Radar | Dec 13,2025

Jun 21 , 2025

By Ramona Kettenstock

In a historic first for Ethiopia’s financial sector, the National Bank of Ethiopia (NBE) has unveiled the "Women’s Financial Inclusion Scorecard", a pioneering initiative that may well become a game-changer in the quest for gender equity in finance. Designed in partnership with the World Bank’s Africa Gender Innovation Lab, the Scorecard represents more than just a measurement tool; it is a bold statement of intent and a strategic lever for reform.

Why does this matter?

For far too long, women in Ethiopia have remained underserved and underrepresented, both as clients of and leaders in financial institutions. They are 1.5 times less likely than men to access formal loans, hold fewer digital accounts, and occupy an extremely small proportion of senior management roles. The Scorecard wants to change this.

The tool, developed as part of Ethiopia’s National Financial Inclusion Strategy II (NFIS-II, 2021–2025), offers a standardised way for banks to assess their performance across three critical dimensions: women in their workforce, women’s use of financial products, and financial innovation tailored to women’s needs. This structured and data-driven approach marks a shift from aspirational rhetoric to actionable accountability.

The findings from the inaugural cycle, spanning 30 of the 32 commercial banks, reveal an industry that is beginning to move but still has a long way to go. On average, banks score 2.95 in the composite index, ranging from one (lowest) to five (highest), placing most institutions in the average “Building Momentum” category. Encouragingly, one institution, Enat Bank, founded with a mission to serve women, achieved the highest status, “Transformational,” demonstrating what is possible when inclusion is at the core of its institutional identity.

Enat Bank was the only institution to achieve a “Transformational” score, but it is not alone in demonstrating meaningful progress. Three other banks, such as Goh Betoch, Tsedey, and Wegagen, were rated “Intentional,” signalling their strong institutional commitment to women’s inclusion. A further 19 banks, including Ahadu, Amhara, Abyssinia, Bunna, Commercial Bank of Ethiopia, Cooperative Bank of Oromia, Dashen, Global Bank Ethiopia, Hibret, Hijra, Lion International, Nib International, Omo, Oromia, Shabelle, Siinqee, Siket, ZamZam, and Zemen, are “Building Momentum,” illustrating growing but not yet fully institutionalised efforts.

The remaining seven financial institutions Abay, Addis International, Awash, Development Bank of Ethiopia, Gadaa, Rammis, and Tsehay were assessed as either “Neutral” or in “Emerging Awareness,” indicating foundational or early-stage engagement with gender inclusion.

Government mandates are playing a vital role in nudging the sector forward. Recent regulations require at least one woman on every bank board and aim for 25pc of senior management to be female. These policies are not merely symbolic; they are catalysing fundamental institutional shifts, especially in workforce inclusion, where board diversity is visibly improving. Yet, progress is uneven. While workforce metrics show some progress, especially in boardroom representation, structural support for women, such as childcare, flexible work arrangements, and mentorship, remains scarce.

On the client side, banks are beginning to reach more women, but products often remain generic and poorly tailored to women’s unique financial realities. Innovation, particularly in digital finance, is still in its infancy.

What the Scorecard ultimately reveals is not failure, but untapped potential. Women are not a niche market. They are a growth engine. Research has consistently shown that women repay loans at higher rates, invest more in their families, and can drive broader social and economic impact when financially empowered. The Women Entrepreneurship Development Project, for instance, reported a 99.6pc loan repayment rate among women participants. Closing the gender gap in access to finance could unlock up to 3.7 billion dollars annually in additional GDP for Ethiopia.

The message to banks is clear. Investing in women is not charity, but a smart business move.

To accelerate momentum, financial institutions should move beyond compliance and into strategy. First, they need to develop financial products based on the lived experiences of women, with products that are flexible, accessible, and relevant to informal workers, smallholder farmers, and urban entrepreneurs alike. Digital innovation should also be gender-intentional. The digital divide is real, and solutions should be designed to include, not exclude, women.

Internally, the sector can create leadership pathways for women, backed by mentorship, professional development, and family-friendly policies. And critically, all of this should be underpinned by data. Many banks still lack the systems to collect and analyse gender-disaggregated data, limiting their ability to design responsive services or track their impact.

