Life Matters | Jan 10,2026

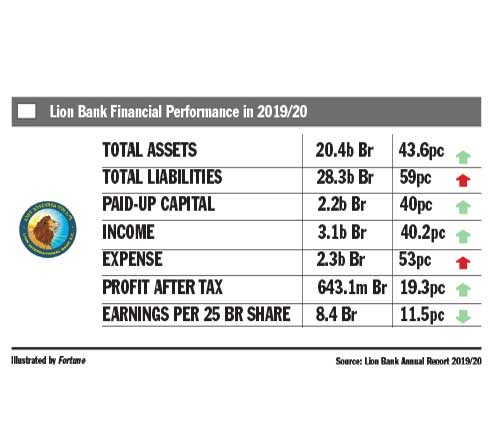

Oromia Coop Bank (Oromia Coop) has enjoyed significant growth in key financial metrics during 2021/22. However, despite a lower total asset turnover, the Bank's higher profit margin and reliance on debt financing contribute to its higher return on equity (ROE) than the average for the top eight private banks.

Shareholders gathered at the Aba Geda Hall in Adama (Nazareth) in December to receive the news that the Bank had registered impressive profit growth, despite declining earnings per share to 34 Br from 40 Br. Fikru Deksisa (PhD), board chairman, attributed the decline in earnings per share to an injection of a significant amount of fresh capital.

Shareholders voted a few years ago to raise the Bank's capital to 13.5 billion Br, boosting its capital adequacy ratio (CAR) by 0.6 percentage points to 13.2pc, far higher than the regulatory authorities' minimum requirement of eight percent. Oromia Coop has increased its paid-up capital by 66.2pc to 7.73 billion Br, becoming one of the four private banks that have passed the central bank's minimum threshold set for 2026.

Financial expert Abdulmenan Mohammed applauded that the Bank follow a capitalization policy that optimizes shareholder returns.

Oromia Coop registered a net profit of 2.05 billion Br, a 54.1pc growth compared to the previous fiscal year, driven mainly by financial and non-financial intermediation revenues. Its profit after tax grew by 34.0pc YoY, indicating a healthy operational performance and an enhanced ability to generate profits for shareholders. The Bank's profit margin of 21.86pc exceeds the industry average of 20.6pc, demonstrating its efficiency in converting revenue into net income.

Derbie Asfaw, the Bank's President, said his management was focused on increasing capital while keeping shareholders' returns satisfactory.

"Capital is essential to compete in the financial market," Derbie said.

A fourth Chief Executive Officer of Oromia Coop since its incorporation in 2005, he was appointed president in 2016. He replaced Wondmagegn Negera, who now serves as the CEO of the Ethiopian Commodity Exchange (ECX). Derbie began his career in the banking industry at the Commercial Bank of Ethiopia (CBE) as a clerk, gradually reaching the deputy presidency position before moving to run Oromia Coop.

The Bank's financial strength and stability have improved since, with its total capital experiencing a 59.4pc YoY increase.

Its income from Murahaba, an interest-free saving scheme, more than doubled to 955.13 million Br, while gains on foreign exchange increased by 43.8pc to 1.32 billion Br. Fees and commissions surged by 37.6pc to 1.61 billion Br. Interest income soared by 49.4pc to 8.08 billion Br, a figure lower than some of the largest private banks such as Awash (14.1 billion Br) and Bank of Abyssinia (14.3 billion Br).

The significant growth of revenues considerably impacted profit growth; however, the expansion was accompanied by increased expenses.

Interest expenses rose by 33pc to 2.7 billion Br, salaries and benefits increased by 43.2pc to 2.32 billion Br, while other operating expenses surged by 44.7pc to 3.56 billion Br. The total operating expenses of Oromia Coop, at 5.8 billion Br, is a billion Birr higher than the average of its peers such as Awash, Abyssinia, and Dashen.

Notes Abdulmenan: "Although the growth of revenues is commendable, the jump in expenses needs attention."

The Bank achieved a higher Return on Equity (RoE) compared to the average of the top Ethiopian private banks, demonstrating its ability to generate better returns for its shareholders, with an ROE of 22pc compared to the industry average of 21pc. Oromia Coop's ROE was six and two percentage points higher than Hibret and Oromia banks and six and seven percentage points lower than Abyssinia and Awash banks, respectively.

