Radar | Nov 19,2022

Aug 17 , 2019

By Fiseha Haile

Structural reforms should be done for the “right” reason, that is to improve efficiency and productivity, writes Fiseha Haile, an economist at an international development organisation. The views and opinions expressed in this article are solely those of the author and do not necessarily reflect the views of the organisation he works for. He can be reached at fisehahaile77@yahoo.com.

Responding to questions in parliament following the 2007 global financial crisis, the late Prime Minister Meles Zenawi argued that the crisis would not have drastic repercussions on Ethiopia, because its financial system was not liberalised and integrated into the global system. “Our boat is not yet in the oceans where the big ships are colliding. Ours is a small boat, and it is somewhere in the rivers,” he added humorously.

The “small boat” is now being undocked and is about to set sail to the oceans. The ruling party, EPRDF, is working toward privatising major state-owned enterprises, including Ethio telecom, Ethiopian Electric Power and Ethiopian Airlines, and liberalising the domestic financial market.

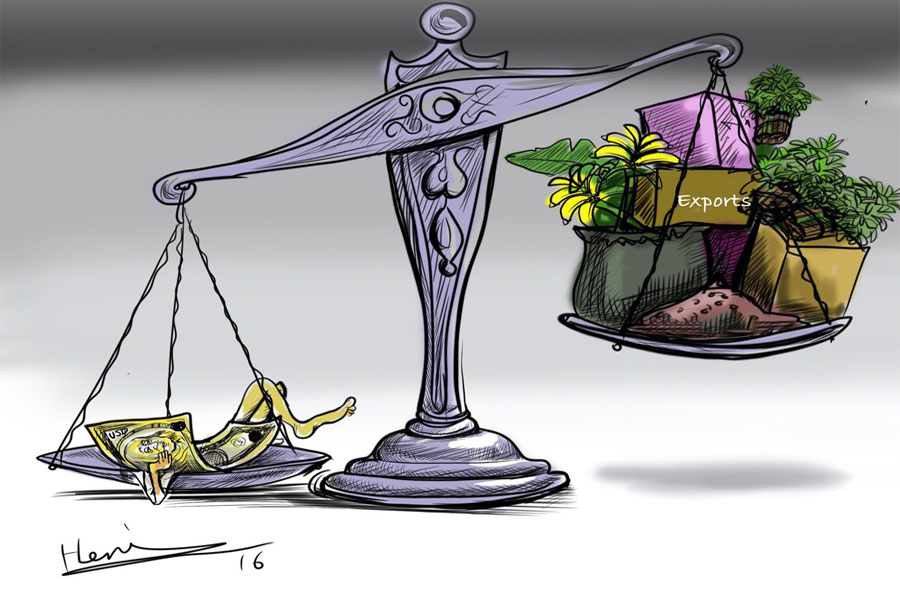

Despite rapid economic growth that lasted more than a decade, Ethiopia has been grappling with several challenges in recent years. Falling exports, chronic foreign currency shortages, debt overhang and rampant youth unemployment continue to threaten the economic stability and social fabric of the country.

The incumbent government has embarked on a reform programme to redress the multifaceted development challenges. However, the laundry list of reforms, from privatisation to trade reforms, from exchange rates to domestic financial liberalisation, do not seem to be anchored in a broader economic strategy. Hence the tendency on the part of the government to implement all of them at the same time - dubbed a “spray-gun” approach to reforms. The pacing and sequencing of reforms are, however, critical to the success, or lack thereof, of reforms. Ethiopian policymakers need to carefully investigate what policies worked in the past, what did not and why, before they start introducing ad hoc measures to circumvent systemic problems.

Why did Ethiopia’s growth model fail to produce jobs and dollars but rather led to a massive debt burden? Since the mid-2000s, the government has made massive public investment in roads, electricity, education, etc., financed by credit from the domestic banking sector and external loans. Ethiopia has had one of the highest public investment rates in the world. These are commendable efforts and exemplary for many African countries that spend little to nothing on infrastructure and human capital. However, the government is struggling to secure foreign currency to cover even strategic imports like oil and medicine. At the same time, hundreds of thousands of graduates remain unemployed or underemployed.

It bears noting that public infrastructure is not necessarily an end in itself; it is rather a means to crowd in or foster the growth of firms that could in turn help generate jobs and dollars. In the last decade, an omnipresent state meant that the private sector remained nascent, crowded out from the credit and forex markets. Since the mid-2000s, Ethiopia pursued a model of financial repression that kept interest rates low and channeled the bulk of credit toward public investment, leaving limited space for the private sector.

