Photo Gallery | 174237 Views | May 06,2019

Feb 9 , 2025

By Nohaila Ibn ElFarouk

Traditional banks are facing mounting pressure to reinvent themselves in a rapidly changing financial sector. The twin forces of technological advancements and the rise of agile neo-banks have disrupted traditional business models, while the emergence of Generation Z as a major consumer group is further accelerating the need for change.

Zoomers — those born between 1997 and 2012 — are redefining what customers expect from their financial service providers. Accustomed to the immediacy and convenience of digital platforms, they demand a customer-centric approach that goes well beyond traditional banking. As early as 2025, this generation will represent 27pc of the global workforce. In Nigeria alone, there are 44 million Gen Z members, a demographic that is quickly establishing itself as a formidable economic force.

Recent studies show that Zoomers are the most optimistic generation when it comes to their financial future. One global survey indicates that 71pc of Gen Z believe they will achieve financial stability, while 41pc view their financial provider as a partner in reaching their financial goals. This optimism is coupled with a strong preference for digital and mobile-first financial services. In Africa, Zoomers are at the forefront of the mobile money revolution, using mobile payment platforms 80pc more frequently than older generations.

This shift in consumer behaviour has forced banks to rethink their offerings. No longer can they rely solely on basic services such as account management or long-term savings products. Today's customers, particularly those in Gen Z, seek an integrated digital experience that combines financial tools with lifestyle capabilities. Banking apps that incorporate features like saving pots, budgeting tools, and seamless integration with e-commerce platforms are increasingly in demand. Customers now expect their financial applications to not only manage their money but also offer direct access to third-party services, such as insurance products, through a single, unified interface.

Mauritius Commercial Bank (MCB) provides a leading example of this trend with its enhanced "Juice" platform.

The recent launch of Juice Tap demonstrates the power of integrating cutting-edge technology into traditional banking services. Using near-field communication (NFC) technology, Juice Tap enables seamless contactless payments and allows customers to consolidate multiple accounts, including external bank accounts, into one easy-to-use digital wallet. In addition to streamlined bill management, the platform offers features designed to meet the digital demands of a modern, mobile-savvy customer base.

The influence of Zoomers is not limited to any one region or age group. While their behaviour is particularly pronounced in Africa, where digital adoption is exceptionally high, users of all ages are beginning to appreciate the convenience and efficiency of integrated financial ecosystems. As these digital natives migrate to platforms that offer increased ease and accessibility, traditional banks are compelled to accelerate their own digital transformations.

One promising strategy that has emerged in response to these challenges is composable banking. This modular approach allows banks to move away from siloed, inflexible systems and toward a unified, adaptable architecture that can be easily reconfigured to meet evolving customer needs. Composable banking supports rapid innovation, enabling financial institutions to integrate new technologies and tailor their services to the digital lifestyle expectations of younger consumers.

By adopting composable banking, banks are positioning themselves to deliver more personalised and responsive customer experiences. Unified banking platforms built on this framework reduce complexity and shorten the time it takes to bring new services to market. This agility not only appeals to tech-savvy Gen Z users but also helps banks reduce costs and stay competitive in an increasingly dynamic market environment.

The transformation of banking services extends beyond the simple digitization of existing processes. Banks should now reimagine how they deliver financial services altogether. This shift requires a holistic approach that encompasses technology and customer experience. Rather than offering a series of disjointed digital tools, forward-thinking financial institutions are developing integrated ecosystems that mirror the seamless experiences found in other areas of digital life.

As Gen Z continues to mature and accumulate wealth, their influence over the financial sector will only grow stronger. Their expectations for real-time, intuitive, and comprehensive digital experiences are setting new standards for the industry. Traditional banks that fail to meet these expectations risk losing the loyalty of a generation that views financial providers not merely as custodians of money but as partners in achieving life goals.

The story unfolding in Africa, where mobile payment platforms are embraced at an unprecedented rate, offers a glimpse into the future of global banking. Digital-first experiences, the integration of lifestyle services, and the adoption of composable banking architectures are not simply trends. They represent a fundamental shift in how financial services are delivered and consumed. As banks steer this transition, the challenge will be to balance the legacy of traditional banking with the need for innovation.

