Oct 24 , 2020.

Officials at the National Bank of Ethiopia (NBE) often like to remain on the fence when responding to inquiries and slow in their release of reports on the state of the economy. It may be the legacy of Teklewold Atnafu, the longest-serving former governor who is now advising Prime Minister Abiy Ahmed (PhD) on macroeconomic affairs. His predecessor, Yinager Dessie (PhD), and his lieutenants at the central bank have recently become more forthcoming. The Governor, in particular, has been more visible than usual as he brings forth the good news.

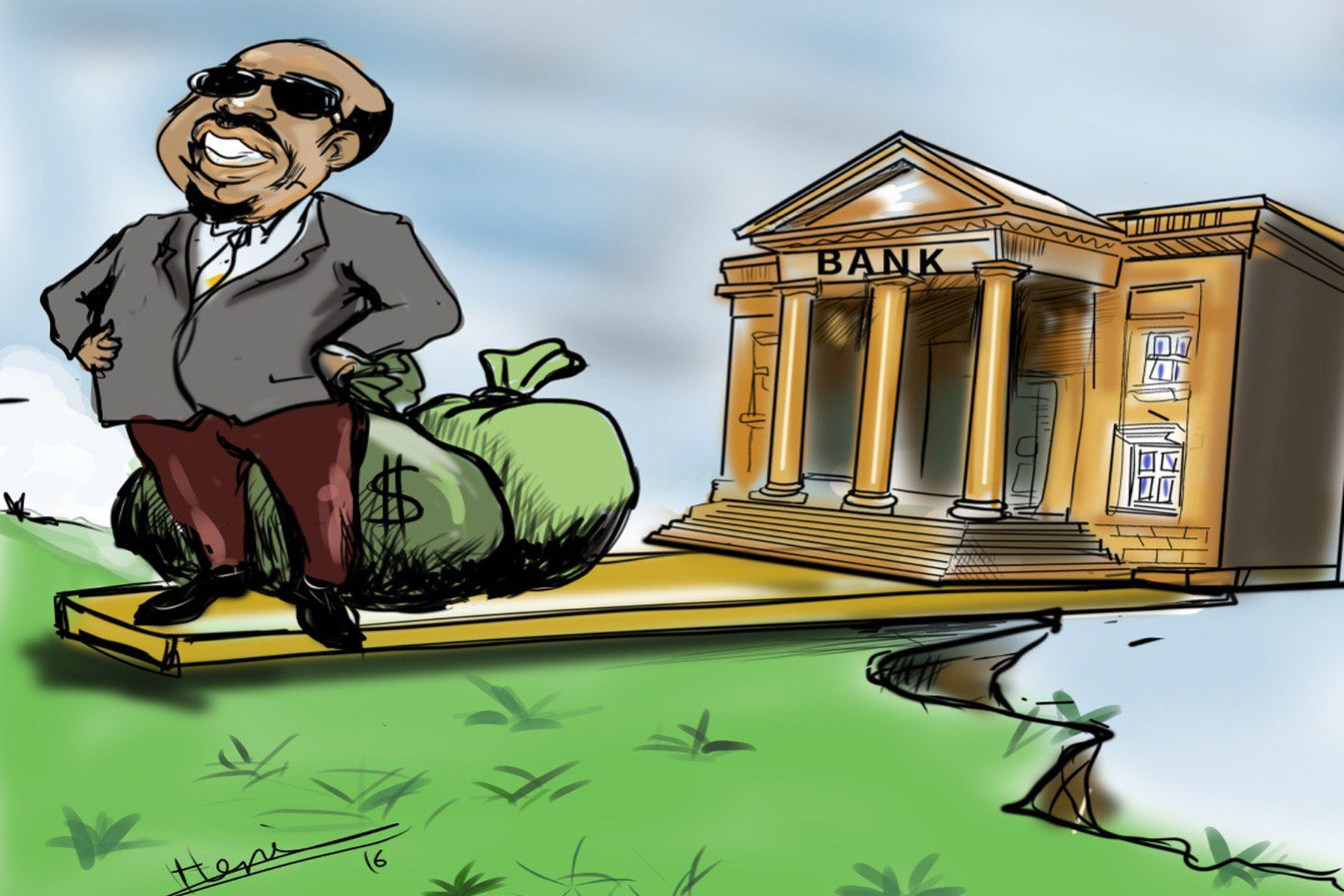

It could be because they seem to think they have a positive spin on the fruits of a measure taken over a month ago — issuing new notes. The technocrats call it "demonetisation". What could be acknowledged as part of the positive impacts of the demonetisation of the Birr in September this year is redirecting money in circulation, in the hands of households and businesses, into the banking system. The central bank hoped that this would tighten the reins on not just black money but the cash outside of the banking system that has contributed to the liquidity crunch in the financial system. By the time demonetisation was announced, central bank officials believed there was over 130 billion Br outside the direct control of banks.

Over 30 billion Br has to this point found its way back into banks, and around a million bank accounts have since opened. Although this represents only one-fourth of what was initially thought to sit outside banks, it seems sufficient for Governor Yinager to inform the market that 55 billion Br in loans were advanced during the first quarter of this fiscal year, an amount one-third higher compared to the same period last year.

Cash outside banks is not necessarily illegitimately acquired money. It is also the case that the amount of money still unaccounted for by banks remains around a third of what has been reported to be in private safe boxes and under mats. The threat of losing one’s legal tender in a few months has encouraged people to take their cash to banks. Considering that the deadline for exchanging over 100,000 Br into new notes has already elapsed and less than two months remain before the old notes become no longer tendered, however, this should be something that concerns officials at the central bank.

It may not be a misplaced concern. Demonetisation has forced savings to the advantage of the economy. It is in the end money that can be directed as credit, which is a considerable advantage in an economy that needs economic activities to be stimulated following the adverse impacts of the Novel Coronavirus (COVID-19) pandemic.