The Bank ranks third in Return on Assets (ROA), indicating its relative efficiency in generating profits from its assets and providing returns to shareholders. Oromia Coop's total assets increased by 40.9pc to 114.6 billion Br, growing by 40.9pc YoY, showcasing the Bank's expansion in size and resources compared to the previous year.

Loans, advances, and interest-free financing also increased by 54.3pc to 82.7 billion Br. They have grown by 54.3pc YoY, highlighting Oromia Coop's focus on providing credit to its customers.

The Bank's non-performing loans (NPL) ratio stood at two percent, lower by two percentage points than the average for the top industry performers. Provision for impairment of loans and other assets soared by 177pc to 631.63 million Br, revealing that substantial loans and advances increased. Abdulmenan cautioned the management to keep an eye on doubtful loans and advances, as it is concerning. The average provision for the top eight performer private banks was 446 million Br, while Awash Bank's was more than double the amount.

Derbie agreed that the provision of Oromia Coop rises as the loss and substantial loans increase.

"It'll probably increase," he said.

Total deposit reached 96.77 billion Br, showing an increase of 36.1pc. The figure exceeds the average of the top eight banks with 84.1 billion Br but is 68.8pc of the total deposit mobilized by Awash and almost 78pc of Bank of Abyssinia.

Furumsa Dubale, an auditor at the 22-Mazoria branch for five years, is proud that his branch achieved 80 customer base targets during the financial year while performing well on mobilizing deposits. He expects the Bank to focus on expanding its digital system.

"Banks are moving towards digital technology," Furumsa told Fortune.

Deposits at Oromia Coop rose by 36.1pc YoY, reflecting an increase in customer trust and an expansion of its customer base. The loan-to-deposit ratio increased to 85.5pc from 75.4pc, lower than Abyssinia,Dashen and Awash banks but higher than the remaining top private banks.

While commending the growth, the expert cautions Oromia Coop for increasing the loan-to-deposit ratio to this level as it may affect its liquidity.

Liquidating its investment in five-year central bank bills, Oromia Coop invested 7.75 billion Br in treasury bills, accounting for 6.5pc of the Bank's total assets. The liquidity level of the Bank increased in absolute and relative terms.

Haile Gebre Lube, former head of the Oromia Regional State Cooperative Agency, initiated the idea of forming a bank by the cooperatives. Oromia Coop registered 112 million Br paid-up capital, where 700 cooperatives still hold most shares.

Bogale Abera is one of the 15,000 shareholders who bought 50,000 Br shares last year. He is happy with the returns, collecting 14,000 Br as dividends. Bogale wants the Bank to expand its branches in recognized crop harvesting areas in the Oromia Regional State, widening the customer base.

The Bank opened 124 branches in the reported year, bringing the total number to 593.

"It's because we were focused on expansion," Derbie told Fortune.

This growth earned Oromia Coop the fourth rank among private banks in most critical financial metrics and ratios, following the Awash Bank, which consistently ranked at the top, showcasing its dominant position in the market. Abyssinia and Dashen follow.

While Oromia Coop showed solid performance in the financial year 2021-22, there is still room for growth and improvement. Its total asset turnover of 8.16pc falls slightly below the industry average of 8.9pc; the Bank could further improve its performance by utilizing assets more effectively to generate revenue.

The equity multiplier, which highlights banks' reliance on debt financing to acquire assets, stands at 10.13 for Oromia Coop Bank, higher than the industry average of 9.8. The Bank is more reliant on debt financing than its peers.

PUBLISHED ON

Apr 03,2023 [ VOL

24 , NO

1196]

Life Matters | Jan 10,2026

Editorial | Aug 14,2022

In-Picture | Jul 28,2024

Fortune News | Mar 13,2021

Viewpoints | May 16,2026

Viewpoints | Apr 22,2023

Agenda | Jul 07,2024

Fortune News | Jul 13,2025

Fortune News | May 16,2020

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 31 , 2026

Weldu Yiheysh has not read the Pacific temperature charts. He does not need to. In Shibta District of Enderta Wereda, in...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Loading your updates...

Loading your updates...