While the government made critical infrastructure investments, it miserably failed when it attempted to substitute the private sector. Key state-led projects and enterprises, including sugar factories and the military-run METEC, were unproductive and led to a rapid buildup of debt. Noble prize-winning development economist Arthur Lewis said that “Governments may fail either because they do too little, or because they do too much.” Too little private investment-a key driver of growth and job creation-is one of the main reasons why the Ethiopian growth model ran out of steam in a little over a decade. Even though firms reached a point where they needed more credit than infrastructure to grow and prosper, the government continued to expand its presence in the economy, thereby becoming counterproductive.

The private sector should play a much greater role if Ethiopia is to realise its aspirations of becoming a middle-income economy. Promoting private sector-led growth would, among other things, require increasing the supply of credit and foreign currency, and alleviating other key business environment constraints, including access to land, electricity, trade logistics and a cumbersome regulatory framework.

“No country has sustained rapid growth without also keeping up impressive rates of public investment," according to the Commission on Growth and Development that included Nobel prize-winning academics and experienced policymakers. However, the Commission also notes that “government is not the proximate cause of growth. That role falls to the private sector, to investment and entrepreneurship responding to price signals and market forces.”

Ethiopia has made only limited progress in letting markets allocate resources and promoting a thriving private sector. Similarly, it featured several of what the Commission identifies as suboptimal policies, such as excessive interference in the banking system and open-ended protection of a wide range of sectors, including through oversized state-owned enterprises (SOEs).

Fostering a vibrant private sector will require reducing and redefining the role of the state. Although there is a broad-based consensus on the need for privatisation of the SOE sector, the questions of what, when and how to privatise have been the subject of intense debate. A move from state to private, or pseudo-private, ownership alone does not necessarily and automatically yield economic gains and thus needs to be handled with the utmost care. Left to their own devices, unfettered markets could wreak havoc on the Ethiopian economy, given the private sector is too undeveloped to withstand foreign competition, the government too unprepared to effectively regulate markets, and the state too weak to provide important institutions that would enable the market to function as designed.

Privatising strategic industries and liberalising the domestic financial market at breakneck speed, just for the sake of addressing the foreign currency crunch, is a recipe for disaster. Africa’s rich experience with liberalisation reforms showed that a single-minded focus on the magic of "‘state minimalism" and "getting prices right" could do more harm than good. Growth and development require a lot more than just getting prices right. In fact, as documented in the classic works of Alice Amsden and Ha-Joon Chang, today’s advanced Asian and Western economies got rich by "deliberately getting prices wrong" and targeted state intervention in order to jump-start industrialisation and structural transformation.

Structural reforms should be done for the “right” reason, that is to improve efficiency and productivity. Nobel Prize-winning economist Paul Krugman is often quoted as saying, “productivity isn’t everything, but, in the long run, it is almost everything."

Ethiopia’s planned privatisation and liberalisation measures should not be seen as silver bullets to solve structural problems but rather as part of a broader set of reforms to promote competition, improve economic efficiency and deter regulatory capture.

Experience shows that privatisation may be successful in a sector that is most inefficient and unprofitable but potentially a competitive industry; that has the least adverse distributional impact; and where government has adequate regulatory capabilities. In the electricity sector, profit-seeking firms do not have the incentive to serve low-income customers. In fact, privatisation of the utility sector could cause dire social consequences, unless combined with measures to mitigate adverse welfare impacts.