The NBE has wisely positioned the Scorecard not as an enforcement tool, but as a learning and transparency mechanism. This approach promotes a culture of progress rather than sanction, enabling institutions to benchmark against peers, identify gaps, and adopt best practices.

Looking ahead, the Scorecard offers a foundation for systemic change. But it will only succeed if banks treat it not as a box-ticking exercise, but as a strategic compass. Regulators, investors, and donors can reinforce this by aligning capital, incentives, and technical support with institutions that lead on inclusion.

Ethiopia’s financial institutions now face a choice. Either they will have to remain passive observers in the face of systemic inequality, or become active architects of an inclusive economy. The Scorecard has lit the path. It is up to the industry to walk it.

PUBLISHED ON

Jun 21,2025 [ VOL

26 , NO

1312]

Ramona Kettenstock is a partner of BKP Economic Advisors, a German based economic research and consulting firm.

Radar | Dec 13,2025

In-Picture | Nov 22,2025

Editorial | Oct 20,2024

My Opinion | Aug 18,2024

Fortune News | Jul 01,2023

View From Arada | Apr 10,2026

Fortune News | Apr 20,2019

Fortune News | Jul 02,2026

Radar | May 23,2021

View From Arada | Nov 11,2023

Photo Gallery | 192206 Views | May 06,2019

Photo Gallery | 181978 Views | Apr 26,2019

Photo Gallery | 178718 Views | Oct 06,2021

My Opinion | 144235 Views | Aug 14,2021

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Jul 25 , 2026

Ideally, citizens who have paid income tax all year should not have to reach for thei...

Jul 18 , 2026

Pressed in Parliament on jobs and household incomes, Prime Minister Abiy Ahmed (PhD)...

Jul 11 , 2026

At a market stall, reform arrives without a communique. It comes as a higher transpor...

Jul 4 , 2026

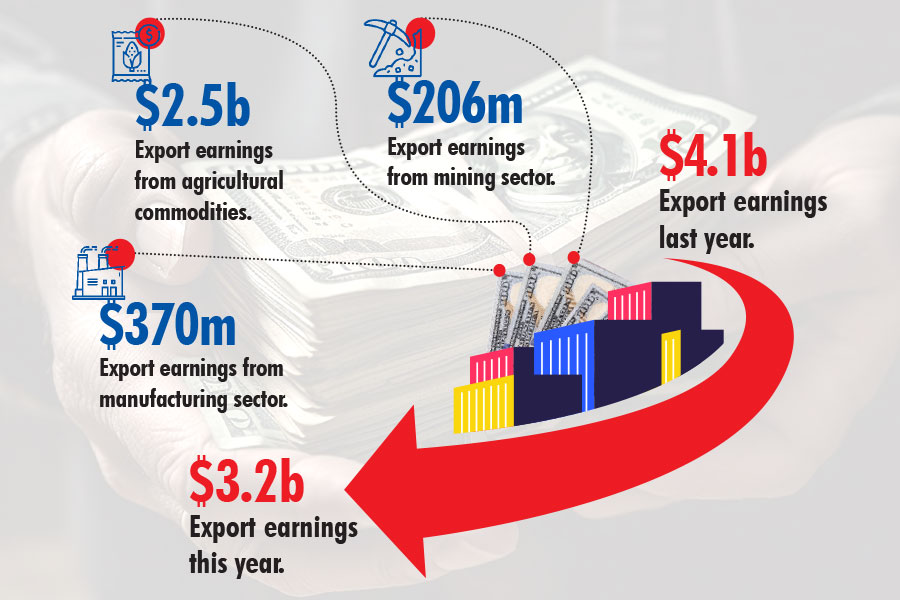

In the goldfields of the Benishangul-Gumuz Regional State, Ethiopia's balance-of-paym...

Jul 25 , 2026 . By BEZAWIT HULUAGER

Global Bank's Board of Directors have overhauled top management, after suspending sev...

Jul 25 , 2026 . By NAHOM AYELE

Judges at the Federal High Court have overturned the National Lottery Administration...

A newly enacted regulation by the Council of Ministers lets eligible producers pledge...

Jul 25 , 2026 . By FITSUM TADESSE

A fuel tanker carrying tens of thousands of litres was confiscated after its driver a...

Loading your updates...

Loading your updates...