Fortune News | Jan 15,2022

Mar 2 , 2019

By FASIKA TADESSE ( FORTUNE STAFF WRITER )

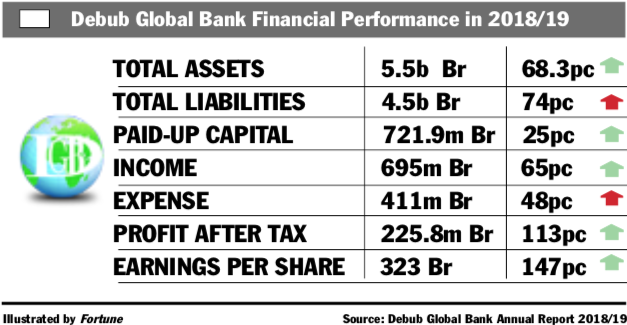

Aided by the massive growth in all income activities, Debub Global Bank reported a substantial profit in the last fiscal year.

The second youngest bank increased its after tax profit by 153pc, reaching 106.6 million Br. Its earnings per share (EPS) also rose to 131 Br from 103 Br.

That is a piece of delightful news for shareholders, according to Abdulmenan Mohammed, a financial statement analyst with a decade and a half of experience.

“Yet the earnings per share of the Bank is still the lowest in the industry,” commented Abdulmenan. “There is a long way to get to the industry average.”

The private industry's average earnings per share stands at about 30pc, as a percentage of share par value, while Debub Global's was 13.1pc.

Enat Bank, Debub’s peer and nearest competitor, netted 158.8 million Br in profit last year and paid 184 Br in earnings per share to its shareholders.

In the reporting period, Debub Global faced various challenges including political and economic problems, according to Nuredin Awol, board chairperson of the Bank. Public unrest and the chronic foreign currency shortage were among them, according to him.

"For us, the challenges unleashed our commitment to prevail over the circumstance and deliver a delightful experience for our customers," said Nuredin in the annual report of the Bank.

Debub, one of the late entrants into the banking industry as the 15th private bank, has bagged the remarkable profit driven by huge increases in all income items.

Interest on loans, advances and National Bank of Ethiopia bills increased by 99pc to 213.5 million Br, net gains on foreign exchange dealings soared by 134pc to 50.8 million Br.

“Achieving such increase is very amazing while this line of income dropped across many banks,” said Abdulmenan.

The bank has exerted enormous effort to realise this, according to Addisu Habba, president of Debub Global, which was established in August 2012 with 266.9 million Br subscribed and 138.9 million Br in paid-up capital.

“There were exporter shareholders of the Bank who were working with other banks,” Addisu told Fortune. “Last year, we made them work with us.”

Debub’s income from fees and commission also increased by 64pc and reached 136.6 million Br.

Expense accounts of the Bank have also shown a significant increase.

Expenses of interest; salaries and benefits; and general and administrative soared by 99pc, 30pc and 56pc, respectively, reaching 80.3 million Br, 84.5 million Br and 103.3 million Br.

The growth of general and administration expenses needs attention, according to Abdulmenan.

“To retain our exporter clients, we provide them with massive loans and advances from the deposits we mobilised with an expensive interest rate,” said Addisu.

The Bank disbursed loans and advances of 1.5 billion Br, an increase of 102pc and mobilised deposits of 2.2 billion Br, leading the loan-to-deposit ratio of the bank to grow by 72pc from 54pc.

“The loan-to-deposit ratio of Debub is very impressive,” said Abdulmenan, “so the management of the Bank must be appreciated.”

The private banking industry has disbursed a total of 60.6 billion Br in loans and advances during the reporting period.

The total assets held by Debub grew by 58pc and reached 3.3 billion Br.

Provision for loans and other asset impairment increased by 27pc to 10.4 million Br.

Even though the increase in provision for doubtful loans and advances is high, it is still reasonable, according to Abdulmenan.

The investments in NBE five-year bonds increased by 61pc to 686.3 million Br, representing 21pc and 32pc of total assets and total deposits of the bank, respectively.

Liquidity analysis shows that the liquidity level of Debub increased in value terms but dropped in relative terms.

Its cash and bank balances increased by 21pc to 824.9 million Br.

Debub’s liquid assets to total assets declined to 25.3pc from 33pc, and liquid assets to total liabilities also decreased to 31.4pc from 40.5pc.

"Despite the reduction in liquidity ratios, the liquidity level of Debub was reasonable," said the expert.

The paid-up capital of Debub increased by 65pc to 580 million Br. Its capital adequacy ratio, the ratio of a bank's capital to its risk, also stood at 41pc.

“The ratio is much higher than required, and it needs to focus on using this capital efficiently," recommended Abdulmenan.

Addissu accepts Abdulmenan’s recommendation.

The Bank was attempting to utilise the capital by investing in procurement or the building of its headquarters, but this could not be realised, according to Addissu.

“We are planning to realise it this financial year,” Addissu told Fortune.

PUBLISHED ON

Mar 02,2019 [ VOL

19 , NO

983]

Fortune News | Jan 15,2022

Radar | Oct 20,2024

Fortune News | Aug 16,2020

Radar | Dec 04,2022

Radar | Dec 25,2021

Radar | Jul 28,2024

Fortune News | Jan 25,2020

Radar | Nov 28,2020

Agenda | Nov 16,2019

Fortune News | Feb 22,2020

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jun 28 , 2025

Meseret Damtie, the assertive auditor general, has never been shy about naming names...

Jun 21 , 2025

A well-worn adage says, “Budget is not destiny, but it is direction.” Examining t...

Jun 14 , 2025

Yet again, the Horn of Africa is bracing for trouble. A region already frayed by wars...

Jun 7 , 2025

Few promises shine brighter in Addis Abeba than the pledge of a roof for every family...

Loading your updates...

Loading your updates...