Radar | Dec 04,2022

Apr 6 , 2019

By Abdulmenan Mohammed

The National Bank of Ethiopia is on track to undertake significant financial sector reforms. Major policy changes though should not come before there is clarity on the economic direction the nation should pursue, writes Abdulmenan Mohammed (abham2010@yahoo.co.uk), a financial expert with 15 years of experience and based in the United Kingdom.

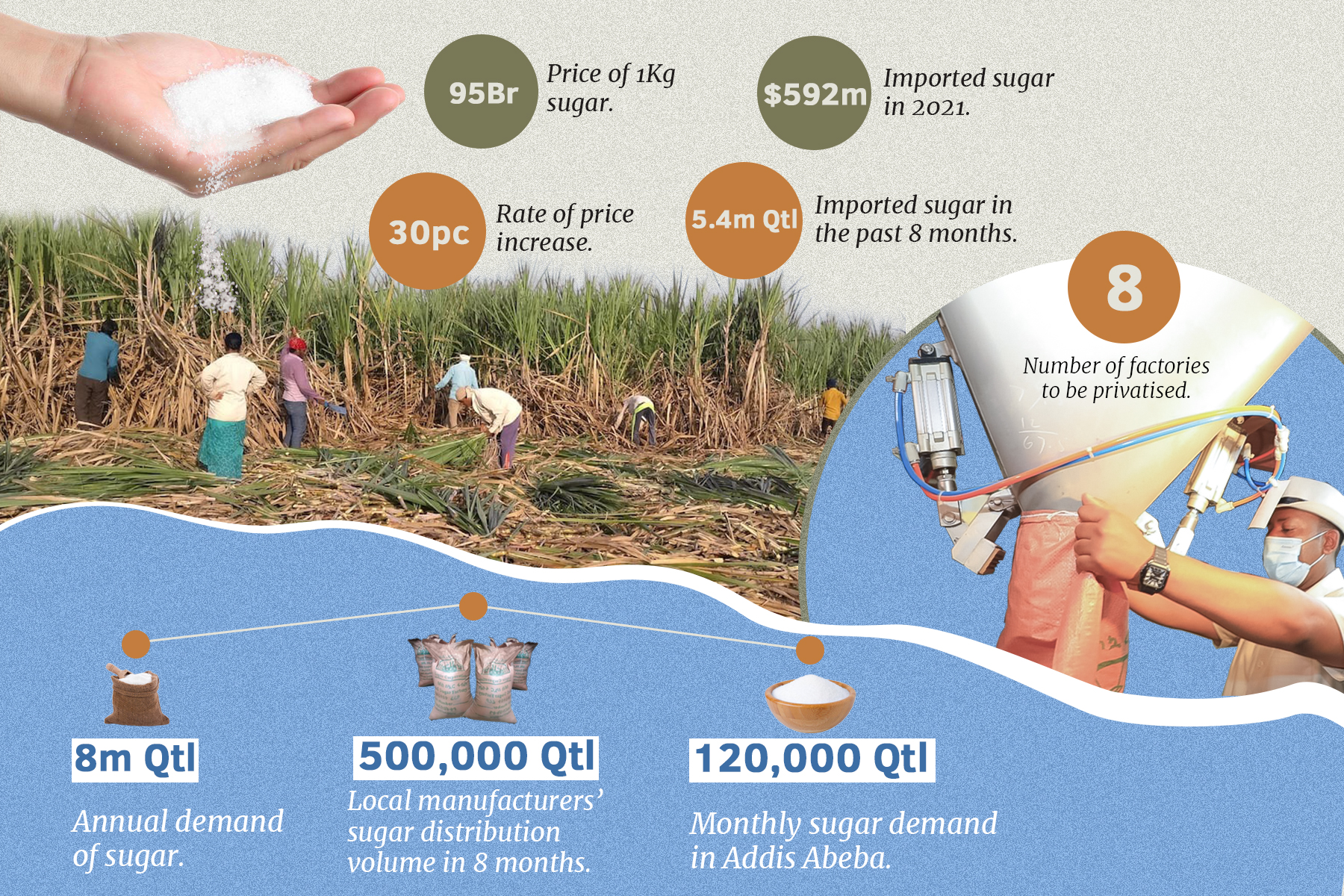

Late last month, Yinager Dessie (PhD), governor of the National Bank of Ethiopia (NBE), presented the eight-month performance report on the Ethiopian economy to parliament. The governor’s report covered several issues such as interest rate, advances to the government, foreign reserves and import-export performance.

What is interesting was that he stated that studies are being undertaken in collaboration with experts of the World Bank to make significant reforms in the financial sector. It included opening it up to international players, the establishment of a capital market, modernising the payment system and allowing the diaspora community to invest in the financial sector. These reforms may be considered as serious as those reforms made in the early 1990s, such as financial sector liberalisation for domestic private players.

Over the past 15 years, the ruling party has tenaciously pursued the developmental state model. The state has been considered the driver of economic development. The role of the banking sector was defined within this economic paradigm. It preferred credit-based instead of market-based financial system and credits allocation have been influenced according to government priority rather than based on market principles.

