Radar | Jul 06,2025

Dec 19 , 2020

By FASIKA TADESSE ( FORTUNE STAFF WRITER )

The National Bank of Ethiopia (NBE) has required all the commercial banks to submit a quarterly report that shows the amount of loans and advances they approved and disbursed against movable property. Approved almost a year ago, the law requires banks to dedicate five percent of their total loan portfolio toward the agricultural sector.

Signed by Solomon Desta, a vice governor at the central bank in charge of financial institutions supervision, the letter was dispatched at the end of last month. The Movable Collateral Registry became operational as of last February, activating a scheme allowing banks to approve loans by taking movable assets as collateral.

The regulatory bank also requires the banks to file the annual disbursement budget and actual loan disbursements against movable properties in a format that is provided to them beforehand. The reports have to be filed at the central bank in soft copy via email or as a hard copy to the Ethiopia Movable Collateral Registry Office that was established under the NBE. Headed by a director, the Office has an Electronic Collateral Registry System and is in charge of approving and providing user accounts for creditors to access the collateral.

Banks should allocate at least five percent of their credit disbursement of the year to entities in the agricultural sector including individuals, cooperatives, unions, enterprises and others using movable property as collateral. Banks that fail to comply with this rule will have to allocate 10pc of their loans to agriculture in the following year.

Taking movable property as collateral for loans and advances is part of the administration's effort to ensure access to finance as well as to raise the loans directed to the agricultural sector. Over the past five years, less than 10pc of loans were directed to agriculture, which is significantly lower than the 30pc to 40pc targeted by the Ministry of Agriculture. The scheme was introduced as part of the Homegrown Economic Reform Agenda that was kicked off by the government two years ago.

The legislation of the law is a landmark initiative since it will encourage the majority of the population who are living in rural parts of the country, according to Yinager Dessie (PhD), governor of the central bank, who spoke at the CEO Forum that was organised last week by Precise Consult.

"If we create access to finance to the farmers and pastoralists," he said, "It'll create a positive impact on the life and livelihood of many."

Yinager also said that the central bank is working closely with the Ministry of Agriculture, Ethiopian Intellectual Property Office, banks and insurance companies to realise the plan.

In mid-September, the NBE issued a directive with a mechanism allowing banks to take farm products, livestock, financial instruments, intellectual property, and forest and landholding certificates as collateral to approve loans. When approving loans, the financial institutions are required to register a tax identification number, national identification cards or passports from the borrowers. The Ministry of Agriculture will provide plastic ear tags to identify the livestock.

The ear tag, which has a 10-digit unique national identification code that is printed in black on a yellow plate, includes details about the species of the livestock, the logo of the Ministry, and the regional code number.

Financial instruments, including bonds, shares, vouchers and warehouse receipts, will also be used as a guarantee after getting registered under the movable collateral registry with their unique serial number. Borrowers using financial instruments are required to provide a TIN, and creditors can consider the market value to determine the par value of the financial instruments.

Intellectual property (IP) should also get a unique serial number issued by the Intellectual Property Office. The valuation of the IP is proposed to be followed by the analysis of the proposal that is submitted by the owner of the IP together with a feasibility study for the loan.

The land use right certificate that is registered under the movable collateral registry with the type of crop pledged, the expected maximum output, and the maximum production can be taken as a guarantee for a loan. Relevant authorities can issue identification of the land use, while development agents handle the valuation of the expected production output of the land. These can be cross-checked with researchers at the Ministry of Agriculture.

Melaku Kebede, CEO of Hibret Bank, says that his institution has been working on these even before the directive was issued, albeit only to a small extent.

"It's an alternative for the banks," he said. "It's a good mechanism to keep customers building a relationship."

Melaku, who believes that the scheme is doable depending on the risk appetite of the banks, argues that the demand for these services is high and it will decrease the risk-taking preference of banks.

"Banks will pick businesses with low risk and high-value collateral," he said. "It'll be more practised where there is a lower demand for the service."