But the question remains, what could incentivise depositors to keep the money with the banks?

At the moment, there is very little. A direct correlation between consumption and savings is a concept well-established by pundits. Whichever pays better is likely to have influence. Banks are paying an average of eight percent in annual interest rates for savings. In the face of a monthly moving average of 20pc inflation over the past fiscal year, saving at banks sounds like a losing prospect. Even the lending rate adjusted for inflation is in the negative. It has been the case that savers in the Ethiopian market are subsidising borrowers; the latter take loans with negative real interest rates.

Under normal circumstances, such inflationary pressure would have made a case for central bankers to push policymakers to tighten their belts. But 2020 is not a normal year, and the impacts of the COVID-19 pandemic has created such economic disruptions that even the International Monetary Fund (IMF) is encouraging members countries to run fiscal deficits. Evidently, the average budget deficit against GDP hovers a little over three percent across the world, although few economies pushed this as high as 10pc.

The recommendation that an expansionary policy is better in the face of a slowing economy that leads to massive job losses and food insecurity was made some time ago. Monetary policy is also not likely to be of much help here either, as an expansionary policy entails lower interest rates and the printing of more of the notes. Even if it were the case that increasing the savings rate would lower inflation, it would lead to higher lending rates that would go on to disincentivise borrowing. It is a policy a government that desperately needs to stimulate business activities does not look forward to.

When it is the case that the government cannot stray away from the demand-side policies that have been the mainstay of economic policymaking for at least the last decade and a half, and inflation may be unavoidable, the policy tools remaining at the disposal are few. This is why it is important to innovate to find overlooked adjustments that could be made to ensure that savings created as a result of demonetisation can be redirected through the banking system.

This may have little to do with monetary and fiscal policies. But these are policies that could be encouraged by the central bank and implemented through the banks to focus on improving the saving culture in Ethiopia.

