gateway provider, the other option is to adjust an already existing switch that can process international transactions. The Bank of Abyssinia opted for the first, partnering with CyberSource, a digital company that works with Visa and Mastercard. These are companies holding 90pc of the market share for card services across the globe.

Hotels, retailers, and tour and travel agencies are the main customers, providing services to the buyer subject to transaction fees imposed by the card issuer. The Bank of Abyssinia also pays a small cut, less than a dollar, for every transaction. Having a stringent monitoring mechanism known as decision manager, which deploys fraud detection protocols using 68 billion previous transactions to identify potential fraudulent activities and is enhanced by machine learning, the system has integrated hundreds of merchants that want to sell their products internationally.

A partnership agreement was signed between the Bank of Abyssinia and CashGo, a crowdfunding and remittance application, on March 5, 2021.

About 43pc of consumer purchases worldwide, excluding China, were made through a digital form of payment last year. However, e-commerce trading is nascent in Ethiopia; onboarding merchants has been a challenge for the Bank. Gesha Village is one of the exceptions in that its website has an API that can integrate with the Bank`s portal.

Not many are clients with digital platforms with the standards needed for integration; some do not accept payments; and some are not able to integrate APIs, according to Sosena Mengesha, chief digital banking officer at the Bank of Abyssinia.

For a country with a low number of internet users, 23 million, that the e-commerce industry is inching may not be a surprise. But the absence of a regulatory framework that directly addresses e-commerce was not encouraging many to migrate to the digital space. Last year, the electronic transaction proclamation was issued, a result of a new digital policy and a national payment gateway directive by the National Bank of Ethiopia (NBE). More encouraging to the financial sector is the emphasis given by the administration of Prime Minister Abiy Ahmed (PhD) to develop a digital economy.

Dashen Bank is yet another financial firm that has jumped on the gateway bandwagon, developing a platform in six months. In April last year, the 25-year old Bank launched its services in partnership with Moneta Technologies, best known for its Amole app, while Visa availed its CyberSource software. Dashen has registered about 20 merchants while several more applications are on hold, according to Kassaye Eshetu, digital banking officer at Dashen, whose gateway accepts Visa, Mastercard and American Express, the latter of which is exclusive to its services.

Dashen and Abyssinia depend on CyberSource to access a payment gateway solution. However, experts see the emergence of a local service provider of the same solution as a matter of time. One of them is Nurhassen Mudesir, a fintech expert, who foresees that a local service provider could surface as an alternative to partnering with international remittance technology providers, allowing for easier system integration and lower service fees.

With the advent of emerging technologies, it is becoming easier for local companies to circumvent and directly connect the newly developed payment networks, according to Nurhassen. "However, exploiting the options currently available shouldn't be forsaken before making sure the alternative implementation can be realised."

It appears that the bankers well understand his advice.

Dashen hopes to see its system help reduce costs incurred by e-commerce traders and individuals who receive money from overseas using the formal channel.

Remittances in the first nine months of the fiscal year registered 3.78 billion dollars, a 14pc increase from the past year, but 6.7pc lower than the highest recorded, 4.06 billion dollars, over the same period in 2018/19. Traditional remittance services may cost as high as 15pc depending on the provider, the transfer method, and where clients collect the cash. Direct bank transfer could cost as high as 25pc depending on the volume of the transfer. However, transfers on digital platforms on average cost 2.5pc to 3.9pc, except for PayPal, which stands at five percent. If digital transactions are expanded in e-commerce, embracing more companies such as Gesha Village, it signals that the country could potentially benefit from higher forex earnings and reserves that covered just 2.4 months of imports by the end of last year.

Exports brought in 2.1 billion dollars over the nine months of the year, a 16pc increase from last year.

For a country with remittance inflow double the amount of export earnings and equivalent to four percent of its GDP, banks seem to understand accelerating the use of digital services is a step forward by any standards.