This economic paradigm resulted in the heavy presence of public banks in the financial sector. The Development Bank of Ethiopia (DBE) was positioned as a policy bank for funding priority private industrial and agricultural developments and the Commercial Bank of Ethiopia (CBE) was tasked to finance mega-state projects. Private banks were forced to purchase significant amounts of NBE bills to funding the policy bank’s operations.

More than a quarter of private banks’ deposits was used for the purchase of NBE bills and interest rates have been kept low for prioritised long-term projects to foster industrial and agricultural transformation.

Consequently, out of the total deposits of 750.36 billion Br, public banks mobilised 61.3pc and disbursed 75.3 pc of the loans and advances. Over half of the loans and advances of the sector were given to state-owned enterprises (SOEs), with two taking up almost a third of the banking sector’s credit. CBE is as a result exposed to significant credit risks.

Non-prudential loans and advances to risky ventures have also exposed DBE to massive credit risks. As a result, its non-performing loans soared to the point that has shaken the financial position of the policy bank to the core. Without extensive financial restructuring, its continuity has become a going concern.

In the past year, several economic measures such as the announcement of privatisation of SOEs have been taken due to soaring state debt and worrying economic situation. The measures showed the limits of debt-fuelled state-led development.

Even if the decade-old economic philosophy seemed to run out of steam and economic reforms are underway, there is still a lack of clarity about the economic direction that the government should be pursuing. It is in this context of economic policy ambiguity that financial sector reform is being considered.

An economic philosophy that is explicitly spelt out provides a rationale for the financial sector reforms. It is essential to locating the role of the financial sector within in the overall economy, avoiding policy incompatibilities, charting the long-term course of the financial sector and making reforms go beyond addressing issues such as shortage of hard currencies. It will also identify the role the central bank and public banks should play.

If economic reforms are intended to expand the role of the private sector, reforming the financial system should be conducted with the intention of expanding the role market forces play in resource allocation, increasing autonomy for the central bank, deepening of the treasury bills market to scale down government borrowing from central bank and creating capital markets. The right set of reforms would entail enabling financial institutions to function according to market principles, limiting state intervention in their decision-making process and guaranteeing central bank independence.

The creation of a capital market is a commendable move as it will be a platform for raising long-term funds and allocating resources efficiently. Allowing foreign nationals of Ethiopian origin to invest in the financial sector is overdue. As it does not pose serious regulatory issues; speeding the process will only enable the diaspora community to engage in the financial sector.

The reform should also address quantity restrictions, including the removal of direct credit allocation mechanisms such as the NBE bonds that private banks are compelled to purchase. Relaxation of entry barriers in the financial system will foster competition. This entails reducing the capital requirement so that new players would join the banking industry and opening the sector for foreign banks. How foreign banks will be engaged in the financial sector and regulated should be thought out thoroughly.

What is fundamentally important is the redefinition of the role of public banks. There should be a roadmap that would eventually enable them to operate on market principles and foster private sector development. This will require gradual removal of special privileges afforded to public banks.

PUBLISHED ON

Apr 06,2019 [ VOL

19 , NO

988]

Radar | Dec 04,2022

Radar | Jan 07,2023

My Opinion | Apr 22,2022

Viewpoints | Apr 30,2021

Featured | Mar 30,2019

Photo Gallery | 96719 Views | May 06,2019

Photo Gallery | 88897 Views | Apr 26,2019

My Opinion | 67161 Views | Aug 14,2021

Commentaries | 65756 Views | Oct 02,2021

Feb 24 , 2024 . By MUNIR SHEMSU

Abel Yeshitila, a real estate developer with a 12-year track record, finds himself unable to sell homes in his latest venture. Despite slash...

Feb 10 , 2024 . By MUNIR SHEMSU

In his last week's address to Parliament, Prime Minister Abiy Ahmed (PhD) painted a picture of an economy...

Jan 7 , 2024

In the realm of international finance and diplomacy, few cities hold the distinction that Addis Abeba doe...

Sep 30 , 2023 . By AKSAH ITALO

On a chilly morning outside Ke'Geberew Market, Yeshi Chane, a 35-year-old mother cradling her seven-month-old baby, stands amidst the throng...

Apr 20 , 2024

In a departure from its traditionally opaque practices, the National Bank of Ethiopia...

Apr 13 , 2024

In the hushed corridors of the legislative house on Lorenzo Te'azaz Road (Arat Kilo)...

Apr 6 , 2024

In a rather unsettling turn of events, the state-owned Commercial Bank of Ethiopia (C...

Mar 30 , 2024

Ethiopian authorities find themselves at a crossroads in the shadow of a global econo...

Apr 20 , 2024

Ethiopia's economic reform negotiations with the International Monetary Fund (IMF) are in their fourth round, taking place in Washington, D...

Apr 20 , 2024 . By BERSABEH GEBRE

An undercurrent of controversy surrounds the appointment of founding members of Amhara Bank after regulat...

An ambitious cooperative housing initiative designed to provide thousands with affordable homes is mired...

Apr 20 , 2024 . By AKSAH ITALO

Ethiopia's juice manufacturers confront formidable economic challenges following the reclassification of...

Loading your updates...

Loading your updates...