Ultimately, the rise of Gen Z is more than a demographic shift; it is a signal that the future of banking lies in flexibility, integration, and customer-centric design. Banks that successfully reinvent themselves will capture the loyalty of younger consumers and redefine their role in a market that increasingly values agility and personalisation over tradition.

PUBLISHED ON

Feb 09, 2025 [ VOL

25 , NO

1293]

Photo Gallery | 174237 Views | May 06,2019

Photo Gallery | 164462 Views | Apr 26,2019

Photo Gallery | 154615 Views | Oct 06,2021

My Opinion | 136655 Views | Aug 14,2021

Editorial | Oct 11,2025

Dec 22 , 2024 . By TIZITA SHEWAFERAW

Charged with transforming colossal state-owned enterprises into modern and competitiv...

Aug 18 , 2024 . By AKSAH ITALO

Although predictable Yonas Zerihun's job in the ride-hailing service is not immune to...

Jul 28 , 2024 . By TIZITA SHEWAFERAW

Unhabitual, perhaps too many, Samuel Gebreyohannes, 38, used to occasionally enjoy a couple of beers at breakfast. However, he recently swit...

Jul 13 , 2024 . By AKSAH ITALO

Investors who rely on tractors, trucks, and field vehicles for commuting, transporting commodities, and f...

Oct 11 , 2025

Ladislas Farago, a roving Associated Press (AP) correspondent, arrived in Ethiopia in...

Oct 4 , 2025

Eyob Tekalegn (PhD) had been in the Governor's chair for only weeks when, on Septembe...

Sep 27 , 2025

Four years into an experiment with “shock therapy” in education, the national moo...

Sep 20 , 2025

Getachew Reda's return to the national stage was always going to stir attention. Once...

Oct 12 , 2025

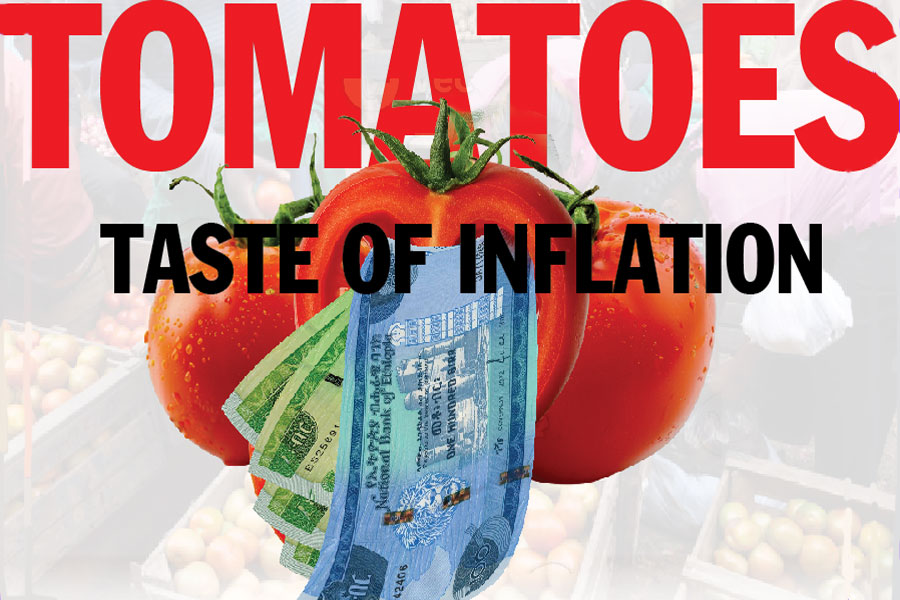

Tomato prices in Addis Abeba have surged to unprecedented levels, with retail stands charging between 85 Br and 140 Br a kilo, nearly triple...

Oct 12 , 2025 . By BEZAWIT HULUAGER

A sweeping change in the vehicle licensing system has tilted the scales in favour of electric vehicle (EV...

Oct 12 , 2025 . By NAHOM AYELE

A simmering dispute between the legal profession and the federal government is nearing a breaking point,...

Oct 12 , 2025 . By NAHOM AYELE

A violent storm that ripped through the flower belt of Bishoftu (Debreziet), 45Km east of the capital, in...

Loading your updates...

Loading your updates...