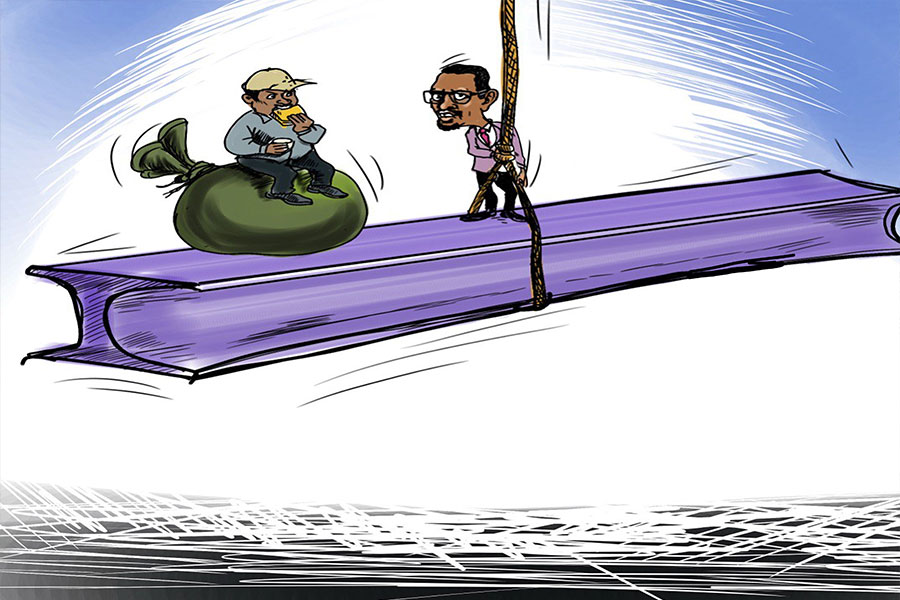

A great deal of caution will also be needed in the pacing of divestitures, not least because Ethiopia has very little experience to fall back on. Privatising the above-listed SOEs all at once-dubbed a “fire sale” approach-should be shunned. The government’s bargaining power, and thus the proceeds it receives, is reduced when privatisation is desperately done at a large scale within a short period.

The case of Ethiopian Airlines has been the most contested, and rightly so. There is no convincing rationale for privatising the Airlines. Ethiopian is well-managed, even by international standards, and has consistently surpassed its profit targets. Ethiopia would do well to learn from its neighbour, Kenya, whose parliament voted last month to re-nationalise its national carrier Kenyan Airways, which badly suffered in private hands.

Also, it is not wise to open the banking sector to foreign banks in the medium-term given the government regulator is insufficiently prepared. The Central Bank has been struggling to successfully discharge its basic responsibilities-notably managing the currency-let alone to effectively regulate foreign banks that come with volatile capital flows and hard-to-regulate financial instruments.

Despite theoretically sound arguments, short-term private capital flows-referred to as “bad cholesterol”-may pose substantial countervailing risks as they are often motivated by speculative considerations and thus prone to quick reversals. Many developing countries consider foreign direct investment (FDI), aka “good cholesterol,” as the private capital inflow of choice due to its resilience. Conventional wisdom suggests that low-income countries need to reach a certain level of financial and institutional development before they can start reaping the potential benefits of relatively unbridled capital flows.

As the oft-repeated adage goes, “if you fail to plan, you plan to fail.” There is hardly any time for large-scale policy experimentation and the cost of taking a wrong path could be unbearable.

PUBLISHED ON

Aug 17,2019 [ VOL

20 , NO

1007]

Radar | Nov 04,2023

Radar | May 28,2022

View From Arada | Aug 03,2019

Commentaries | May 25,2019

Verbatim | Jan 12,2019

Photo Gallery | 96131 Views | May 06,2019

Photo Gallery | 88392 Views | Apr 26,2019

My Opinion | 66994 Views | Aug 14,2021

Commentaries | 65715 Views | Oct 02,2021

My Opinion | Apr 13,2024

Feb 24 , 2024 . By MUNIR SHEMSU

Abel Yeshitila, a real estate developer with a 12-year track record, finds himself unable to sell homes in his latest venture. Despite slash...

Feb 10 , 2024 . By MUNIR SHEMSU

In his last week's address to Parliament, Prime Minister Abiy Ahmed (PhD) painted a picture of an economy...

Jan 7 , 2024

In the realm of international finance and diplomacy, few cities hold the distinction that Addis Abeba doe...

Sep 30 , 2023 . By AKSAH ITALO

On a chilly morning outside Ke'Geberew Market, Yeshi Chane, a 35-year-old mother cradling her seven-month-old baby, stands amidst the throng...

Apr 13 , 2024

In the hushed corridors of the legislative house on Lorenzo Te'azaz Road (Arat Kilo)...

Apr 6 , 2024

In a rather unsettling turn of events, the state-owned Commercial Bank of Ethiopia (C...

Mar 30 , 2024

Ethiopian authorities find themselves at a crossroads in the shadow of a global econo...

Mar 23 , 2024

Addis Abeba has been experiencing rapid expansion over the past two decades. While se...

Apr 13 , 2024

A severe financial stranglehold has been imposed on the banking industry, underminin...

Apr 13 , 2024 . By MUNIR SHEMSU

In an unprecedented move, the central bank has published its inaugural stress test report, uncovering potential fault lines within the finan...

Apr 13 , 2024 . By MUNIR SHEMSU

In a bold departure from its historical position on foreign investment, the federal government has opened...

Apr 13 , 2024 . By AKSAH ITALO

A proposed excise tax stamp system draws controversy amongst industry leaders in the alcohol, tobacco, be...

Loading your updates...

Loading your updates...