Awash International Bank has been a pioneer of digital remittance through its digital services dubbed Asgori, a money transfer option through PayPal. Globally, PayPal has over 390 million users, availing transfers in 200 countries with 25 currencies. The service provider charges five dollars for every transaction made, which makes up the transfer fee and currency conversion fee.

Asgori PayPal, launched three years ago, allows account holders to transfer money directly to the accounts of Awash customers, while beneficiaries who have no saving account with Awash can collect the money from one of the Bank's branches. Recognising the potential, others are lining up to join the digital remittance arena as well.

The most recent market entrant is a service from Dashen Bank that allows users to send money from their card providers and most digital money services like Google and Apple Pay. In partnership with Flutterwave, a global payment service provider with more than 10 methods such as mobile wallet, digital money, card, and bank transfers, recipients can get their money directly from the Amole mobile wallet or pick up cash from the Bank's branches.

In partnership with the Bank of Abyssinia, the CashGo application came to the scene with remittance and crowdfunding as its core services earlier this year. In the past, charitable institutions in Ethiopia used GoFundMe to collect donations from overseas. However, GoFundMe takes as much as three percent of donations collected, compared to the CashGo platform offers free of service charge, which has registered 16 non-profit organisations seeking donations.

This increases the foreign currency amount generated and donations delivered to these organisations, Besufekad Getachew, co-founder of CashGo, believes. Remittance transfers cost below the global average, whereby the platform charges one percent for amounts above 100 dollars and one dollar for amounts below 100 dollars. To keep a watch on fraudulent activities, up to 5,000 dollars can be sent at once, and a person can send a total of 15,000 dollars a day.

Since the official launch of CashGo two months ago, the activities on the app have been somewhat modest, garnering more than 1,000 downloads on the Google Play Store so far. On average, one transfer amounts to 350 dollars, according to Besufekad, who is working to integrate the platforms with six other banks, including the Commercial Bank of Ethiopia (CBE)

The state-owned CBE is by far the largest bank handling foreign transfers, with a forex inflow of 1.7 billion dollars in remittances over the first half of this year.

But CashGo is going to face its fair share of hurdles posed by informal foreign exchange inflow as well as the low adaptability of technology-based services. "People think of traditional service providers when they think of remittance," Besufekad said.

Moreover, it will have to win the customer over from traditional remittance companies instead of facing the uphill battle of informal remittance, a methodology that Dashen Bank is also sticking to.

"When the remittance is received directly into bank accounts, it fosters saving tendencies," said Kassaye.

Nonetheless, there are structural problems beyond the remittance business. The parallel market offers an average of 10 Br against the dollar compared to the official transfers, discouraging senders and receivers from going to the banks whether through the traditional channel or the digital platforms. Last year, nearly half of the country's remittance inflow came from informal channels, which grew significantly year after year.

This can be addressed through the banks or the regulator using digital remittance services. Although drastically lowering the cost of transactions in time and processing costs, these services can only lower the cost down to a certain point, necessitating policy change and market intervention, according to experts.

Regulators have to investigate how to incentivise innovative digital remittance service providers, especially those with innovative products and services, according to Nurhassen.

"Banks and the blossoming fintech companies should effectively market their value-added services to the Ethiopian diaspora through innovative products such as remit-to-pay that complement and encourage remittance," he said.

But there is little that can be as effective as bridging the gap between the official rate and the parallel market, an option policymakers at the macroeconomic team are tinkering with lately, according to officials familiar with the policy orientation.

Time will tell if this will be a policy path the administration of Prime Minister Abiy wants to take. However, it will mean a hopeful future for those in the ecosystem as more and more traders like Gesha join the digital market.

PUBLISHED ON

Jun 05,2021 [ VOL

22 , NO

1101]

Fortune News | Mar 09,2024

Radar | May 23,2020

Radar | Apr 17,2021

Radar | Jan 15,2022

Fortune News | Dec 19,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jun 27 , 2026

The federal legislative house rushed through one of the country's most contentious ho...

Loading your updates...

Loading your updates...