Amenable to developing countries with low savings rates are policies that have not been tried in Ethiopia such as commitment savings accounts, labeling and reminders. The former is a form of time-saving deposit but has greater flexibility to recover the money while disincentivising consumption. This intervention increased savings among a sample group in the Philippines by 82pc in a single year, according to a study conducted in the early 2000s by Innovations for Poverty Action, an American nonprofit.

Labeling is another design feature for bank accounts that allows earmarking savings for specific purposes, such as on health or education. At the same time, reminders are simply text-messages to clients to remind them of customised saving goals. The former was found to improve pocket spending on health by 65pc to 75pc in Kenya among farmers that opened labeled accounts. Reminders for specific saving goals improved saving by 16pc in sampled developing countries such as Bolivia and Peru.

Such interventions should not be taken lightly considering the increased awareness of behavioural economics and how factors such as mental accounting impact saving and consumption behaviour. They are simple but innovative interventions at the fingertips of policymakers and bank executives to improve the saving culture in Ethiopia. They are meaningful means of addressing economic headaches at a time when the government is forced to spend to stimulate the economy and thereby risk high inflation.

The challenge to saving does not end here though. There remains work to be done on what happens with the saved money. While the central bank reports credit by banks increased in the first quarter of the fiscal year, the appetite for investment has been going down even before COVID-19 existed.

A testament to this is foreign direct investment (FDI). Two years ago, the country was celebrating attracting four billion dollars in capital from non-Ethiopian investors. Just last year, the amount was a tiny fraction of that at half a billion dollars worth of capital investments. It is a precipitous decline in two years that will not be surprising considering the state of politics over the same period.

Uncertainty poses a challenge far more formidable than weak infrastructure, bureaucratic red tape or burdensome taxes. It is not even an economic policymaking issue. Neither the central bank nor the ministries of Finance, Revenues or Trade & Industry can do much about it.

To peace and stability as well as the economy, a fundamental challenge lies with a lack of political leadership. As long as parts of the country remain restive, it will continue to be a problem that puts at risk the lives of citizens, let alone securing the viability of businesses.

PUBLISHED ON

Oct 24,2020 [ VOL

21 , NO

1069]

Radar | Jun 12,2023

Sunday with Eden | Jun 08,2019

View From Arada | Apr 30,2021

Sunday with Eden | Nov 29,2020

Life Matters | Nov 26,2022

Fortune News | Jan 01,2023

Sunday with Eden | Nov 30,2019

Sunday with Eden | Sep 18,2021

Commentaries | Mar 27,2021

Fineline | Feb 23,2019

Photo Gallery | 96518 Views | May 06,2019

Photo Gallery | 88799 Views | Apr 26,2019

My Opinion | 67123 Views | Aug 14,2021

Commentaries | 65748 Views | Oct 02,2021

Feb 24 , 2024 . By MUNIR SHEMSU

Abel Yeshitila, a real estate developer with a 12-year track record, finds himself unable to sell homes in his latest venture. Despite slash...

Feb 10 , 2024 . By MUNIR SHEMSU

In his last week's address to Parliament, Prime Minister Abiy Ahmed (PhD) painted a picture of an economy...

Jan 7 , 2024

In the realm of international finance and diplomacy, few cities hold the distinction that Addis Abeba doe...

Sep 30 , 2023 . By AKSAH ITALO

On a chilly morning outside Ke'Geberew Market, Yeshi Chane, a 35-year-old mother cradling her seven-month-old baby, stands amidst the throng...

Apr 20 , 2024

Ethiopia's economic reform negotiations with the International Monetary Fund (IMF) are in their fourth round, taking place in Washington, D...

Apr 20 , 2024 . By BERSABEH GEBRE

An undercurrent of controversy surrounds the appointment of founding members of Amhara Bank after regulat...

An ambitious cooperative housing initiative designed to provide thousands with affordable homes is mired...

Apr 20 , 2024 . By AKSAH ITALO

Ethiopia's juice manufacturers confront formidable economic challenges following the reclassification of...

Loading your updates...

Loading your updates...