PUBLISHED ON

Dec 19,2020 [ VOL

21 , NO

1077]

Radar | Jul 06,2025

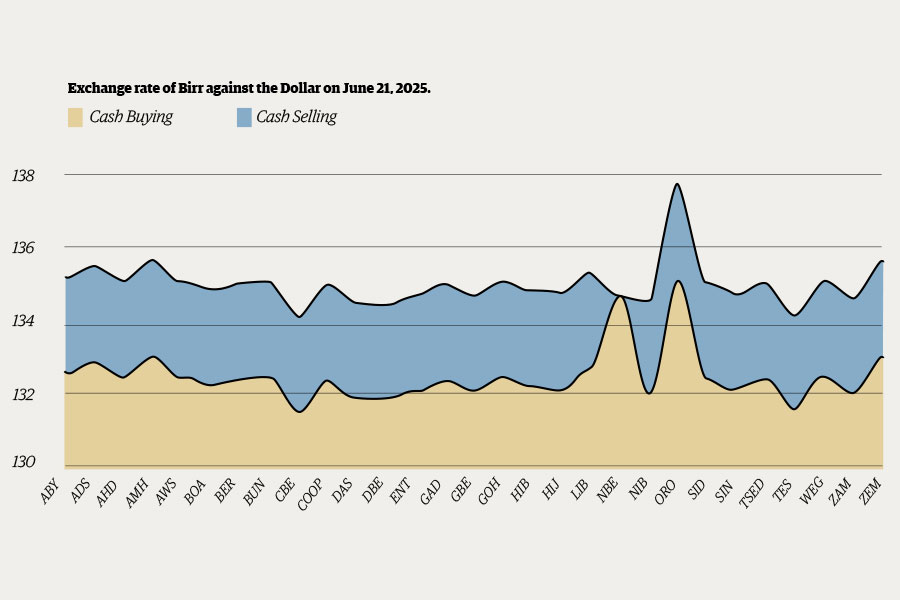

Money Market Watch | Jun 21,2025

Radar | May 21,2022

Radar | Jun 04,2022

Radar | Jul 11,2021

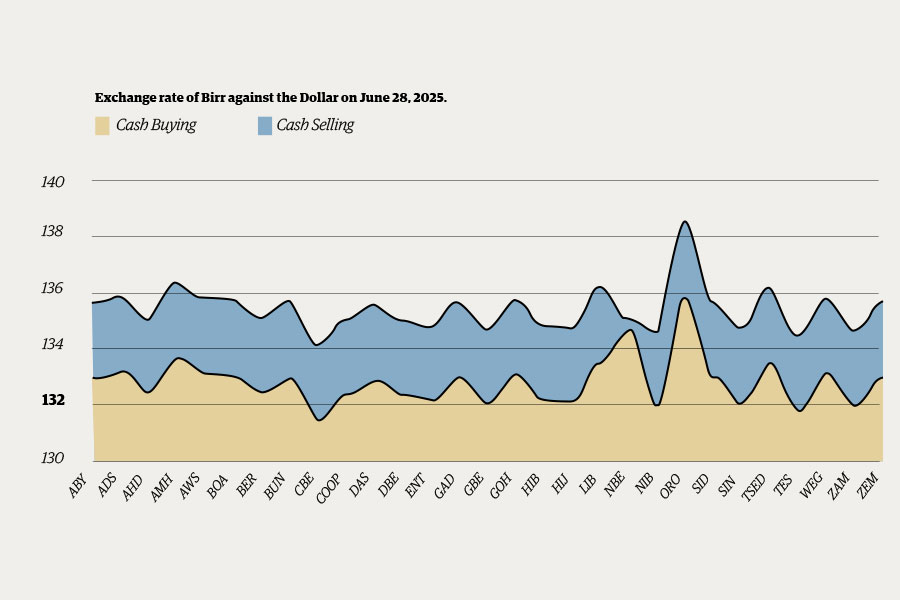

Money Market Watch | Jun 29,2025

Fortune News | Jun 05,2021

Fortune News | Mar 13,2021

Fortune News | Jul 23,2022

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 31 , 2026

Weldu Yiheysh has not read the Pacific temperature charts. He does not need to. In Shibta District of Enderta Wereda, in...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Loading your updates...

Loading your updates...